Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

A Real-Life Client Critique of Monument

I recently published two quick videos on some thoughts I had about the economy. We put them out on social media but are still working on the best way to get them out through the blog. Here they are:

Three Quick Thoughts on the Market | July 12th

Are You Still Moving Forward? | July 16th

I’m working on better audio, but also want to make these really easy to do and not overproduced. Keep looking out for them. You may see them on social media faster than the blog so be sure to follow us on LinkedIn, Twitter, Facebook, YouTube and/or Instagram.

I recently received an email from a routine reader of our “Off the Wall” Blog. The general thesis of the note was a challenge to our convictions. It reads like an argument, but you have to know our relationship to understand it’s not. This is just us being us – we are friends, and we both stand strong and speak plainly. He gave me permission to use our back and forth as a blog. In fact, he was the one who suggested I use it as a blog.

The original was seven pages in a Word document. I thought it would be useful to share a few of the points for two reasons: 1) in case any readers misunderstood any of our positions or convictions and, 2) in case anyone needs a refresher or new readers are just now joining in.

His statements in italics are extracted from the original email and my replies underneath. I’m only slightly editing the answers for formatting, context clarity and some brevity. I’ll [bracket] any edited portions.

“Your themes in general are reiterating to the investor that staying long over time is a winning strategy.”

- You are reading that I’m saying, “stay long” when I am actually advocating “staying fully invested”. They are two different things.

- I interpret staying long to mean blindly buying and holding, generally equities, regardless of the economic reality and environment.

- Being and staying fully invested means you have a Private Wealth Plan, an Investment Policy Statement (IPS), a strategic asset allocation and have forecasted to the best of your ability when you need cash.

- Cash is not only an investment and an asset class—It’s also the ultimate hedge…and it costs nothing. Especially when compared to the 2/20 expense structure of so called illiquid “hedge funds”.

- Being fully invested like that [Dave here: “like that” meaning with a Plan, IPS, appropriate asset allocation and identified cash needs] in low expense strategies that are as tax efficient as possible…THAT is the winning strategy.

“In the overall view, you and I differ on where we are in the cycle.”

- You claim we differ in opinion over the cycle…but you don’t define a cycle. So, I can only respond with this:

- My definition of a cycle is the 4-stage big picture – i.e. 1) we are in an expansion, 2) we are slowing, 3) we are in a recession, 4) we are coming out of a recession. I suspect your definition is much more granular

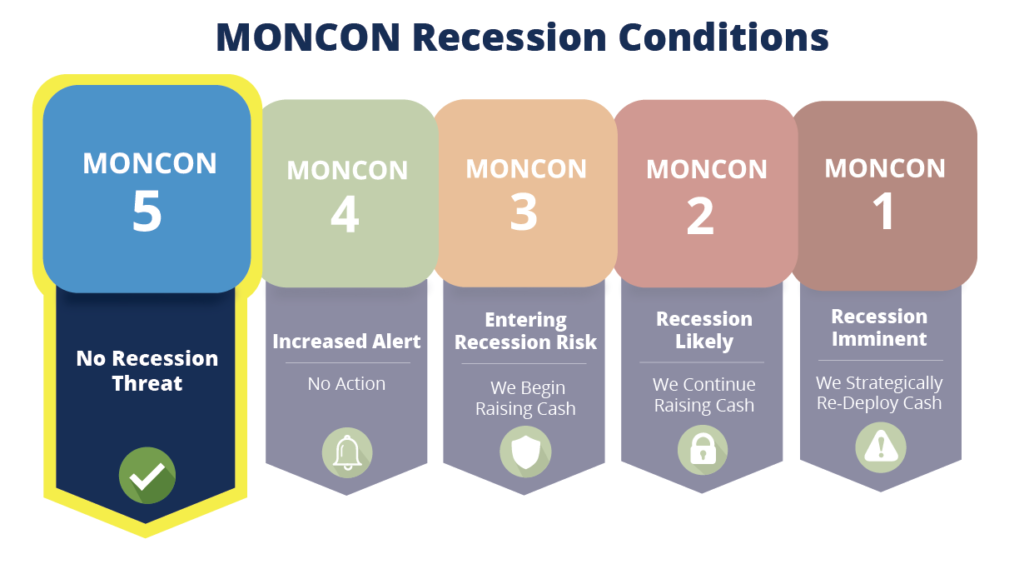

- I ABSOLUTELY track my definition of the cycle and will adjust portfolios accordingly. Please reread my MONCON model blog where I explain EXACTLY what I collect data on, model, and use to determine if the PROBABILITY of a recession is increasing. If the probability is not increasing beyond a pre-determined trigger point, each client’s portfolio stays fully invested per their [Plan]. Once MONCON changes to a specific trigger point, we will start raising cash as a hedge.

- Please remember my drumbeat of reality here: A slowing economy is not the same as a recession. Reference 2015-2016 and the flat returns in the equity markets. My clients who forecasted the cash they needed during that period of time didn’t have to react to the economy slowing down; we were able to stay fully invested and participated in the ride back up before most market timers could get comfortable enough to get back in. That goes for 2015-2016, but also 2008-2009, 2012, and the fourth quarter of 2018. Remember – cash is the best and cheapest hedge available if you plan for allocating to it.

- You are being critical of my convictions and advice simply because it is not as reactive and tactical as you believe it should be, even though I have been right. We have not had a meaningful economic change that warrants any investment change based on the way we model our hedging strategy!

“In my opinion, every financial advisor should be talking about the cycle and what might be around the corner. Pounding the long-only strategy doesn’t take much effort.”

-

- First – I am talking about the cycle! You just aren’t reading it with the same definition of cycle or are dismissive of my analysis. Not acting is not the same thing as not analyzing! In fact, it takes a massive amount of analysis and conviction NOT to fall prey to “if’s” and “buts” because I don’t believe those things are knowable!

- Second – I AM talking about what’s right around the corner, it’s just that I believe that corner is no closer than [6-8 months] out. You and I are just looking at different corners.

- I am “pounding” the advice which is most applicable to where I think we are in my definition of a cycle. Maybe the fact that you don’t agree is clouding your ability to see my perspective. Which is unfortunate because the opinions that are most different from yours are the ones that are probably most worth heeding.

- Unless your other holdings are 100% cash, [I suspect] you ARE actually listening to someone else’s advice and research and investing with them and not me. That’s okay – I have no real problem with that. I know that I don’t have to resonate with everyone, I just have to resonate with SOMEONE. And I’m okay that it’s not with you. I mean that.

- Go to the Monument Blog page and pull up one June blog going back each year… better yet, since I’m on a roll, let me just do it… 2018 / 2017 / 2016 / 2015 / 2014 / 2013 / 2012 / 2011 / 2010. Admittedly, the opinions are not as strong back in the early days since we were not an RIA until 2013. And frankly, I was newer to blogging and was doing more “market recaps” than market and investing opinions. My track record on filtering current financial news topics OUT of our investing strategy has been spot on.

- I don’t confirm your biases, theses, and analyses, so it is completely natural that they do not resonate with you. This is fairly common, actually. Confirmation bias is when we choose to reinforce our own beliefs by seeking out information that supports what we believe to be true. It’s why Dems generally watch MSNBC and Republicans watch Fox. [THIS IS] EXACTLY WHY I RUN THE MONCON MODEL—because otherwise I will seek out the information that validates MY theses and desires to be right. Being rules-based is my savior here.

I appreciate him very much. He knows this emphatically. We will play golf soon, he won’t give me any strokes and I’ll lose money until we go double or nothing on the last hole. Then he’ll give me one stroke and I’ll rise to the occasion.

My perspective on my conviction and what we do and who we do it for it unshakable. I like to say to people, “We don’t need to resonate with EVERYONE, we just need to resonate some SOMEONE.” Here’s a real life statement on my perspective…Phil Knight said recently after Nike was blasted for their position on Kaepernick and the Betsy Ross flag, “It doesn’t matter how many people hate your brand as long as enough people love it.”

Thankfully, that ratio is really in our favor.

Here’s one of the things that makes us different – we have our heads screwed on straight here at Monument. We are humans, so we are obviously fallible, but we do our level best to make sure we set a steady course for our clients. We focus on getting the “few big things” right for them because we know they are the most important things. Being right on the margins is fun to brag about but many times it does not move the needle in real life.

We help people, and that feels good. It’s why we all love what we have built here, and we stand proudly on that. Sure, we measure the standard things every business measures to gauge how well we are doing, but the best measurement came from a meeting last week where a client said, “I have two people I want to introduce you to who have asked me who we use. I think you can really help them.”

There’s no line on the balance sheet that shows you “referral goodwill” and there is no line on the P&L that shows “Pride”.

Keep looking forward,

Dave

We remain at MONCON 5 – DO NOT CONFUSE WEAKENING GROWTH WITH RECESSION – Slow growth is still growth. We continue to labor to find overpowering substantiation of recession in the short term, despite the Yield Curve showing some warning signs. It’s important to remember that lead times to recession from yield curve inversions are very long and widely dispersed, making this less than useful for timing purposes.

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.