Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Thanksgiving Leftovers

I don’t have any one topic I want to cover today. There were a lot of big macro data points last week, and a lot of great reads. Think of today’s post as some delicious Thanksgiving leftovers, so let’s eat.

My last post was on an investment in our Strategic Income Portfolio (Tanger Factory Outlet Centers, ticker: SKT). Since then, Barron’s published a positive article on SKT, making the case that shares are oversold. Positive Barron’s write-up’s are generally nice short-term catalysts, and the stock was up about 3.0% last Monday, and about 2.4% on the week. Again, this is more of an income story than a capital appreciation story, but it was nice to see shares stabilize a bit.

Monday: An abysmal ISM Manufacturing report.

The ISM Manufacturing report was down for the fourth month in a row and is in negative territory. The reading came in at 48.1 and anything less than 50 is consider negative growth. The last time this happened was November 2015 through February 2016, and before that July 2008 through July 2009. The former occurred in tandem with a meltdown in the energy sector and the latter, of course, was in connection with the Great Financial Crisis. Monday’s ISM news spurred an intra-day trading range of over 1% in the S&P 500 for the first time in 34 days, which is the fifth-longest streak since 1985 (per Bespoke Research). With consecutive negative days on both Monday and Tuesday, the month did not get off to a good start.

Wednesday: More weak data.

ADP Private Payrolls missed expectations, as did ISM Non-Manufacturing (reading of 53.9, so still above the 50 level). When you combine both ISM data points this week, (often referred to as the “Composite”), the November Composite score fell month-over-month from 54.0 to 53.3. Like the others, anything over “50” is still considered expansionary.

Friday: A surprise in non-farm payrolls and unemployment.

Non-farm payrolls were expected to be 187K for November, and came in at 266K, with the unemployment rate dropping from 3.6% to 3.5%. (Dave here: I heard on Friday that this is the best unemployment rate in 50 years, but that was on Fox Business News, so….) Talk about a pick-your-poison type of week for headline data: Weak ISM reports, flip-flops on trade headlines from the administration and a huge payroll beat. The S&P gapped up close to 1% Friday morning.

Energy

- No Brent in Brent. The Wall Street Journal reports that Shell is set to cap their last Brent oil well in the North Sea. This is significant because this field set in motion the creation of the Brent crude benchmark, which is one of two major references used to set prices on commodity futures markets. The other major oil benchmark is WTI (West Texas Intermediate), which represents a “lighter” type of oil that is mainly produced domestically in the U.S.

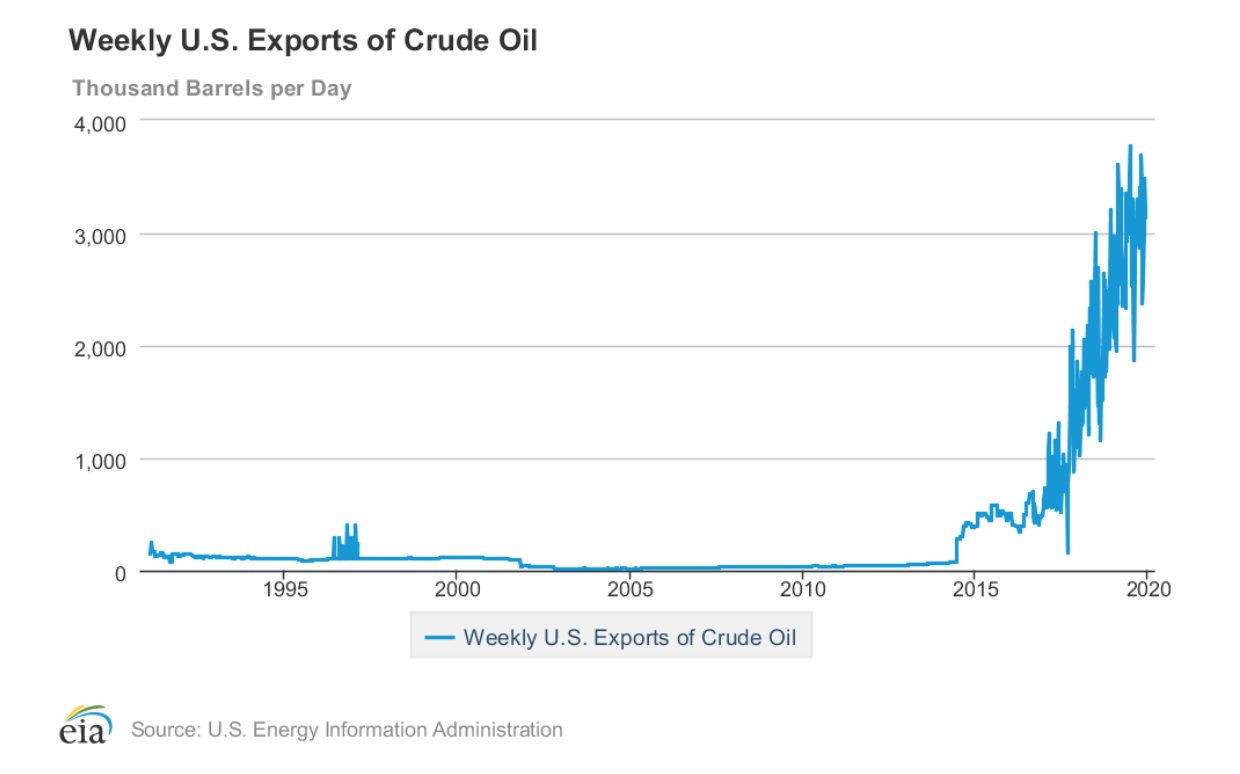

- Speaking of U.S. crude, in September-October, the U.S. became a net exporter of oil for the first time since the stats have been tracked. The graphic below is telling.

- The surge in domestic output – thanks in large part to major shale fields in Texas and New Mexico – is great news for consumers, but not so great for publicly-traded energy on the whole. While the S&P 500 is up nearly 28% year-to-date (YTD) on a total return basis, the Energy sector (as measured by XLE) is up only 6.8%. This is by far the weakest sector performance, with Healthcare the next worst-performing group, up 17.8% YTD. Further, energy now represents only 4% of the S&P, down from the 14% weighting it held in early 2009.

- And here is a shocking stat for you: there are 28 companies in the S&P 500 Energy Sector. Their collective market cap: $1.1 trillion. This is less than the market cap of a single company. Apple. At $1.2 trillion.

- Keeping with the energy theme: if you’re looking for a compelling Netflix watch this week, check out Last Breath. This is the story of a commercial saturation diver who survived without oxygen for 30 minutes at the bottom of the North Sea.

There were a few other tasty bits that I didn’t cover from last week. Namely: mid-cap stocks and the performance of the S&P 500 “after-hours.” Until next time.

Call the Team with any questions—I just wanted to share what Dave and I have been reading and chatting about over the week.

Erin

What’s next?

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

Erin M. Hay, CFA, CMT

Private Wealth Advisor, Portfolio Manager

A graduate of the University of Oklahoma, Erin began his investment management career with J.P. Morgan Private Bank. There, he worked with portfolio managers, traders and asset class specialists to bring tailored investment solutions to his team’s high net worth clients. However, intellectual curiosity would dictate both a change in geography and job description.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.