Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Eight Week Winning Streak Over – Time to Sell?

The Dow and the S&P 500 both broke eight-week winning streaks. It has been an impressive run-up in prices, but not without precedent. Everyone remember 2013?

Well in case not, we had a nice strong bull market in 2013.

No two periods are exactly alike, I get that, but comparing key metrics and some of today’s concerns with 2013 offers a perspective – things really weren’t that different back then.

However, I’ve been getting different versions of the same question for a few weeks now, “Does anything about the current environment give me pause?”

It’s a little bit of a loaded question since investing always carries risk and anyone that claims to know what’s happening next is either a charlatan or a fool.

Market corrections are really about probabilities in my mind. In other words, what is the probability that we will have some sort of correction caused by an economic event like a recession?

My answer is that I just don’t see a high probability of a recession or an economic event on the horizon over the next 12-18 months. I realize that with the markets at all-time highs and also looking expensive, it may FEEL LIKE the market is about to correct.

And it might. But it might not. And if it does, I don’t think it will be because of a recession or economic event…it will more likely be a behavioral reaction. If that happens, there will be a bunch of “I told you so-ers”, but they are just guessing. Don’t let anyone break their arm patting themselves on the back if they win the “best guesser” award.

The bottom line here is that we don’t see anything out there on the horizon that changes our current investment view…it just seems clear to us that the wind is still in our sails as the global banks are pumping more capital into the system than is needed by the economy and that is supporting markets globally.

It’s not that a selloff can’t occur. We’ve experienced four corrections of at least 10% in the S&P 500 Index since the bull market began in 2009. But investors remain optimistic that a profit-punishing recession isn’t likely in the near term.

Reasons? Most leading economic indicators are positive. Growth is accelerating. Inflation is not. Interest rates are still really low. The yield curve is positive, and I suspect we will see it steepen. At some point I think we will see the dollar strengthen as passage of tax reform gets closer.

I think people and businesses like sureness and when the tax reform is passed it will unleash spending that has been held up…since no one was really sure whether a bill would be passed and what it would include. (I know we still don’t know what will ultimately be included but we kind of know what it will look like.)

I don’t think the bull market is over. I’m not saying it will last another 8 years, but I don’t think we are heading into a recession over the next 12-18 months.

Probabilities are better than guesses. Guesses are made with your gut and caveman brain.

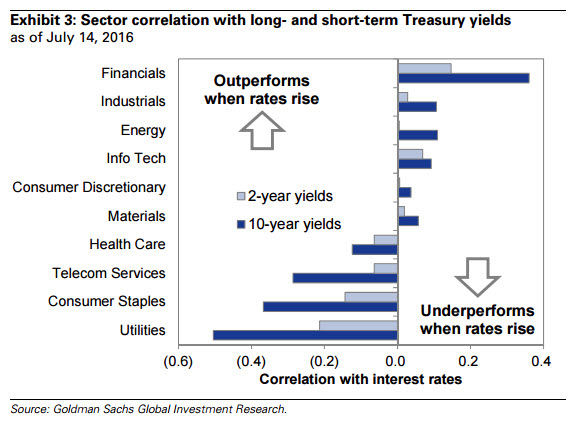

We continue to like the financial, tech and industrial sectors alongside a higher-than-usual exposure to developed and developing overseas markets. We like equal weighted exposure to indices versus market cap weighted indices to limit the exposure to the very expensive FANG stocks.

Here’s a Goldman Sachs chart from 2016. I, along with most others, believe that rates will rise.

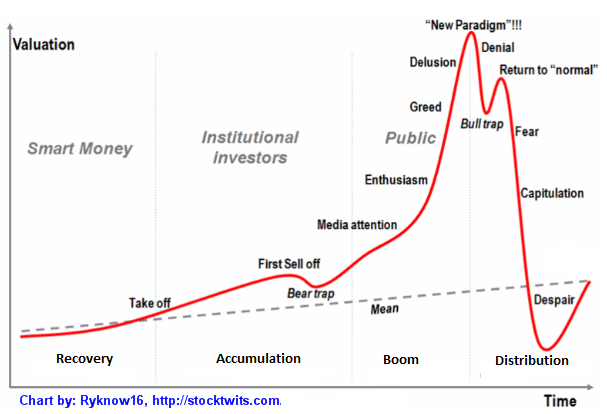

I remember the late ’90s very well and the calls for the market at a top in ’96, ’97 and ’98. Those calling for a top never dreamt of a year like 1999. I was brand new in the business and 1999 will always be my benchmark for measuring complete mania…we are nowhere near those levels. Take a look at the chart below. I think we are in the “Boom” cycle, but not near the “New Paradigm” peak.

Please call with questions.

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.