Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

When Perceptions Change, Should Your Portfolio Change, Too?

The markets were surprised by Trump’s tweet last Sunday declaring he was raising tariffs from 10% to 25% on the initial $250 billion of Chinese imports…and implementing tariffs on the remaining $300+ billion as well.

However, this should not be a big deal to many of our readers. Those who don’t need cash right now are just fine.

Here’s the plain old, straightforward truth…We don’t know what will happen, nor does anyone else. As investors, we must all hope for the best while continuing to plan for the worst.

Investing Behavior

We all know by now that uncertainty surrounds us here in investing land. Learning to accept that is instrumental and important when creating an investment strategy. I’ll go out on a limb and claim (admittedly with zero factual evidence to back it up) that every investment strategy ever invented has bombed at one time or another even if it has been successful over the long run. That includes the strategies at Monument along with the strategies created by the smartest investors out there. Even Buffett.

Why? Because of human behavioral traits. We all have them. They are fostered by the racket we are exposed to on a daily basis.

Learning to filter out the racket is key. Some things are important, and a lot of things are not. This last week was a perfect example. We’ve had a great market and that puts everyone on the lookout for a pullback…it’s the “itchy trigger finger” syndrome.

I think we’ve experienced a lot of over-reaction to news that has no immediate discernible outcome.

In other words, what’s changed? I know there is a lot of speculation that things COULD CHANGE, but really…what’s changed?

What HAS really changed? Perception. To some—let’s call them the “undisciplined” or the “impatient” investors—perception means everything. To others, it means nothing.

If you have a well-diversified portfolio, there will be a time when you hate something you own. But for those of you who have come to terms with that, you have an advantage. You’re like the casino that wins over the long-term because the odds are in their favor 51/49. Time and statistics are on your side.

As situations arise things can and should adjusted if the answer to the question, “What’s the money for?” changes. But investors must avoid the natural tendency to “do something” when the news noise gets loud. Those who get caught up in trying to time the market or adjust based on changing perceptions will wind up driving their portfolios into poor overall returns.

For a refresher, please read the “What to Do Now” section found at the bottom of this post from December 20th, 2018. Do you remember the markets back then? Oh hell, go read the whole thing again, it’s one of our top–rated blogs of the last 12 months.

Perception or Reality?

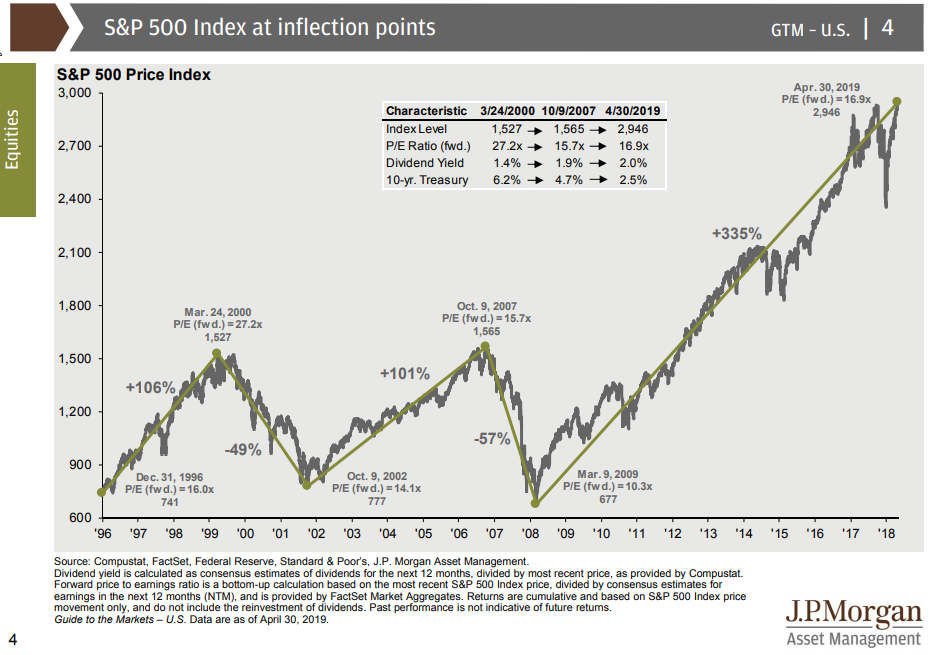

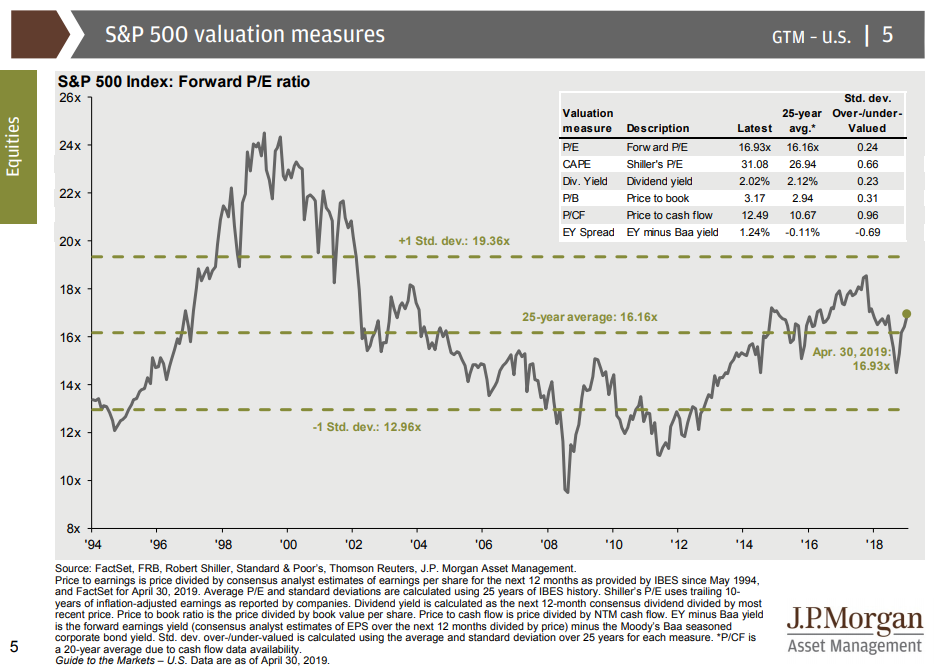

To conclude, I have a few thoughts based on the slides below. (Data is as of the end of April 2019.) I’ll keep the commentary to a minimum…just look and ask, “What has changed—perception or reality?”

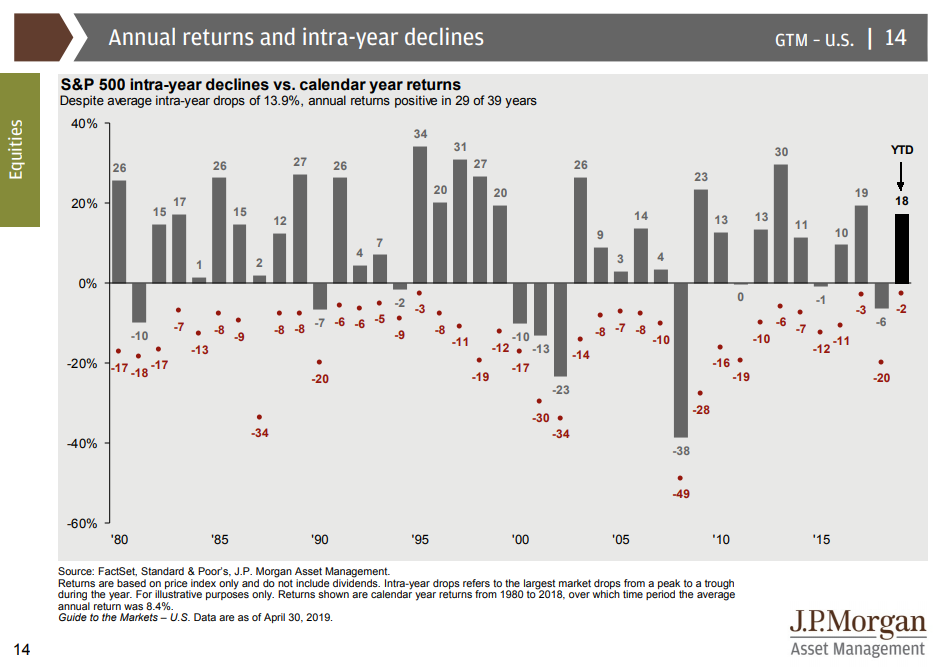

The last slide is the “shit happens” slide. Okay, fine…I do have some comments, I can’t help myself.

Every

Single

Year.

Something

Shitty

Happens.

Just look at the red dots and the section of the slide that reads, “Despite average intra-year drops of 13.9%, annual returns are positive 29 of 39 years.” Those are good odds, especially when you consider that casinos make huge profits off a 51% advantage.

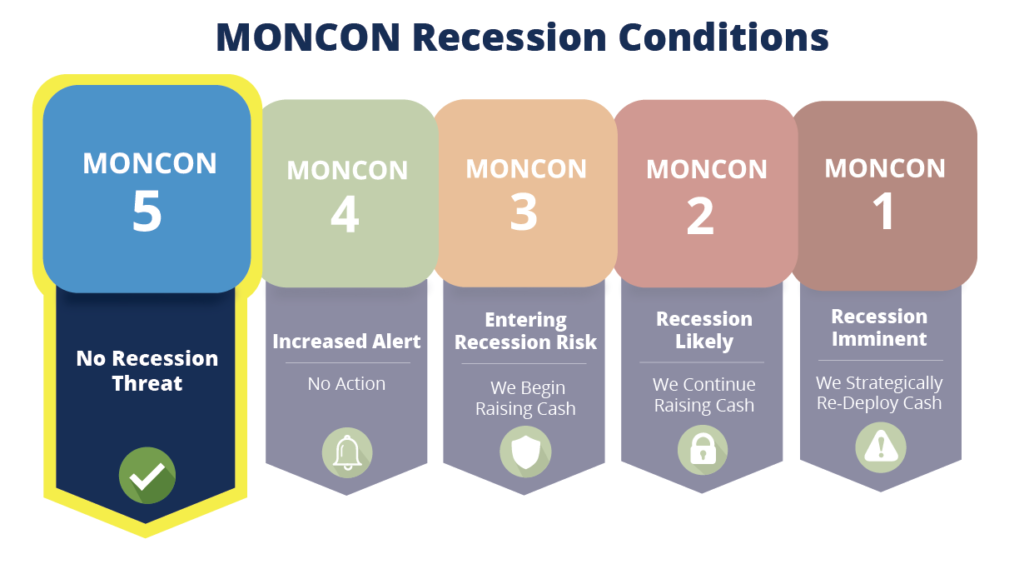

MONCON Recession Watch

We are still at MONCON 5 for recession watch. If that sounds like a broken record, good. It should. If you were trying to adjust your portfolio over the past 6-8 months based on noise and changing perceptions, you probably got hurt in the market. For those of you ignoring it (like the MONCON model does), you have stayed in the market and have probably made money despite last December and last week.

Keep looking forward.

Dave

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.