Recession and Emotional Fire Drill

Something that has people worried right now is all the talk about the yield curve and its predictive value for calling a future recession. But is it really that great of a tool?

To start, let’s look at what are considered leading economic indicators. Here’s a list of the ten components of The Conference Board Leading Economic Index (LEI) (for the U.S.) straight off their website:

- Average weekly hours, manufacturing

- Average weekly initial claims for unemployment insurance

- Manufacturers’ new orders, consumer goods and materials

- ISM Index of New Orders

- Manufacturers’ new orders, nondefense capital goods excluding aircraft orders

- Building permits, new private housing units

- Stock prices, 500 common stocks

- Leading Credit Index

- Interest rate spread, 10-year Treasury bonds less federal funds

- Average consumer expectations for business conditions

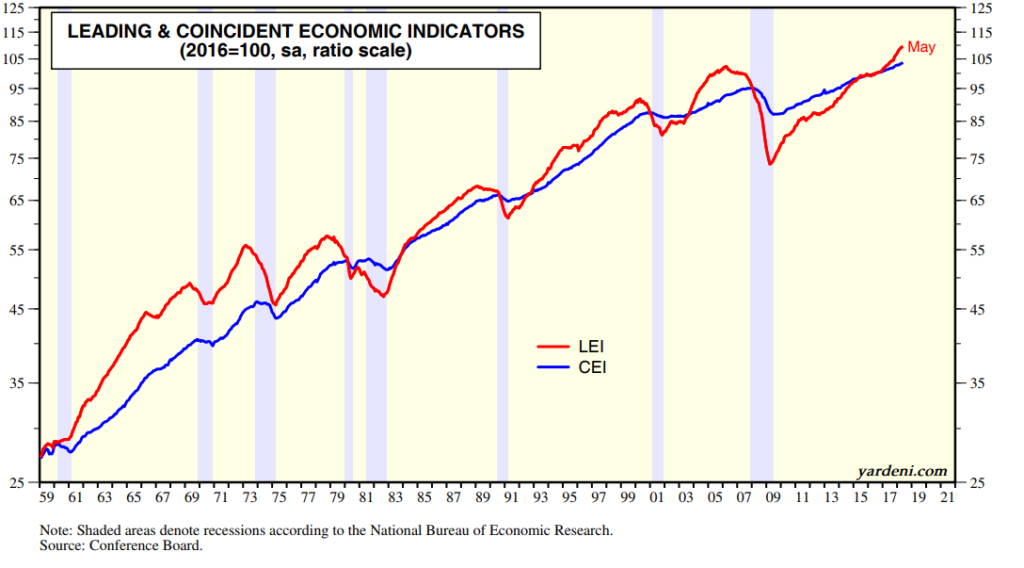

Ed Yardeni recently published the chart below of the index. The red line is the Leading Economic Indicators (index) and the blue is the Coincident Economic Indicators (index). Shaded areas are recessions. The May reading is a record high…please note that the red line turns down before recessions.

The LEI is not flashing a red flag.

The main thing I want to point out is number 9 on the list, which is the interest rate spread between the 10-year Treasury bond and the current Fed Funds rate. The difference between the two is a common interpretation of the Yield Curve. (Another popular interpretation that is more routinely referred to is the difference between the 10-year Treasury and the 2-year Treasury. You will see that referred to in the chart down below, but stick with me for now.)

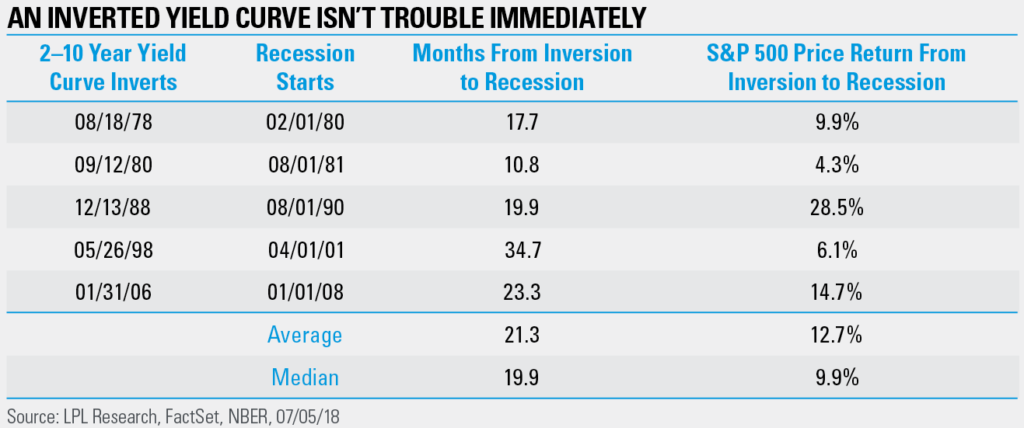

There is and will be a lot of talk about the Yield Curve in the press, yet it is only one component of the LEI. That’s not to say it’s unimportant – in fact, it is a great predictor of a recession. According to LPL Research, “Inverted yield curves have a perfect history of predicting economic recessions over the past 50 years, with nine of the past nine inversions followed by an eventual recession.”

What it’s NOT good at predicting is WHEN. Note the use of the word “eventual” in the above quote.

I want to point out that “flattening” is not the same thing as “inverted”. A lot of growth can happen during the time that the yield curve is flattening/flat. For example, take a look at the mid to late 1990s.

More from LPL Research Senior Market Strategist, Ryan Detrick:

“Here’s what you need to know: an inverted yield curve isn’t this end-all sell signal that many make it out to be. In fact, looking at the past five recessions, economic growth continued to accelerate for an average of 21 months after the yield curve inverted, and the S&P 500 Index added nearly 13% on average—rising in every instance—before a recession officially started. We aren’t ignoring this potentially troublesome sign, but it doesn’t appear to be the major warning many make it out to be.”

My point to clients and other readers is this…

Inversion happens well in advance of a recession starting. During the window of time between inversion and recession, the average return (above table) is 12.7% with a median returnof 9.9%.

Why does that happen? Because the other 9 LEIs are still strong and the economy still has growth left in it.

An inverted yield curve would be troubling and it is a red flag worth heeding. However, that’s different than panicking, which some people are going to do and the market will experience a sell off when that happens. Be prepared for that volatility, because it will lead the news cycle if it happens.

I don’t think we are headed to a recession anytime soon. One will come again for sure, but it’s probably not inside of the next 12-18 months. The data are just not there to support one happening that quickly.

As always, we have our eye on things, but we are not changing the DEFCON level at this time.

When the DEFCON level does change, investors with a proper Private Wealth PlanSM will be fine because they have the cash they need set aside to ride out any volatility. Adjustments will be made inside the Monument portfolios as the DEFCON level changes, but that’s taken care of operationally as a matter of portfolio management.

Use this opportunity while things are okay to run an “emotions fire drill.”

Ask yourself if you woke up tomorrow and the market was down 10-20% from today, would that cause you serious harm? If the answer is yes, please call us. It probably means you need to raise some cash to cushion things and keep you from selling at the worst time. If the answer is no, remember we will see an eventual recession and resolve yourself to ride it out because those who do ride it out always emerge on the other side in good shape.

Process, patience and discipline. Those are the silver bullets every investor has at their disposal.

Everyone should have a plan that they are comfortably committed to. If you are not a Monument client and lack a process or plan, we can help. If you lack patience and discipline, we can help too by showing you the data that highlights the benefits of both. String all three together – that’s how Buffett does it.

Earnings season is starting soon. I suspect it will be a good one once again. I’ll have blogs soon on the trade war issue and earnings as they start to make some meaningful announcements. The teaser is that if you think there is going to be a trade war, good…I’ll explain why in the next blog.

Keep looking forward,

Dave

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.