Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

My Private Journal

How do you react when the market is down?

I kept a little journal on my observations and thoughts when the market began the most rapid selloff in history. I intended to use it as a personal guide to go back and remind myself what I was thinking, observing and feeling.

Turns out, it’s one of the most valuable things I’ve ever done for myself…and frankly, for you too.

Let me share them—they are mostly based on observing people and behavior.

Focusing on the possibilities without properly considering the probabilities

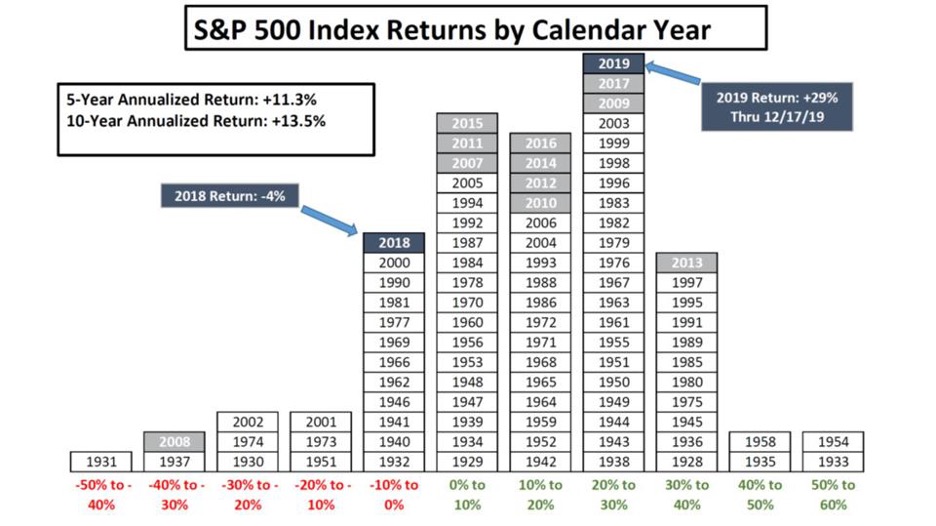

It’s important to remember that while the world is full of possibilities, they are different than probabilities. Over time, there is a greater possibility that the stock market and investment returns are positive. It’s like flipping a weighted coin that comes up a winner way more than a loser. Here’s data from FactSet and the graphic is from The St. Louis Trust Company.

Forgetting the above

You need to remember the above, no matter what the news is saying.

Abandoning their plan

Your plan should account for the unpredictable nature of the market and its temporary declines. This seemed to be the number one pitfall with the “do it yourself” (DIY) crowd and the “performance at all cost” people that I’ve spoken with. People usually abandon their plan when they either sucked to begin with or they were out of date. There is a difference between “a plan” and “planning.”

Thinking an advisor can control the market

Markets dictate returns, not an advisor. While advisors have influence over constructing an appropriate portfolio, it’s the market that has the greatest amount of influence.

Anchoring on starting portfolio values

Imagine that a DIY investor invests $100,000 in an all equity portfolio and generates gains of $50,000. The DIY investor then takes the $150,000 and hires an advisor and the advisor also maintains an all equity portfolio. A year later, the portfolio is valued at $125,000. Anchoring makes the investor feel like they lost $25,000. I saw that result in poor short-term decision making.

Making decisions in fear

Feeling fear during a market decline is natural, acting on it illogical. I saw a lot of mistakes made by people who did not have a firm grasp on their planning. In some cases, based on an investor’s age, the mistakes are irreparable. Knowing what the money is for, possessing a plan for it, and having the appropriate amount of cash in a portfolio is the antidote for fear. The most common phrase I heard from people who were doing solid planning was, “I’m okay, since I don’t need the money right now. I’m just not gonna look at it.” I swear.

Making changes to a portfolio

The time to make changes to a portfolio is when there are clear heads. Changes to portfolios should only be done when the plan is changing, not because the markets are changing. A well-constructed portfolio already KNOWS how the markets will behave. A bad portfolio is one that was never properly constructed in the first place to account for how markets behave.

Trying to time the market by selling and then buying back in

This observation is nothing new, but I saw it a lot more this year than ever. Getting this right requires guessing because there is no crystal ball. More accurately it requires two guesses: when to sell and when to buy back in. Ego and anchoring factor in too—the need to be right (or more accurately the need to “not be wrong”) is a powerful force. I’ve never witnessed anyone get it right, ESPECIALLY after taxes. The probability of two correctly-timed guesses is too low to make this worthwhile. As a client said to me on the phone today, “You take the stairs up and the escalator down with the market.”

Not appreciating the role of cash

Forget complicated options strategies and expensive hedge funds. Cash is the ultimate hedge. It is cheap, maintains value, reduces volatility, and more importantly, reduces anxiety. It also has what I call “value in use.” Finally, cash safeguards investors from having to make emotional decisions during selloffs. The hard part? Raising it when the market is doing well…mostly because of overconfidence and greed. Having a plan and sticking to it really helped investors during the selloff.

Taking advice from people who have nothing to lose

I’m talking about the dopes that pay PR firms to get them on CNBC and a lot of the analysts that publish projections. Eschew them all—they don’t know you, your situation, your goals or what your money is for. Most of your lifetime investment returns will be shaped by decisions you take (or don’t take) during very small windows of time in your life. Very few things are as important as understanding your own time horizon and not being swayed by the market fluctuations caused by people with different time horizons.

Not getting the big things right

I saw a lot of focus on the performance of individual securities that were of small overall significance to the entire portfolio by people who didn’t even have wills, trust and estate plans, or accurate beneficiaries designated in IRA accounts. Not owning Tesla is of little consequence if you die and your entire IRA goes to your ex.

Losing sight that declines are temporary

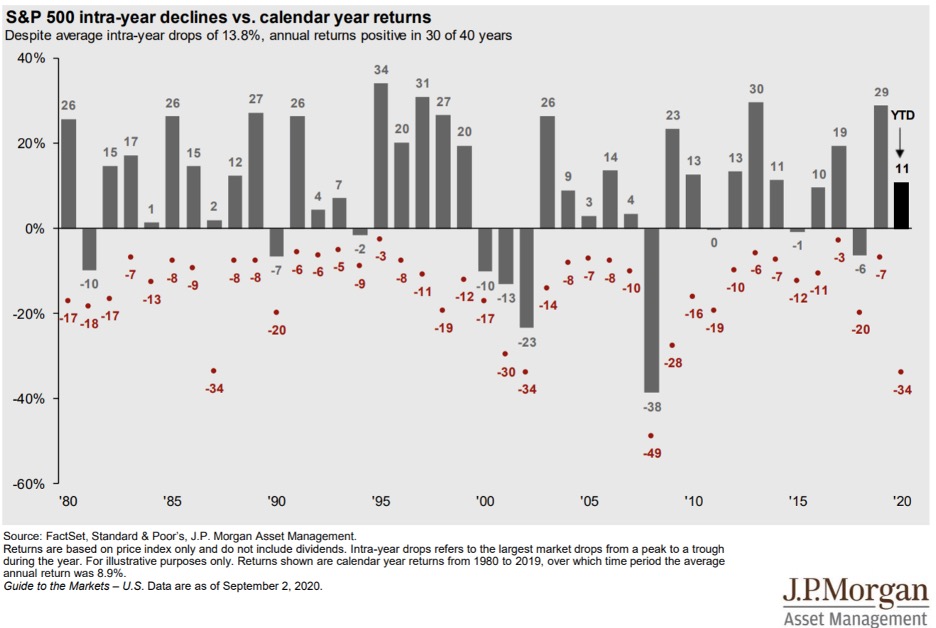

If you fell asleep on January 1st and woke up September 1st, would the selloff and recovery have been of consequence? No. That window of time would have been of consequence only if you needed cash out of your portfolio and you had not raised it prior to the selloff. See “Not appreciating the role of cash” above. Also see the chart below, which is not new to long-time readers but always worth seeing again. 30 of the past 40 calendar years were positive while all years had a loss at some point and the average intra-year loss was -13.8%.

Driving through the rear-view mirror

“XYZ has done great, why aren’t we in it?” This is like picking the winner of the Indy 500 after the race is over and thinking you have special skills. One thing I’ve realized is there are no investing geniuses. I’m not one, you’re not one, and no one on TV is one. If there were such thing as investing geniuses, they’d keep their mouths shut and just quietly keep printing money for themselves from a tropical island hoping no one else discovered their secret. The genius is in THE PROCESS. So, what makes following a process so f-ing hard? It’s boring and lacks the “financial sex appeal” that most people crave. Fortunately, processes are generally simple, straight forward, transparent, and capitalize on compounding along with patience and discipline. The hard part? Accepting that.

Refreshing their portfolio value every thirty seconds

Come on…stop. Unless the answer to the question of “What’s the money for?” is “entertainment,” it’s probably not a worthwhile use of time or emotional energy. For those of you who do it anyway, don’t let it ruin your day or dinner with your family. Lots of people had their 2018 Christmas Eve dinner with family ruined over the market that day…and today, no one gives a shit about the December 2018 correction.

Tinkering with the portfolio instead of tinkering with the plan

Always changing the plan is fine. In fact, since your life is always changing, it may be one of the smartest things you can do. Changes to a portfolio that are a function of a change in planning is completely justified. Changing a portfolio when the planning has not changed is silly. If the answer to “What’s the money for?” has not changed, your portfolio shouldn’t either.

Forgetting what the money is for

Maybe this is a little repetitive at this point, but it was important enough at the time for me to write it down. A lot of people were losing sight of why they were actually investing. One response from April which stood out to me was, “To make more money!” Talk about losing (or never really having) sight of why they were investing!

Thinking there is some sort of an “edge”

I’m firm in my conviction on this last observation…there is no obtainable edge, there are only smart decisions that maximize the probabilities of success through the use of a solid process, patience and discipline.

Let me know if you also learned something about managing wealth this year. I’d love to hear your thoughts and share any lessons you learned in a future blog, too.

Keep looking forward.

What’s Next? Learn about Private Wealth Design:

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument.

Please remember that if you are a Monument client, it remains your responsibility to advise Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request.

Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s web site or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Please Also Note: IF you are a Monument client, please advise us if you have not been receiving account statements (at least quarterly) from the account custodian.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.