Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Investing before the market bottoms – How bad is the pain?

At the risk of sounding repetitive, I want to reinforce my point of differentiating between market bottoms and opportunities.

I’m on the Investment Committee for three different foundations, The Marine Corps Heritage Foundation, the Community Foundations for Northern Virginia and The Station Foundation. All three foundations are reviewing their first quarter portfolios, holdings, and performance. One of the common discussions is, “Should we be putting cash to work right now or is there still more downside?”

So, like many, I’m living the emotional rollercoaster of wondering about a market bottom or the market bottom. On one call I paraphrased a Warren Buffett quote, “I like to eat hamburgers, so when I see them on sale, I buy them and eat them.”

Well, the quote is something to that effect…but you get the point.

Foundations are different than individual investors in one regard – they are essentially indefinite life organizations. Other than planning out their annual cash needs from the portfolio, they don’t have any future event like retirement to plan for.

They have an infinite time horizon!

Yet even with a time horizon of infinity, these committees still have PEOPLE on Boards and Committees…all subject to their own formative experiences, behavioral biases, emotions and human tendencies.

So, after one call, I decided to do a little history project and combine it with some arithmetic. That should scare any reader I went to high school with, especially if they were one of my teachers.

My good friends at YCharts (@ycharts) helped me by exporting data on the S&P 500 going back to the 1950s (that’s as far back as they had data, but it’s good enough). Disclosure – I’m a paying customer, I get nothing from them by highlighting their data and product here – I just really like the service and especially the support I get.

I wanted to see what returns looked like assuming an investor dumped money into the S&P 500 index at some point after it started to sell off from an all-time high (ATH), and that sell-off resulted in what is historically considered a Bear Market.

I had to make some assumptions as to “when” that investment would happen and since I’m reading a lot about how Bear Markets “bounce” then sell off again, I just picked the date three months prior to when market bottomed out and started a recovery.

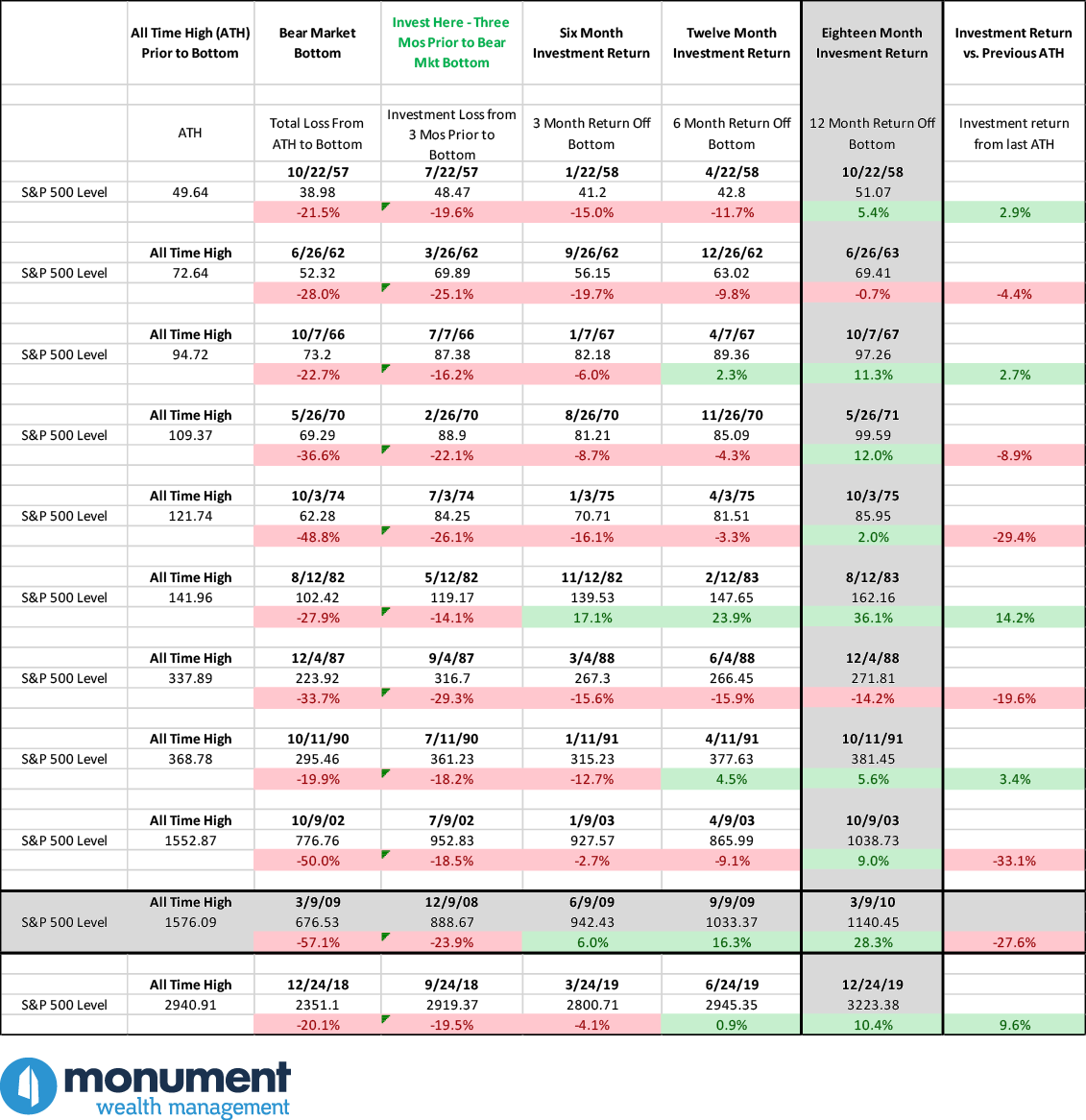

Across the top, you’ll see descriptive boxes.

Follow along the 2008/2009/2010 date range as an example – it’s a row in gray.

The first two columns from left to right show that the S&P 500 index hit an ATH level of 1,576.09. From there, it sold off to a market bottom index level of 676.53 on March 9, 2009. This was a peak-to-trough loss of -57.1%.

The next column shows the S&P 500 index level of 888.67 on December 9, 2008, which is three months prior to the bottom. Its -23.9% return is how much the index was down on that day from the ATH of 1,576.09.

The next few columns show the S&P 500 index levels and returns six, twelve and eighteen months from the December 9, 2008 “imaginary investing date” (which is also three, six and twelve months after the BOTTOM.) In this example, the returns from December 9, 2008 are +6%, +16.3% and +28.3% respectively.

Finally, there is a column that shows what the return would be eighteen months after December 9, 2008, relative to the last ATH. In this example, eighteen months later, the S&P 500 was still -27.6% BELOW the ATH.

Here’s the point – there’s a good chance that even if an investor invests too early and has a negative return down to the bottom, they will regain the losses and even be positive in relatively short order.

As you can see, in all but two periods, any investment in the S&P 500 three months prior to the ultimate market bottom is green (positive) in 18 months. In some cases, it’s SIGNIFICANTLY positive. The only exceptions are 1963 when the “early investment” was still negative -0.7% and in 1987 when the “early investment” was still down -14.2%.

The 18-month returns made three full months before an eventual bottom in order from highest to lowest are:

+36.1%, +28.3%, +12.0%, +11.3%, +10.4%, +9.0%, +5.6%, +5.4%, +2.0%, -0.7% and -14.2%.

You may not catch THE market bottom, but in most cases, being early is not going to do a lot of damage to an investor who seizes the opportunity.

In other words, if you like hamburgers and they are currently on sale at 20% off, you should buy some – because right now they are a good deal.

And let’s face it, you were probably okay buying them in November, December and January at full price anyway…when they were 0% off.

Keep looking forward,

Dave

(Also see our disclosures, I have to say that because I’m human and I could have made a mistake. I checked my formulas carefully, but still…)

What’s Next?

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.