Explore Our

“Off The Wall” Blog

Read our Private Wealth Advisory team’s unique thoughts on the markets and investing.

Erin’s Emerging Market Musings

“Truth is an up and to-the-right line. Not a university lecture or a cheering crowd.” – Alex Good

Something we routinely call out in our monthly FAA update pieces is what we are doing with respect to Emerging Market (EM) stocks. An important topic, considering EM is home to nearly 85% of the world’s population and close to half the world’s share of global trade, despite accounting for less than 15% of global market capitalization.

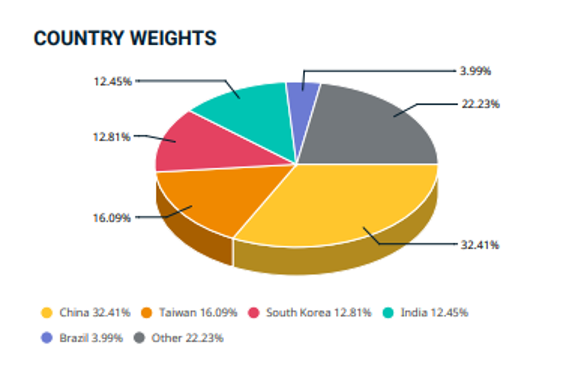

For reference, here’s what we mean when we say “EM.”

Source: MSCI

My opinions on the conventional merits of EM investing have changed a lot over the last ten years. I used to believe that nearly everyone should own some EM stocks. For their implied diversification benefits, and because EM demographics and structural trends would underwrite superior long-term outperformance versus the U.S. Intuitively, it just made too much sense. “What?! You don’t have any EM exposure? You’re obviously not CFA material.”

The thought was: EM would start to work. It had to. Eventually. Much like Value would start to outperform Growth. And interest rates would begin to rise. And the Texas Longhorns would be “back.”

Then reality set in. And not just in Austin.

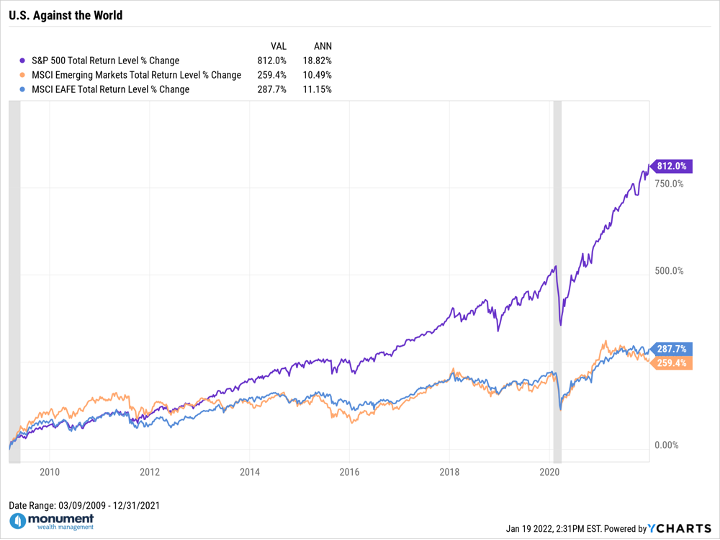

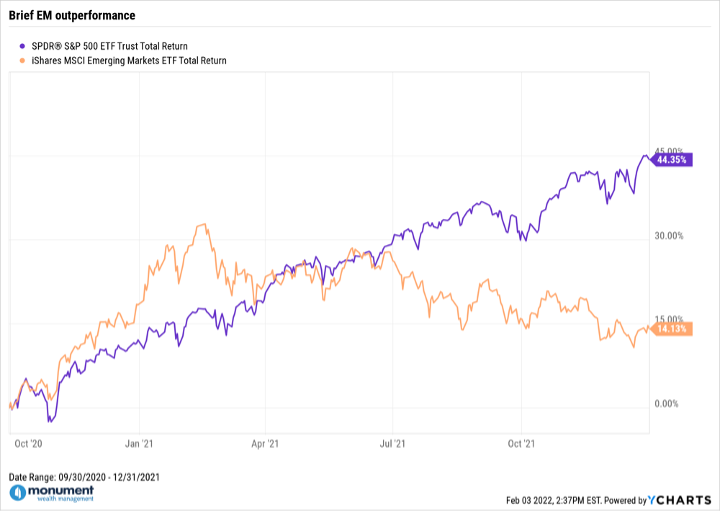

The graphic above shows the cumulative and annualized performance of the S&P 500, Developed International and Emerging Market stocks since low tide of the Great Financial Crisis in March 2009 (which ironically coincides with the last year Texas last won a conference championship). EM, for all its supposed structural tailwinds, has been a massive disappointment. At least, for buy-and-hold investors with “naive” exposure. Twelve years is a long time to suffer if you’ve had any meaningful allocation to non-U.S. stocks, and doubly true if those stocks are EM in nature. I guess triply true if you’re a Longhorn season ticket holder. And there is no reason that these disappointments can’t continue. Trends can last longer than people realize.

They say there is nothing like price to change sentiment. And I am not immune…my sentiment has drastically evolved. So given the previous chart, here are what I perceive as the main reasons to avoid naïve exposure to Emerging Market stocks. Or at least things to consider if you have an existing allocation or are thinking about allocating to the space.

- Despite being touted as a diversifier for U.S.-centric portfolios, there is ample evidence showing that the desirable correlation characteristics of EM are only present during bull markets. In plain English: EM doesn’t offer diversification benefits during bear markets.

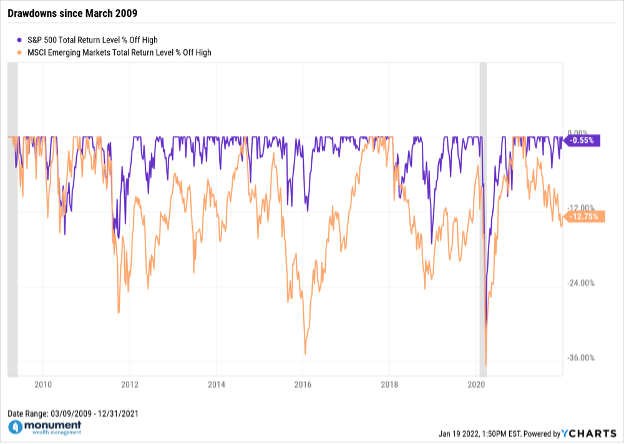

- Not only has EM arguably not provided expected diversification benefits, but it has also subjected investors to more extreme drawdowns than U.S. markets. Look below: the further the line is from 0%, the greater the fall from a previous index high. EM is consistently in drawdowns ranging from 20-30%.

- Emerging markets do not conform to U.S. accounting standards (U.S. GAAP) and are often littered with firms that have a high degree of state ownership. On the accounting bit: that makes knowing what you own that much trickier. Of course, you could outsource the minutiae to a third-party manager, but that is going to cost you, as active EM funds have notoriously high expense ratios. And when it comes to state-owned enterprises (“SOE’s”), it is not hard to imagine how a group like the Chinese Communist Party doesn’t have the best interest of U.S. shareholders or global stakeholders in mind. Talk about an Environmental, Social, and Governance (ESG) nightmare.

- Lastly, one can make the case that investors looking for “exposure” to EM demographics don’t need to look outside the S&P 500. According to FactSet, nearly 40% of aggregate S&P 500 revenue is derived from international sources.

When should you have emerging market stocks?

I’ve just given you a laundry list of reasons to avoid. So, the natural question is, when should you have EM stocks?

Simple.

When they are going up.

You laugh, but I’m being serious. Don’t be a midwit.

Okay, in practice it’s a little more involved than that. What variables do you assess? What time frames are we talking about? And what about the underlying investment vehicles? But conceptually speaking, it’s quite simple. Momentum and relative strength –concepts underpinning our Flexible Asset Allocation (FAA) and Tactical ETF (TacETF) models – are incredibly value in assessing not only when to invest, but also when to avoid.

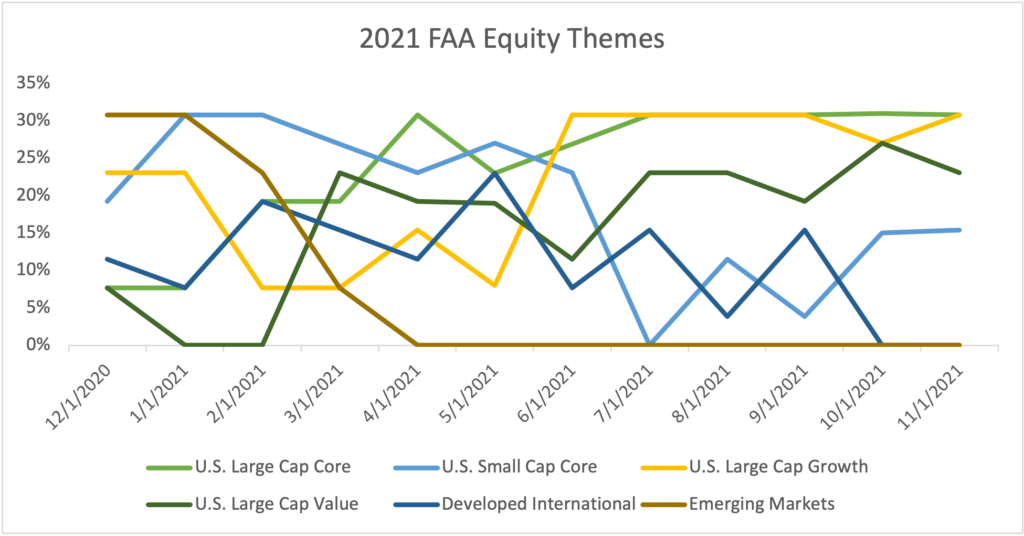

The graphic below shows the relative weightings of EM in our FAA and TacETF models throughout the last year. Notice the brown line. Despite EM posting negative returns in 2021, our FAA model experienced some upside from EM during the year.

That’s because we participated in a somewhat pervasive (albeit short-lived) trend. EM outperformed the U.S. by a wide margin beginning in the fourth quarter of 2020, though you can see that trend eventually dissolved and reversed course. As did we with our EM allocation in the FAA model. What was once our highest stock weighting in the model soon turned into a complete “zero” allocation. Again, see the brown line above.

There’s a lot more to unpack here, so we will cut it short with a simple call to action. If you are working with another investment provider…and this is especially true of anyone reading who might be involved with an institution who has a mandated weighting to Emerging Market stocks via an investment policy statement…ask them how they think about EM, and how that impacts how they invest. Do they give a lazy, boilerplate answer? That is, having a naïve “evergreen” allocation for the supposed diversification benefits? Or do they have a more thoughtful, nuanced approach?

In fact, here’s one more call to action – check out the “Are We a Fit” page on our website to see the types of people we help. If it sounds like you, reach out to us and we can talk through how our Flexible Asset Allocation strategy works.

Curious what others are saying? Check out our Google Reviews.

Until next time.

Erin

Erin M. Hay, CFA®, CMT®

Private Wealth Advisor, Portfolio Manager

A graduate of the University of Oklahoma, Erin began his investment management career with J.P. Morgan Private Bank. There, he worked with portfolio managers, traders and asset class specialists to bring tailored investment solutions to his team’s high net worth clients. However, intellectual curiosity would dictate both a change in geography and job description.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.