Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

A Long Nap – I’m Woke

It’s really important that investors understand what has happened over the past two months. Ask yourself, do you even remember what caused the Christmas Eve sell off? If you do, do you still possess fear over that issue?

Furthermore, what were your emotional reactions? I suspect there was a lot of fear and anxiety – and that’s understandable. No one likes to see account levels decrease even when you fully understand that markets do not go up in value in a neat, straight, 45-degree line on a graph over time.

Here’s another question: what is your emotional state now? I suspect a lot less anxious and maybe even indifferent.

That’s because losses hurt twice as much as gains. The market falls 10% and everyone, especially the media who gets paid fat cash to draw in viewers, freaks out. The market gains 10% and it’s, “Ehhh, that’s cool…did you see that YouTube video called “The Can Opener Bridge”?

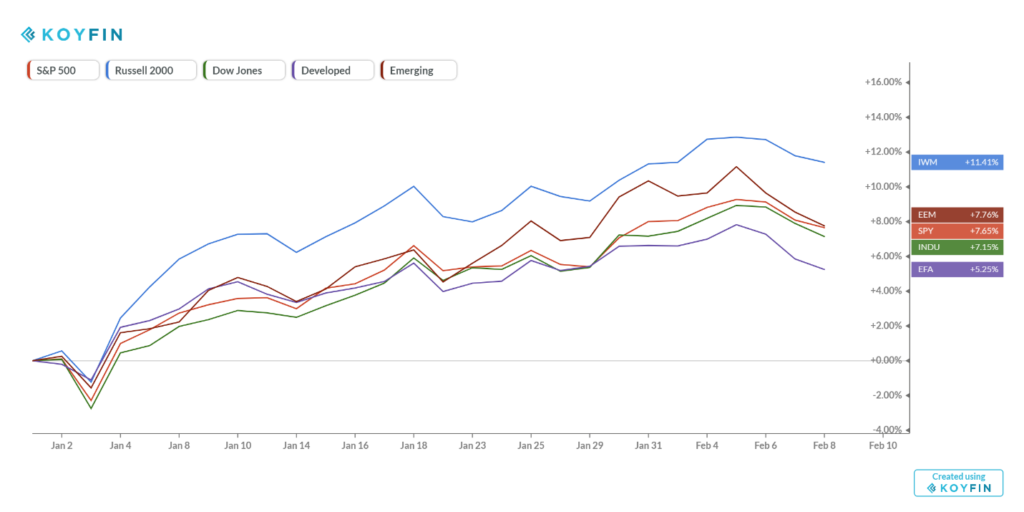

Just so you know, here’s how things look year-to-date (as of 2-8-19).

In a blog post titled “Trump and the Tariff Man” published back in December 2018, I wrote that the best research and thinking is found on Twitter and in blogs rather than through “one way content” such as research reports from big Wall Street firms or media broadcast across the Twitter universe.

Idiots and charlatans on Twitter don’t get respect and don’t get followed. In fact, they get called out…sometimes viciously. Conversely, CNBC and other traditional media sources rely on capturing eyeballs to drive advertising rates through sensationalism, hype and drama, and there is no immediate way to call them out on the spot.

That means I read and digest thoughtful content from folks who are technically competitors…well, on paper anyway. In reality, we are all pros and generally outspoken critics of a broken financial services industry serving their master – sales. So rather than view each other through the close-in camera lens of competition, we choose the wide-angle lens viewing each other as colleagues acting in concert as fiduciaries on behalf of investors’ best interests.

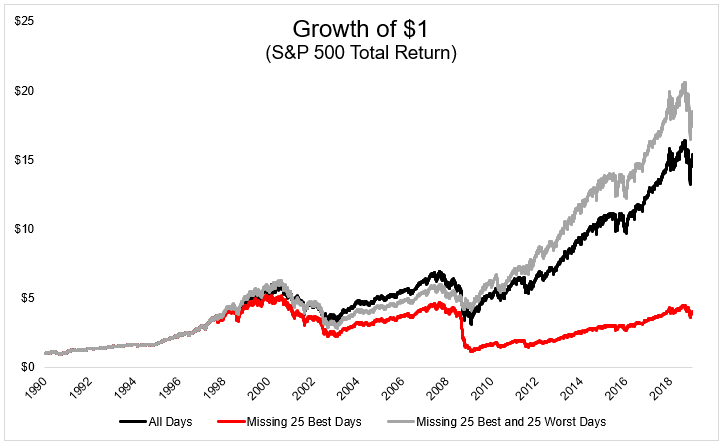

On that note, a great piece just came out from Michael Batnick, CFA over at Ritholtz Wealth Management. It’s titled, “Miss the Worst Days, Miss the Best Days.” He has a larger lesson that I’m going to gloss over and instead cherry pick a smaller point he makes about not being in the market when it is experiencing advances:

If you missed just the 25 strongest days in the stock market since 1990, you might as well have been in five-year treasury notes. This remarkable data point is almost always followed by “time in the market beats timing the market.” I’m generally on board with this line of thinking, however, I don’t necessarily agree that this chart is the best way to prove this point.

He then goes on to say:

The chart below shows what happens if you were able to successfully avoid the 25 best and 25 worst days. This would have put you well ahead of the index. Of course, this assumes perfect end of day execution, no transaction costs, and most importantly, no taxes.

Here’s the chart.

He concludes with:

I haven’t yet mentioned the most important assumption, which is that you could stick with this for twenty years…would you have been able to stick with it when it is dramatically underperforming the index?

He’s got a point. You should go read his blog; He’s smart and I hope over time we stack the house at Monument with people of his caliber…but I have a different point.

What if the “All Days” line was good enough to get your wealth to a level necessary to fund all your goals and objectives? What if you didn’t waste your time trying to perfectly time the market and account for taxes and costs but rather just had a long-term strategy to make sure you were not out of the market on the 25 best days?

It’s easy. Frequent readers are already anticipating my drum beat of the real silver bullet: patience and discipline.

I personally know people who completely abandoned a reasonable, well thought out investment strategy last quarter simply because they were not making money over a short snapshot in time. I’ll bet that their knee jerk reaction was to sell and go to cash because “they just had to stop the bleeding” or some other common response to losing patience and discipline.

In other words, they were riding the red line above.

It’s easy to be the “All Days” line and not the “Missing 25 Best Days” line. It’s called having a plan that projects out any need for cash over the next 18 or so months and leaving your investments alone.

With a plan like that in place, you have no need to sell on Christmas Eve and you are happy that you’ve seen a lot of that sell-off rebound back.

In other words, you are “All Days.”

Keep looking forward.

Dave

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.