Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Investors: What Should You Do with Your Bond ETFs?

I received a great follow-up question to my piece last week about not stressing over paper losses on your individual bond positions: What about investors who have bond ETFs? How should they approach their paper losses?

I felt the answer deserved to be shared because many people use ETFs for their bond exposure. In short, my advice of “stick to the plan” still holds for bond ETF owners, but with a caveat. It depends on why you want to own them. Is it for income generation or for portfolio diversification?

Income Generation

If you’ve been using bond ETFs to produce income, now is a good time to consider moving to a bond ladder comprised of individual bonds. Yields have risen and we are now seeing opportunities to lock in a 5%-6% annual rate using individual corporate and/or municipal bonds with a 5 to 6-year average portfolio duration.

Bond ETFs of all issuer types (government, municipal, corporate, etc.) have shown material price volatility over the past couple of years, so moving into a hold-to-maturity, individual bond ladder will lock in yields and would also help reduce the impact from price swings caused by interest rate movements. This is just like what I discussed in last week’s article.

Portfolio Diversification

If you’ve been holding bond ETFs as a portfolio diversifier, I would recommend staying the course for now just like the owners of individual bonds. Bond ETFs and individual bonds behave similarly, and right now both may be underwater from a price standpoint, but they are paying investors elevated yields.

The key difference between them is that bond ETFs rarely have a singular, set maturity date meaning there are no repayment guarantees ETF investors have by holding-to-maturity. With less guarantees, bond ETFs should have higher volatility than individual bonds, but also the potential for higher total returns over time.

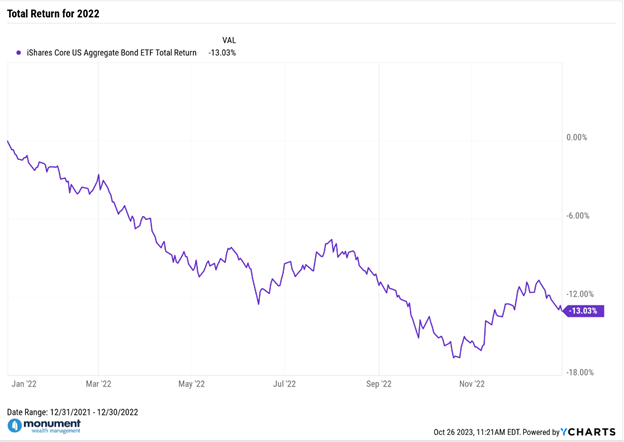

Price Volatility In the U.S. Bond Market

To illustrate what’s been going on with bond ETFs, let’s look at one of the biggest, the iShares Core U.S. Aggregate Bond ETF, ticker: $AGG. It now has a 30-day SEC yield around 4.84% annualized, which is pretty competitive given the current rate backdrop. However, that increase in yield also caused a -13.03% total return in calendar year 2022.

But if you look back a little farther into recent history, $AGG has also seen some stretches of impressive performance like 2019 through 2020, which saw a cumulative total return of +16.57%, or +7.95% annualized, over those two years.

These are fitting examples of the volatility, both positive and negative, bond ETF owners have experienced recently and should expect in rapidly changing interest rate environments.

So far in 2023, $AGG is down about -3%, but in the future, if interest rates move significantly lower during a flight to safety caused by the next crisis, whatever that may be, we likely will see noticeable price appreciation in bond ETFs like $AGG.

Why You Own Them Dictates Your Response

To summarize, with individual bonds you’re waiting for their set maturity date and the principal repayment. With bond ETFs you’re hoping for lower rates leading to their price recovery. However, no one can predict the next move in rates. It could be up or down, so with bond ETFs it’s impossible to know how long you’ll be waiting for or your final payout.

That’s the crux of this discussion. If your financial plan, time horizon and risk tolerance can support some volatility, bond ETFs continue to be appropriate for your fixed income exposure. If not, ladders of individual bonds are starting to appear well suited for investors who want to reduce some fixed income risk while locking in a known income stream.

Every investor is different, so there is no “right” answer to this question. But whether you own individual bonds or bond ETFs, they should be part of a long-term financial plan and should be offering some form of diversification or safety within your portfolio.

Nate W. Tonsager, CIPM

Private Wealth Advisor

What comes to mind when you think of Wisconsin? Farmland? Cheese? Growing up in a small Wisconsin town, Nate can confirm that the cheese is as good as they say it is, but what shaped him most was being a part of a strong, close-knit community with a desire to help your neighbors. Nate got his first taste of the financial industry during high school...

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.