Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

What’s going on with MONCON – A look inside our recession probability model

I’ve been staying away from the heavy “blah, blah, blah,” technical writing in an effort to keep everyone focused on what I think the proper mindset should be during this crisis. However, I need to publish an update on what’s been up with our MONCON recession probability model.

People want to know, “WTF MONCON!?”

Even though MONCON failed to predict this recession based on how swiftly the conditions changed on the downside, I still believe it is an effective tool for risk management. In particular, when to remove risk and when to add risk to your investment portfolio. I also want to remind everyone what an effective tool it was in helping us navigate the numerous head fakes over the past five years. Staying invested over periods like the bear market in January 2016, the selloff in January 2018, and the recession fears in December 2018 are easily forgotten success stories of our MONCON Recession Plan.

The most important thing to remember about the MONCON recession probability model is the age of the data. The data that gets loaded into the model lags by about ten days. In normal times, that is not a problem since the increasing probability of a recession is usually something that builds over time.

However, given the swift and sudden nature of this crisis, ten days turned into an eternity.

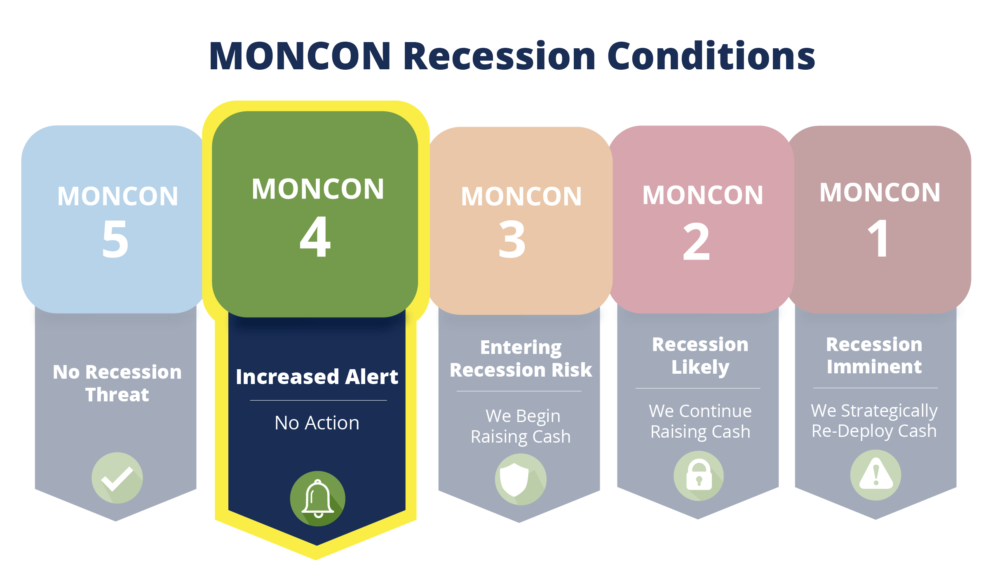

Data that was loaded into the model from March 20th gave us a new MONCON reading on Tuesday, March 31st. At that time, MONCON moved from MONCON 5 to MONCON 4.

Even before the move from 5 to 4, we had started liquidating securities across our managed portfolio independent of MONCON as specific securities triggered sell alerts. In normal times, when a security triggers a sell alert, we use the proceeds from the sale to repurchase a new security.

Because of the rapid sell-off and the lack of visibility into the economic impact of this event and its probable negative impact on future corporate earnings, we kept the proceeds in cash out of an abundance of caution and to act as a cost-free hedge against a continued sell-off.

As you can see above and read more about in our original “how to manage a recession” blog post, a move from MONCON 5 to 4 does not set the conditions for Monument to raise cash in managed portfolios. Under normal times, there is a 50/50 chance that a move to 4 results in a move back to 5.

It is not until MONCON moves from a 4 to 3 that our risk management rules direct us to proactively raise cash across our managed portfolios. Again, in normal times.

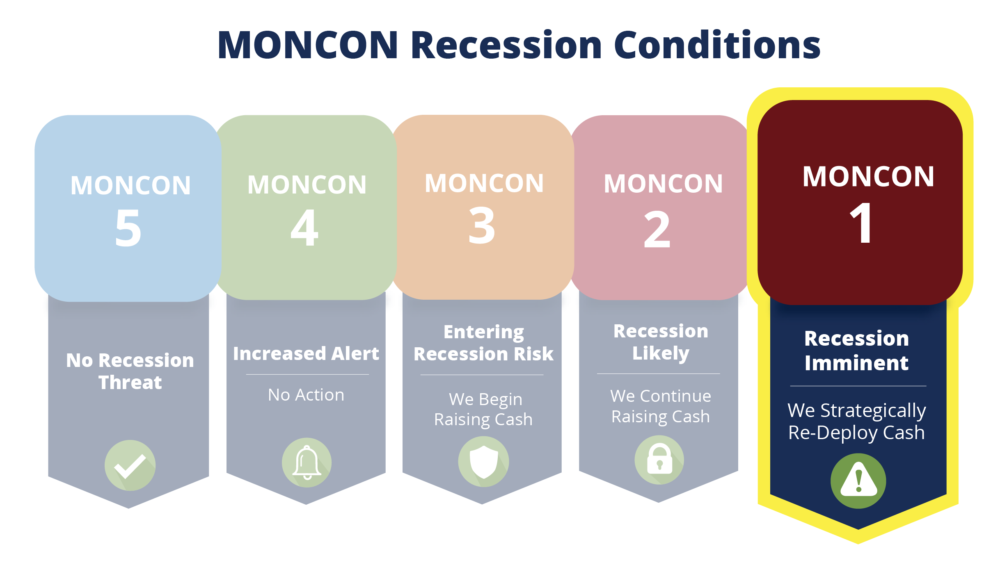

The latest data loaded into the current MONCON reading is from the 27th of March. That data caused the reading to surge from MONCON 4 directly to 1.

Obviously, that is a massive and rapid move for the model, and it is simply not designed to forecast recessions that are caused by sudden events, crises, or pandemics.

In fact, nothing is.

That does not make MONCON useless, but it does beg the question, “What does it mean now?”

The economic indicators that feed into the model are not going to recover in lockstep over 7 days in the same way they crashed. In fact, I think they will recover slowly and normally, making it an effective tool to help us determine an opportunity to put money in our managed portfolio’s back to work for long-term growth.

As such, we have begun to slowly redeploy cash reserves that were raised in February across our managed accounts. As I said in my last video (and I have written about in most of my recent blogs), it is impossible to know when we have hit A BOTTOM or even THE MARKET BOTTOM. However, I am optimistic that we will continue to make progress on fighting the virus and the U.S. economy will get back on its feet very quickly.

When we look back at the history books, I think everyone will agree that April will be viewed as a good opportunity to invest in the future you.

It’s possible we could go down from here proving that this may not be THE BEST opportunity that presents itself.

It’s also possible that March 23rd will prove to have been THE BEST opportunity when the Dow was at 19,992.

When I’ve decided I want to own something and suddenly see it on sale at 20% off, my natural inclination is not to say, “I’m gonna wait for it to be 30% off.”

My inclination is to say, “I was willing to buy XYZ at its normal price and now that it’s 20% off, that’s a good deal so I’m going to buy it now.”

Everyone’s mindset should be, “I want to be investing in the future me” and not “Where is this market going over the next 2-3 months?”

And down 20% is a better long-term opportunity than down 15%, 10%, or 5%.

Our Portfolio Update email will be out to clients shortly and will highlight the securities we sold, why, and how we chose to redeploy SOME of the cash we raised in that process. Our Portfolio Manager and Private Wealth Advisor, Erin Hay, CFA will also be highlighting the reasons why we continue to hold some securities.

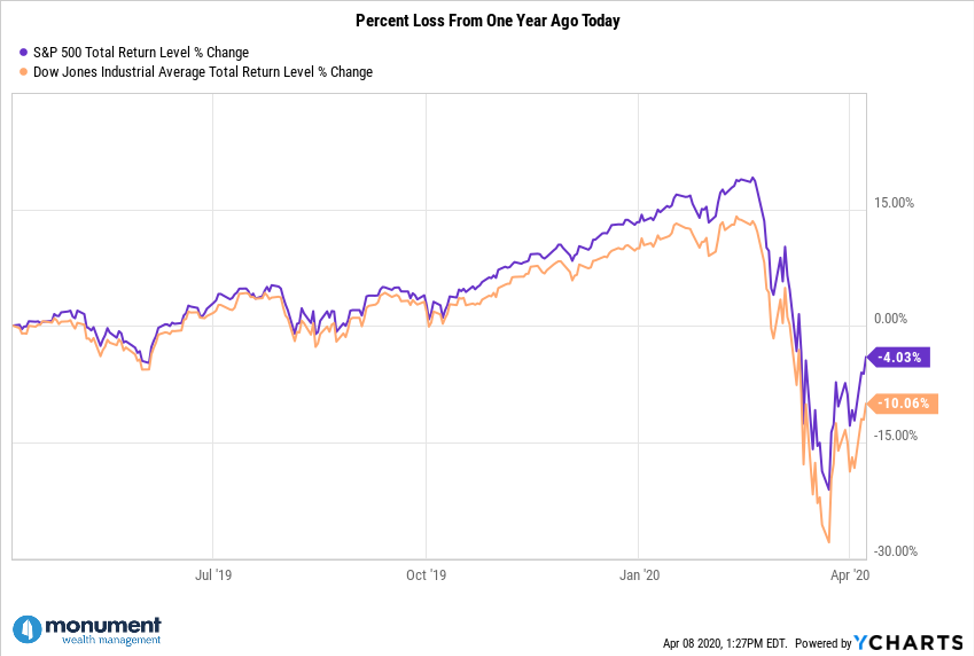

This market seems to be trading daily on nothing more than good news outweighing bad news and vice-versa. Keep the below chart in mind – I think it helps to see the previous 12 months of returns rather than focus on the past six weeks of returns.

It should help you too…

Keep looking forward,

Dave

What’s Next?

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.