Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

What the UK Debt Crisis Teaches Us About Managing Debt Costs

England is having a tough time adjusting to higher rates – just Google “UK debt crisis 2022”. It’s admittedly a strong statement, but Google works on headlines, and I find that headlines tend to use phrases like that frequently.

Bloomberg, CNN, NY Times, etc., are all writing and/or talking about it, so I won’t spend much time discussing the gritty details, but I would recommend looking into it. It’s interesting stuff – for investment dorks and non-dorks alike.

Here’s a Quick Summary on the UK Debt Crisis: A Gilt-y Moment

- The UK government announced broad tax cuts. This means the government will likely need to borrow more to maintain their current spending levels, especially since they are subsidizing higher energy costs to help soften people’s pain this winter.

- The interest rate on 10-year Gilts (UK government bonds) spiked on the announcement. Anticipated increases in future debt levels for the UK government, lead investors to demand higher interest rates to lend money to an already indebted country.

- In 8 days (9/19/2022 to 9/27/2022), 10-year Gilts went from 3.16% to 4.47%. That’s a +41% jump… in 8 days… THAT’S FAST!

- The increased borrowing costs over such a brief period, led to liquidity concerns across the economy and financial markets reacted negatively.

- The UK government backtracked on their proposal, the prime minister resigned on 10/20/22 after just 44 days in office, and the markets seemed to have calmed down.

Coincidence? Impossible to know, but I think it’s safe to assume the financial markets’ temper tantrum had some impact on the political decisions.

I’m hopeful for a positive resolution, but it’s important to note that the UK economy almost had real debt problems in about a week. All thanks to the spike in borrowing costs that resulted from proposed fiscal policy changes.

It’s been a recurring theme of mine this year, but all markets seem to be moving insanely quick.

What can investors do when markets are whipping around like this?

Answer: Clean up your “Financial House.” In other words, be prepared.

Dave Armstrong recently wrote about how financial market commentary should be categorized into one of three buckets: 1. Interesting, 2. Actionable or 3. Both.

That said, I’d label the UK story as “Interesting” only. No portfolio actions to take, but it is a good reminder about managing your debt costs, especially in a rising interest rate environment. Rates seem unlikely to go back to zero anytime soon. That statement isn’t “Interesting,” everyone seems to know that. But the transition to higher interest rates does present some “Actionable” items.

People, investors, business owners, and executives need to be prepared for fast moves in financial markets and ensure their “Financial House” is in order. They need to be financially unbreakable, so if a high-speed move occurs, they are ready.

A few good first steps to kick off the “house cleaning”:

- Check your cash levels and income flow. If your cash reserves are feeling uncomfortable, consider replenishing them.

- Review your investments’ long-term goals/priorities and update them if necessary. If they have changed, you should review your asset allocation to make sure it’s still appropriate for you.

- Check your debt levels and the cost of carrying that debt now that interest rates are higher. And if you don’t have a final payoff plan for your debt, work to create one.

How Consumers are Navigating Record Debt Levels

Let’s focus on the final bullet point regarding debt. According to the New York Fed’s website, as of 6/30/2022:

- Total household debt rose +2% in the second quarter, the largest increase since 2016.

- Total debt is now $16.15 trillion with mortgage balances totaling $11.39 trillion of that.

- Credit card balances were up +13% year-over-year, the largest increase in more than 20 years.

I’ve started to hear some analysts talk about the overall levels of consumer debt. Yes, there is a lot of nominal debt out there, but that isn’t necessarily a terrible thing – even as the Fed remains committed to hiking rates and pushing lending costs up.

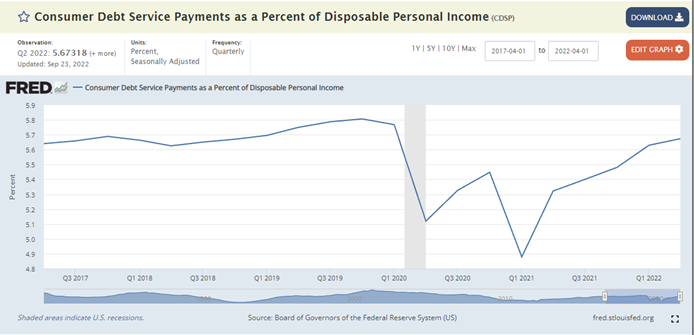

If you can service that debt within longer-term payoff plans, borrowing funds can be a useful part of your wealth plan. However, you must be able to manage it. Look at this 5-year chart from the St. Louis Fed’s website as of Q2 2022. This shows the percent of consumer disposable income (income after tax) that is being used to pay their debts.

While overall debt may have grown rapidly last quarter, the overall servicing of that debt as a percent of after-tax income is about even with pre-pandemic levels when interest rates were near zero. Thankfully, it appears consumers have been doing a good job so far of managing their income/cash flow and paying their debts despite interest rates more than doubling since mid-March.

Having a Plan is the Best Way to Prepare

While the UK’s situation might not present anything “Actionable” from an asset allocation standpoint, it does provide a good reminder to review your debt.

Keep an extra close eye on your variable debt (think of credit cards, lines of credit, margin accounts, etc.) which can have a bigger effect on cash flows. If interest rates continue to increase, variable debt becomes more expensive as the borrowing costs go up too. Debt that was previously manageable can suddenly become unsustainable.

Most importantly make sure you have a plan to payoff that debt. Eventually the bill does come due, and you should be ready for that time. If you don’t have a plan, make one, or contact your wealth advisor to discuss ways to not only effectively service, but ultimately payoff your debt.

Debt is a key piece of your wealth plan and managing it has become even more important in a world of higher interest rates. And it’s vital to be prepared when markets are moving this fast, so you don’t get caught flat-footed like the UK almost did.

Nate W. Tonsager, CIPM

Private Wealth Advisor

What comes to mind when you think of Wisconsin? Farmland? Cheese? Growing up in a small Wisconsin town, Nate can confirm that the cheese is as good as they say it is, but what shaped him most was being a part of a strong, close-knit community with a desire to help your neighbors. Nate got his first taste of the financial industry during high school...

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.