Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Tanger: Short Term Turkey

Good afternoon everyone!

I’m sure your Thanksgiving preparations are in full swing. I’ll be spending the holiday in Arlington with one of my best friends and his family. We’re going to…a Chinese restaurant. Kinda excited, not going to lie. Don’t fret though: Mom and Dad are FedEx’ing some pies to my apartment, which I will be enjoying with a glass of Barry Switzer wine.

Two brief updates. First: people love to take victory laps whenever they get things right, but it is disingenuous to never write about when things go “wrong,” at least in the short-term. As our clients are aware, we recently made a small real estate (REIT) purchase in our Strategic Income Portfolio, and unfortunately, the position has moved against us over the past few weeks, even as stocks more broadly have moved higher. We are not hitting the panic button though: this is a small position and we’ll give it time to play out. Second: we look at some broad market data that supports our view that the probability of a near-term recession is still low.

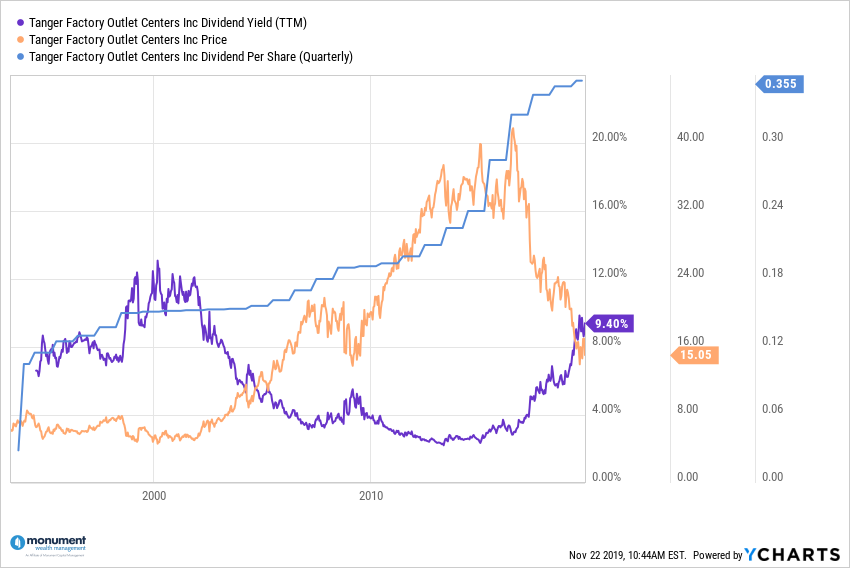

Tanger Factory Outlet Centers (SKT) – Picking the bottom is hard.

For those invested in our Strategic Income Portfolio, we recently swapped out of a bond ETF to purchase a shopping center REIT, to the tune of about 4% of the model. The TL/DR (too long/didn’t read) thesis: we bought a conservatively managed company, with a sound balance sheet, that has sustained or increased its dividend over the last two decades, even in the Great Financial Crisis.

As the “Amazon Effect” has battered retail-focused mall REITs, Tanger has gone along for the ride, and we took a small position at what we think was a good discount. But since we purchased earlier this month, SKT has lost about 10%, so it warrants a blurb.

The Strategic Income Portfolio’s primary goal is consistent dividend income, with a secondary goal of capital appreciation and even then, with no real time horizon for in mind. While nobody wants to see a stock they own go down – particularly over the last several weeks, when the broader equity markets have reached new all-time highs – know that the dividend, as long as it is maintained, acts as a buffer against market volatility.

We will continue to hold this stock so long as fundamentals dictate a high probability of maintaining or increasing the payout, knowing that there are often bumpy price movements along the way.

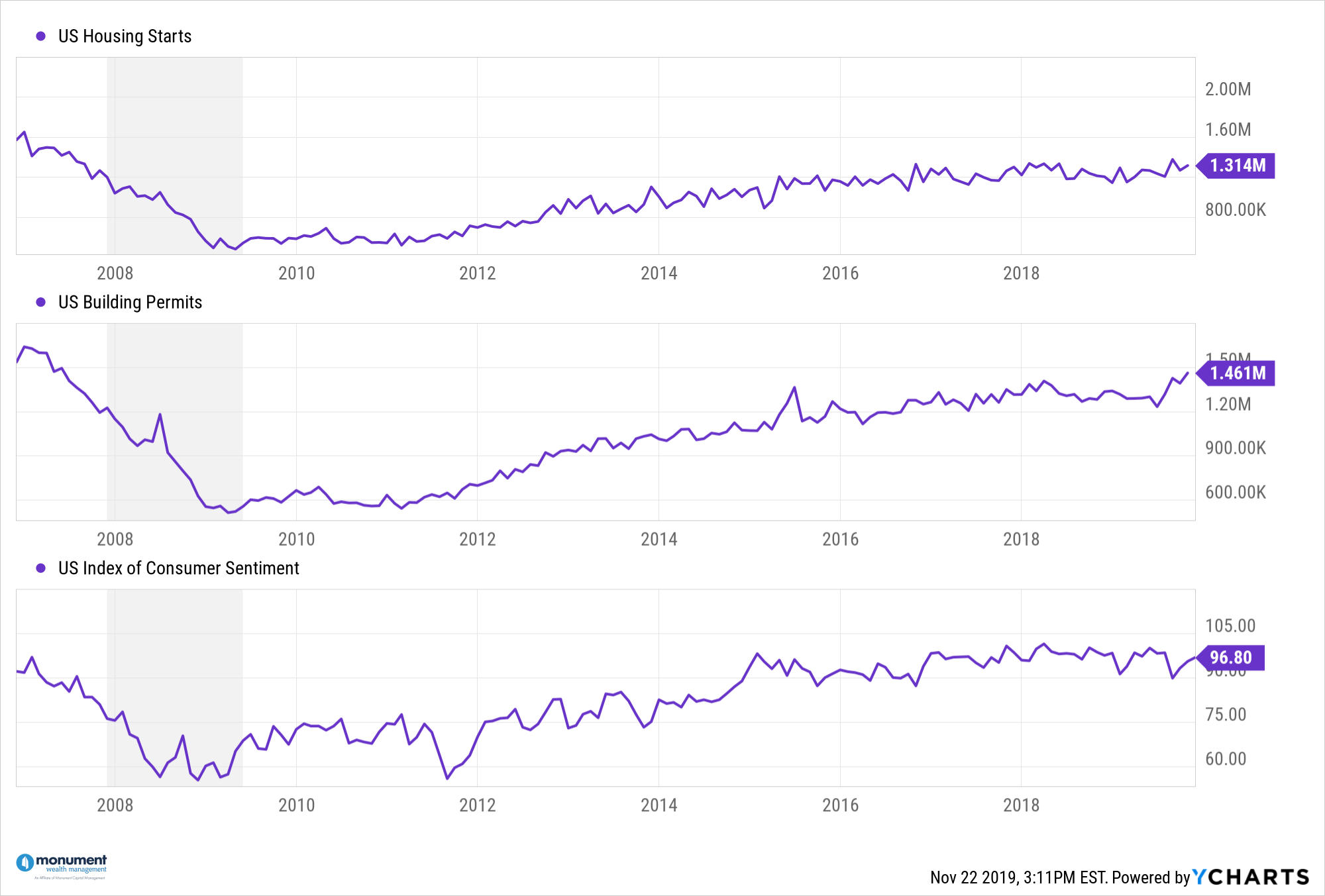

Macro data points.

Long-time clients are aware of our MONCON recession indicator, which Dave has written about here and here. While we continue to be in MONCON 5, there are some other data points that caught my eye over the last week, and reinforce our opinion that a recession, while inevitable, is not likely in the short-term.

Ned Davis Research recently published a piece with their own (simplified) checklist, which includes a combination of yield curve inversion metrics, S&P 500 margins, unemployment and consumer sentiment. None of those metrics are flashing red. Elsewhere, building permits are at their highest levels since 2007, and housing starts, while weaker than analyst forecasts, remain near their highs. Lastly, we are at the tail end of third quarter earnings. While earnings growth is slightly negative on a year-over-year basis, the number of companies reporting both revenue and net income above analyst estimates is above their respective five-year averages.

In short: things look pretty good. As always, things can change in a hurry, which is why we preach that clients have 12-18 months of cash at their disposal, to weather downturns and avoid selling at troughs.

What’s Next?

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

Erin M. Hay, CFA, CMT

Private Wealth Advisor, Portfolio Manager

A graduate of the University of Oklahoma, Erin began his investment management career with J.P. Morgan Private Bank. There, he worked with portfolio managers, traders and asset class specialists to bring tailored investment solutions to his team’s high net worth clients. However, intellectual curiosity would dictate both a change in geography and job description.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.