Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Three reasons it’s time to reconsider Roth conversions

The benefits of Roth conversions seem obvious: having better control over taxable income in retirement (a Roth may lessen or eliminate your required minimum distributions), possibly paying less in taxes on a withdrawal now than in the future or leaving more money for your heirs to inherit tax-free.

However, when someone insists that a Roth conversion is a no-brainer, my answer is often “Yeah, but…”

It’s not a yes-or-no question, and there’s more to the decision than just tallying up numbers.

Any decision to convert should be considered within the context of YOUR big picture, not someone else’s. There are, however, a few big things happening right now that move me from “Yeah, but…” to a more enthusiastic “YES” when seriously considering Roth conversions as part of a tailored Private Wealth Design.

1. The Obvious: Making Lemonade Out of a Sour Market

While it hurts to look at your IRA statements right now, a shift in perspective can help you see the long-term opportunities for tax and retirement planning. A decrease in gains means you have less money in your IRAs that has not yet been taxed – meaning if you’re converting all or a substantial portion of your IRA, you will generate less taxable income now than you would have if you were considering a conversion just a few months ago, when equity indexes were near record highs. Whether you complete a full or partial conversion, you are being handed the opportunity to let the converted amounts rebound inside of a Roth, sheltering those earnings from future taxes.

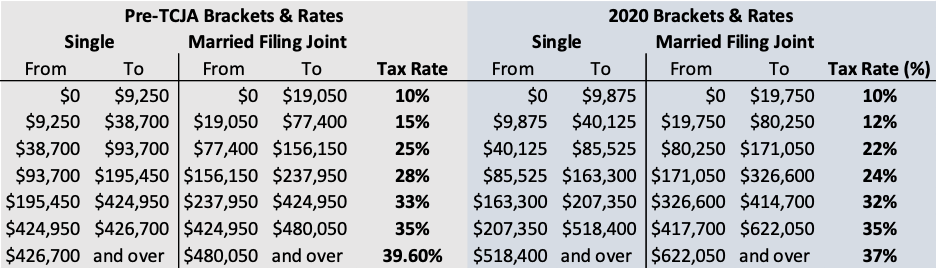

2. The Tax Cuts and Jobs Act

The Tax Cuts and Jobs Act (TCJA) of 2017 may be old news by now, but it provides a compelling reason to convert in the short-term when considered alongside the current market environment. The lower rates and shifted thresholds for income tax brackets are only temporary (see the chart below). Unless Congress acts to extend the provisions of the TCJA, the adjusted rates and brackets will sunset to Pre-TCJA levels after 2025.

Now, I realize that lower rates don’t equate to lower taxes paid for everyone (there’s a lot of pain over the SALT limitations). However, an advisor who is in tune with your unique situation can evaluate your tax landscape as part of your big picture, helping you see your options and understand why it’s worth considering one over another.

Beyond rates and brackets, a reality for many people this year will be the decrease or outright loss of income due to the economic impacts of the pandemic. It is tough to see anything as a silver lining, but decreased taxable income creates a window of opportunity for conversion with less tax impact. A conversion should only be considered if it doesn’t create additional financial stress, and money outside of the IRA should be used to cover the taxes if possible, allowing you to experience the maximum benefit of the Roth conversion.

3. The SECURE Act

IRA owners are rethinking their estate plans with the introduction of the SECURE Act and it’s 10-year rule for beneficiaries. Previously, beneficiaries of IRAs could “stretch” minimum distributions over their lifetime, resulting in smaller taxable distributions and greater wealth accumulation in the form of compounding tax-deferred earnings. Now, beneficiaries are required to fully draw down an inherited IRA within 10 years. This could add to already-high taxable income in prime earning years for beneficiaries and eat away at an inheritance that was intended to last beyond a generation.

While Roth IRAs are not exempt from the 10-year rule, distributions are tax-free for beneficiaries in most cases. Roth inheritances won’t fully avoid the wealth implications created by the SECURE Act, but increasing the amount of Roth money a beneficiary receives may reduce total taxes paid on IRA money—that is, if the beneficiary would pay more in taxes than the IRA owner would on a conversion. If tax reduction on inherited wealth is a primary concern, Roth conversions are worth consideration.

If you have been building wealth inside of tax-deferred retirement accounts, now is a great time to start or revisit the Roth conversion conversation.

Here at Monument, we help our clients through these decisions with a Private Wealth Design. Our Private Wealth Design is a collaborative, creative, customized approach to turning a wealth of diverse opinions, ideas, resources, and investments into a design that represents the life YOU want to live.

A Private Wealth Design may traffic in numbers, but it isn’t paint by numbers – our team of seasoned creative thinkers are here to help design your customized solution.

Let us know if you need help with a conversion or check our website to see if you are a good fit for a Monument Private Wealth Design. While we can’t work with everyone, we know enough great advisors to find anyone the help they need. Just reach out.

Emily M. Harper, CFP®

Vice President & Partner

Emily’s background in the financial industry began after she graduated from the University of Virginia. During a seven-year run in various advisory and leadership roles at a global asset management firm, Emily acquired four industry licenses, a certificate in Financial Planning from UVA, and her CERTIFIED FINANCIAL PLANNER™ designation.

Recent Posts

By David B. Armstrong, CFA

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.