A Spooky Week on Capitol Hill

This post is part of our ongoing series about tax reform proposals and what they may mean for you. We’re also sharing opportunities you should explore before tax laws potentially change.

Are Americans in for a trick or a treat this Halloween week? Spooky things abound – not witches or goblins but the specter of tax changes that may accompany the spending bill currently being negotiated by the Senate and the House of Representatives with President Biden. The scary part for planners like me (we crave certainty) is the unknown: we still don’t know what will make it into a framework for spending, who will be impacted and to what degree, and when. We do know that we likely don’t have a lot of time before changes take hold.

WARNING: Negotiations on the Hill are moving at a dizzying pace – This blog is being published October 27th, 2021, and by the time you read this, it is possible that a framework will be available, and we’ll have a better sense of what makes it into a final package. A framework does not mean that this becomes the law of the land – it will give us an idea of what legislation to be voted on will look like and is a necessary step for the bi-partisan infrastructure bill (currently being held up by this reconciliation process) to move forward. However, a framework is likely to reflect the various conditions that holdouts on the larger spending bill can live with.

While the pace of change and degree of uncertainty can feel overwhelming, focusing on the things we can control, largely our own behavior and decisions, can lessen the anxiety. By thinking in probabilities and focusing on what is most likely (or unlikely) to change can help us narrow in on opportunities to consider before time’s up.

What May Be Likely?

The amount of money the government will need to raise by taxing individuals and corporations to cover spending will depend on how much spending Congress can agree to – while we are full of opinions at Monument, this isn’t a matter of opinion. What started as a $3.5T wish has likely slimmed down substantially to around $1.75T, reducing the amount of revenue in the form of income taxes that needs to be raised to pay for the spending.

Some Senators are opposed to increasing taxes on high income individuals and families (but billionaires might be a different story …if you didn’t start a company to launch yourself into space I wouldn’t worry about this headline too much). With a slimmed down spending number, it’s possible that major changes to individual tax rates initially proposed won’t be necessary.

It is easier to adjust amounts and thresholds within the existing income tax code than to create entirely new taxes, so it may still be likely that some revenue will be raised by:

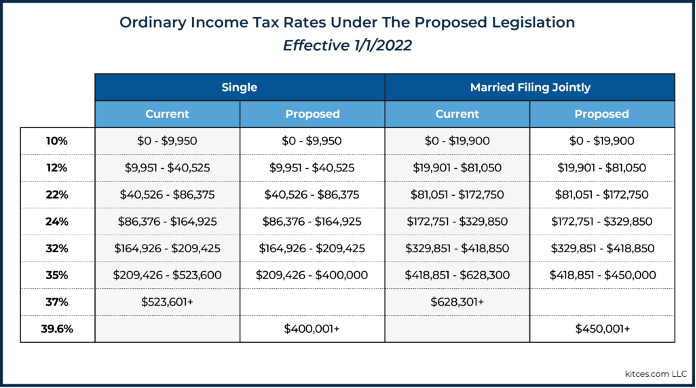

- Increasing the top marginal rate for high income individuals and families to 39.6% at lower thresholds of income (the House Ways & Means Committee proposed $400k for individual filers and $450k for married filers – Senators opposed to tax increases may take issue with these thresholds especially for married couples). If passed, these rates would be effective for 2022. See this chart from Kitces.com.

- Increasing the top long-term capital gains rate. Congress gave an early “treat” here by proposing a much lower capital gains rate than President Biden’s proposal. The current proposal in the House would see a top rate of 25% for individual and married tax payers at $400k/$450k in taxable income respectively. Look out for the additional 3.8% net investment income tax as well for a total of about 29% (still more generous than the 39.6% Biden suggested at income above $1M). If passed, this may be retroactive to gains realized after September 14, 2021.

There are a whole host of other potential changes, including a reduced lifetime gift and estate exemption amount (down to around $6M from the current $11.7M per person under the Tax Cuts and Jobs Act) and provisions surrounding the inclusion of Grantor Trusts in the taxable estate. There’s no shortage of analyses on these complicated topics – ultimately they represent a relatively small amount of the revenue needed to offset spending but are easy targets when you have an “adjusting thresholds” philosophy.

What Can or Should You Do?

There’s no way to cover every single proposal in a single blog post, but those surrounding personal income tax rates and capital gains rates are likely to be the most wide reaching and most impactful in day to day lives.

If you are concerned that you may be subject to higher taxes going forward, the best way to ease your anxiety is to test the impact of higher tax rates on the probability of success of your Private Wealth Design. You may find that the monster in your head isn’t as scary when your probability of success still points to a viable outcome given your personal goals and objectives. That doesn’t mean you have to be happy about paying higher taxes, but at least you’ve taken control and removed the ability of the unknown to cause stress or anxiety. Give us a call if you can’t sleep at night and we’d be happy to stress-test your plan.

If your goal is to minimize taxes on income as much as possible or take advantage of current rates as they are, we suggest:

- Looking for ways to realize income in 2021 – Can you accelerate a bonus into calendar year 2021? Are you sitting on unexercised stock options from your company that you can exercise at current ordinary income tax rates? This can be especially meaningful if you are at a current marginal rate of 32-35% since taxpayers in these brackets will see the most dramatic change as income crosses $400k/$450k.

- Pushing deductions into 2022 if possible – As your tax rate increases, itemized deductions become more valuable. Your charitable giving strategy is largely under your control in terms of timing and how to give – in a world with higher marginal rates AND higher capital gains rates, donating appreciated securities in lieu of cash is worth another look.

- Maximizing easy tax-deferral opportunities in 2022 and going forward – In addition to pre-tax 401k deferrals, don’t overlook Health Savings Accounts (HSAs) where possible. If a high deductible health plan is an option for you, contributing to an HSA comes with a triple tax benefit.

- For self-only coverage, a deductible contribution of $3,600 can be made, while family coverage allows a deductible contribution of up to $7,200 (regardless of whether you itemize deductions or take the standard deduction).

- Earnings grow tax-free and tax-free withdrawals can be made to cover medical expenses, or for any purpose after reaching age 65.

I’d like to have a crystal ball and tell you precisely what will happen, but no one can deliver tomorrow to you today. Our Team can help you understand potential tax changes in the context of YOUR big picture and share our opinions on which options are worth considering as Congress sprints toward the finish line. Here’s to hoping your Halloween and beyond are full of more treats than tricks.

Emily M. Harper, CFP®

Vice President & Partner

Emily’s background in the financial industry began after she graduated from the University of Virginia. During a seven-year run in various advisory and leadership roles at a global asset management firm, Emily acquired four industry licenses, a certificate in Financial Planning from UVA, and her CERTIFIED FINANCIAL PLANNER™ designation.

Recent Posts

By David B. Armstrong, CFA

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.