Decoding Market Signals: RRG® Charts, Stock-to-Bond Strength, and More

I grew up in Wichita, KS and Tulsa, OK. Smack dab in the middle of Tornado Alley. When I was a kid, every Friday at noon, both cities would run tests on their tornado alarms. Which were just repurposed Cold War nuclear bomb sirens.

If you were from out of town, it was a little disconcerting. But if you were a local and it was sunny or December, you went about your day. Although the fact it was winter was not a guarantee that tornadic activity wouldn’t materialize. Strangely enough, in all my time in Kansas, Oklahoma, and now Texas, I have NEVER seen a tornado. This is akin to someone who grew up in Colorado having never experienced snow. Go figure.

So, welcome to Monument City. This is kinda-sorta our Friday early warning system testing. As a reader, you know not to panic, but to simply acknowledge that we’re monitoring trends in the capital market weather system. But instead of Advanced Doppler and air raid sirens, we’re using Relative Rotation Graphs (RRGs) and a Friday blog as part of our radar array.

For the uninitiated, please read our RRG primer post here. In short, these visuals can give us a bird’s eye view of relative strength in and among the capital markets, highlighting points of strength and weakness.

Let’s first do a mid-month check on stock-to-bond relative strength, a variation of which is a large component of our Flexible Asset Allocation (FAA) model. On a weekly scale, stocks have turned over in comparison to the aggregate bond market, as measured by the $AGG ETF. Not a perfect “comp” for our FAA model, but directionally it works for us.

On a smaller timeframe (daily), the relationship has actually started to improve and is heading further into the leading quadrant. Given the disproportionate share of U.S. equities in the construction of the $ACWI ETF, 3Q23 earnings season – in conjunction with ongoing geopolitical events in the Middle East –are going to go a long way in determining the near-term direction of this chart. Remember, this isn’t a rendering of absolute performance, just a relative performance comparison. The $ACWI line may turn up due to strength in stocks and/or weakness in bonds.

Next, let’s revisit the eleven S&P 500 sectors, which are most relevant for our Core ETF model, where we run a relative strength sector rotation sleeve. In short, there isn’t a ton to love here now, with three possible exceptions (Utilities $XLU, Technology $XLK and Communications $XLC). The trajectory of nearly every sector has turned over, with those notable exceptions.

And after a brutal stretch, likely a function of the race higher in interest rates, Utilities seems to be working off deeply “oversold” conditions as quantified by the short-term RSI (bottom panel of the chart below). The RSI simply quantifies up days versus down days…in this case, over the past 14 days (which is standard). Numbers above 70 are typically associated with “overbought” conditions and 30 with “oversold.”

This last bit is even more evident on the daily RRG® rendering, as $XLU’s relative strength momentum has bottomed, with the trajectory headed in the direction of the blue Improving quadrant. In other words: longer-term I have no clue the direction of the Utilities sector, but it is not surprising to see it “bounce” right here.

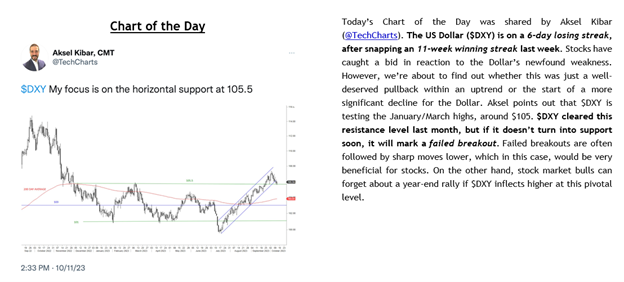

One final comment to make regarding the U.S. Dollar and seasonality. Recently, a strong USD has been a huge hindrance to stocks, but it appears that the DXY is on the verge of a “failed breakout,” something which would potentially add a tailwind to some favorable seasonality trends. In other words, do not be shocked to see stocks drift higher from here despite the horrific scenes playing out overseas. Especially given the fact that the S&P 500 has bounced off a very important support level, it’s 200-day moving average.

Have a good weekend,

-Erin

Erin M. Hay, CFA, CMT

Private Wealth Advisor, Portfolio Manager

A graduate of the University of Oklahoma, Erin began his investment management career with J.P. Morgan Private Bank. There, he worked with portfolio managers, traders and asset class specialists to bring tailored investment solutions to his team’s high net worth clients. However, intellectual curiosity would dictate both a change in geography and job description.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.