Trade and The Tariff Man

I was inspired to write based on a social media post from yesterday by my old friend and stalwart colleague, Rob Bartenstein, the CEO of Kestra Wealth Management.

“The news media may or may not be the enemy of the people. But it ain’t your friend. Your friend wouldn’t blare negative sh!t [my edit] at you all day punctuated with ads for pain relief. Your FRIEND would tell you how much you are loved and appreciated and where the free ice cream is.”

Who doesn’t like free ice cream?

One of the things that I enjoy about the usefulness of Twitter is the blend of commentary with no real advertisement influence. Right, Twitter makes money selling sponsored ads, but the people who tweet are not trying to drive eyeballs to Twitter’s sponsored ads…they are trying to drive eyeballs to their own tweets. The currency exchanged on Twitter is respect and “follows,” so there is a huge incentive to post well thought out, fact-based, defensible positions.

Idiots and charlatans on Twitter don’t get respect and don’t get followed. In fact, they get called out…sometimes viciously.

Conversely, CNBC and other traditional media sources rely on capturing eyeballs to drive advertising rates through sensationalism, hype and drama, and there is no immediate way to call them out on the spot.

That brings me to the current market situation…I’m seeing complete hysteria.

I wrote about the yield curve inverting and how long it takes a recession to materialize after inversion in “When the Yield Curve Inverts.” My opinion is that the near-inversion is based on a problem with the short-term rates not the long-term rates. The long-term rates are a function of the market’s expectation for long-term growth and inflation expectations, the latter of which has been pushed down with the sudden and rapid decline in oil prices. The short-term rates are controlled by the Fed. So when Fed plans for interest rates exceed the market’s expectations for growth and inflation, that’s a Fed problem (Chairman Powell problem) and it increases the probability that we see a pause in the Fed’s current and expected plans for rising rates…possibly even in the December meeting.

I also think that trading on the possibility of an inversion is just stupid for anyone who calls themselves an investor.

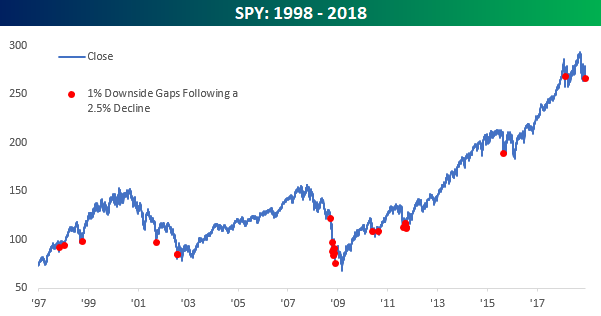

So, I’ll just move on. Just remember, things like Tuesday and today happen. The chart below is from Bespoke.

The real hysteria comes from the media insincerely depicting the recent trade news, claiming that there isn’t an actual agreement in place. But there is…in fact, China and the U.S. have both officially stated it.

Of course, there are some “differences” between what each country is saying is in the agreement, but I think this is more of a “there are three sides to every story” kind of situation. There is Trump’s side, Xi’s side and the truth…with the truth somewhere in the middle, I’m guessing.

The media is hyping the appointment of Robert Lighthizer as the U.S.’s negotiator as if it’s a bad thing. Today, Politico wrote, “Trump names hard-liner Lighthizer to be ‘vigilant’ in China talks.”

That doesn’t sound good, does it?

However, after reading through the posts of some smart people on Twitter, I learned that Lighthizer is a U.S. Trade Representative, unanimously approved by the Senate Finance Committee and confirmed 82-14 by the Senate. Oh, and he’s a Georgetown Law School grad.

I concluded that he’s probably a pretty tough negotiator…and that’s what we need at the table.

The Trump tweet is providing plenty of fodder for those predisposed to confirmation biases and I think the media and late-night TV took it out of context to capture the eyeballs.

That’s just what I think.

Look, I get it…if I were President, I would never act, speak or tweet like he does. I’m not defending HIM, I’m just pointing out that the opinions woven into the media may be hyping this for the benefit of their own business model.

Here’s something else I think…I think a deal gets done. The problem will be that market volatility will continue to be driven by the media business model of generating sensationalism, hype and drama combined with the understandable dance and face-saving of the negotiation process for both parties.

The media lives on bad news. Over the next few months, the media will probably make you doubt a deal will be reached.

Good.

We need ambiguity on this issue because the U.S. will not have any negotiating power unless everyone believes Tariff Man is dumb enough to inflict the pain of a trade war upon the American economy. You should cheer every time you hear someone of any authority (and any dubious authority) complaining that the President is out of his mind for thrusting us towards the economic cliff of a trade war because it only strengthens the position of Lighthizer’s seat at the table.

This means uncertainty and volatility in the market will most likely be prevalent over the next few months. Steel yourself for that.

A deal will be made – that’s what I think. Don’t fall for the media hype to sell ads.

If I’m wrong, that will speed up a recession, but for now our model is still at MONCON 5, the lowest level of recession probability. If that changes, we will be out with a specific piece on that change.

Instead, grab a friend and treat him or her to some free ice cream.

Keep looking forward,

Dave

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.