Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

How Long Can This Market Keep Going Up? (Oh, and Does it Really Matter?)

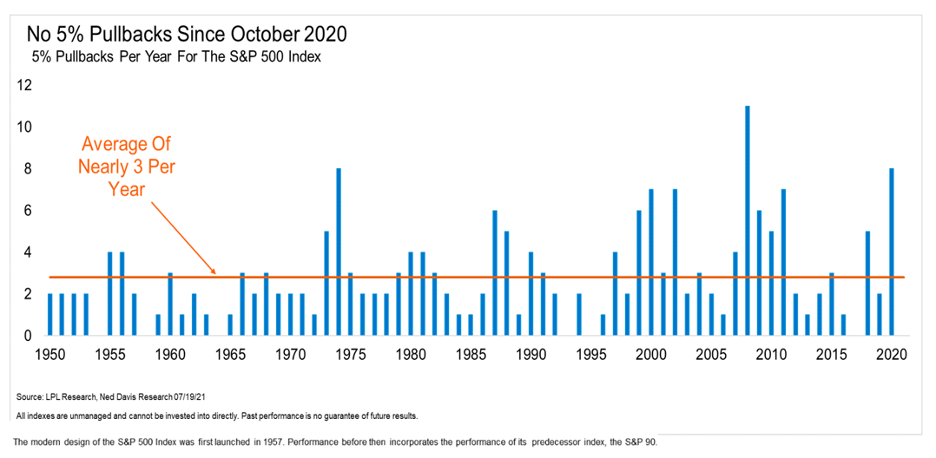

Whenever the stock market goes up for a long time without any sort of significant pullback, the natural question that we start to field is, “How much longer can this go on?” At this point, it would have been natural to expect a 5% pullback in the market, given how often they happen.

In fact, on average, we should expect a 5% pullback to happen three times a year. Yes, A YEAR.

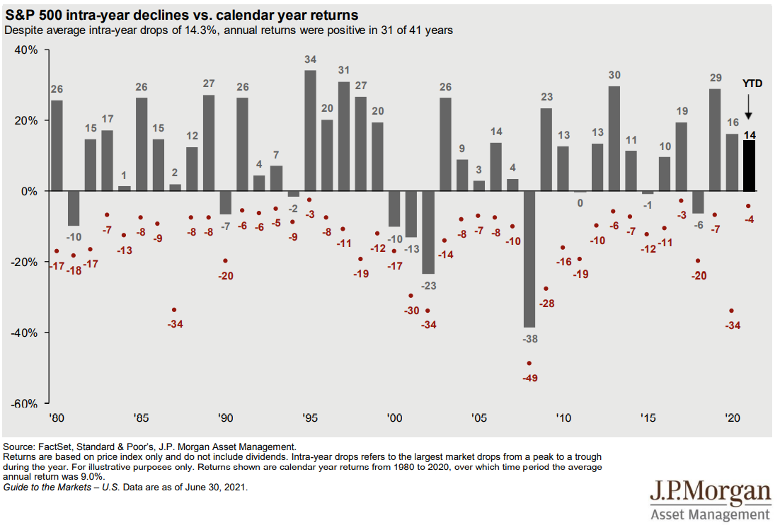

But remember, while “on average” is not the most useful statistic for an investor (or prognosticator), 5%, 10%, and 20% pullbacks do happen. Below is a decent chart that shows intra-year declines (red dots) for the S&P 500 over calendar years along with the actual calendar year return. With an average intra-year drop of around -14%, 75% of the 41 calendar years in the chart ended up with positive returns (Source: JP Morgan Asset Management).

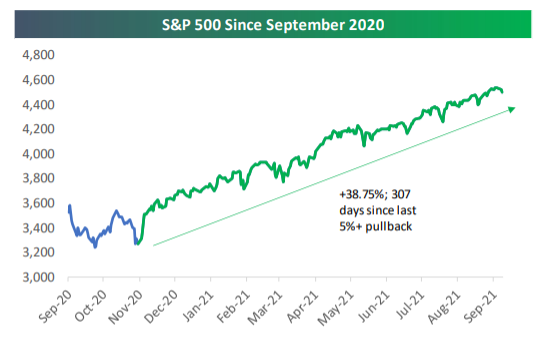

At this point, the S&P 500 has gone about 307 days without a 5% decline. And over those 307 days, it has advanced approximately 39%.

So 307 days without a 5% pullback resulting in an increase of 38%.

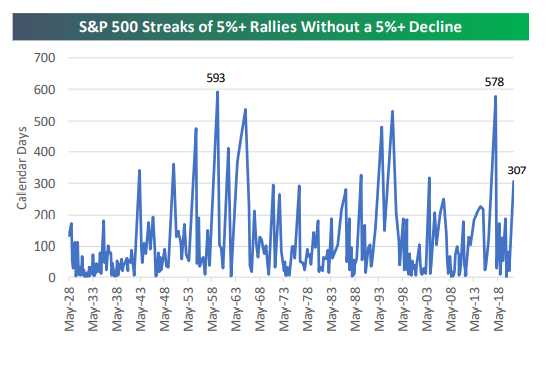

So, while 307 days is certainly a long time, it is also not without precedent. As early as 2018, investors enjoyed 578 days without a 5% or greater pullback, and the longest streak was 593 days, but you have to go back to the 50s to find that. Keep in mind that those two streaks are close to two times as many days as the one we are currently in.

So what?

You never know what you don’t know. Translation: your gut is not a good gauge for anything, so here are the things you should be doing now:

- Raise cash you think you may need over the next year. This allows you to ride out any market pullbacks without having to react—bonus points for feeling good that you raised cash near an all-time high and brag to your friends. (I won’t even ask for credit…just run with it and savor the glory.)

- Run a “Fire Drill”. If you had $1 million in a portfolio of stocks and woke up tomorrow to a 20% pullback, how pissed would you be on a scale of 1-10 (10 is the most pissed) at losing $200,000 overnight? Raise cash until the actual dollar loss would put you at a 4.9.

- Now double-check the dollar amount associated with your 4.9 and realize the portfolio will need to go up 25% to make you whole again. If your score went up, sell more to get back to 4.9

- Check your concentration. Are you exposed to a few big names in your portfolio that could cause you to lose more value on a percentage basis than the corresponding market pullback? Fix that, because, as the ice age proved (and no, Dean was not alive back then), you don’t need a lot of force to create a ton of damage.

- If you have corrected everything above or were all set and require no adjustment, there is still something you need to do…let compounding do its thing. Remember, compounding doesn’t depend on BIG returns. It simply needs sustained, unbroken GOOD returns over a long period of time. And unbroken means holding through the periods of pandemonium and turmoil.

- Finally – get the big things right. Preventing one big, mistimed mistake can do more for your lifetime of investment returns than getting dozens of small choices (guesses) right. For more on that, be sure to check out our upcoming Podcast where Jessica and I host Emily Harper on this topic.

You knew we have a Podcast, right? Check it out in our Resource Center, on Apple Podcast or search for Off The Wall on your favorite podcast player.

Keep looking forward.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

Recent Posts

By David B. Armstrong, CFA

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.