Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

“Boring Alert” – Understanding the role of the credit markets (in a way that’s not boring…)

By now, everyone is familiar with the Paycheck Protection Program (PPP), the CARES Act and Economic Injury Disaster Loans (EIDL) because they are aimed at helping everyday people. But today I want to help people understand what happened with something else that was also a big deal – the Fed credit lending facilities.

Even though they are not designed to help everyday people with direct money, they are important to everyone, none-the-less.

Before I get to why, a disclaimer: People reading this who are really smart about the Fed are gonna have to cut me a break on my 3rd grader understanding of all this – I’m simply trying to make this understandable by the general investor and its impact on the market.

So don’t hate, okay?

Back on March 23rd (the date the market started its reversal), the Fed launched two corporate credit facilities. These facilities allowed the central bank to LEND DIRECTLY to companies that had investment-grade debt. It also facilitated a mechanism to BUY their debt in the secondary market (meaning not directly from them).

The facilities total $750 million.

Size of the whole investment-grade debt market?

$5.7 trillion.

$750m/$5.7t = ~13% of the market.

But then, in April, they expanded the deal to include investment-grade bonds that fell into junk status AFTER March 23rd.

In industry lingo, they were targeting BBB-rated debt, the lowest rating a bond can have and still be considered “investment grade.” After that, they are considered BB or High Yield…or as Michael Milken would call them, “Junk Bonds”.

So what, right?

Well, the Fed was worried about BBB getting downgraded from “investment grade” to BB junk. It would be bad if that happened. Again, keeping it at a high level, if big institutions are prohibited from owning junk bonds (and a lot, if not most, are) they would have to sell those bonds.

It would cause a big problem. If you are not investment-grade, you probably can’t borrow any longer. The fancy term for that is “dislocation,” so if you hear that, that’s what they are referring to.

So, the Fed stepped in to backstop that. Additionally, of the four levels of investment-grade debt; AAA, AA, A, & BBB, there is more in BBB than any of the other four.

So, it’s a LOT of money. In fact, of the $5.7t in investment-grade debt, BBB accounts for about $3t. It makes sense this is what they were targeting with the facilities.

They also did something similar in the ETF markets, coordinating to buy up to 20% of the available investment grade AND high yield ETFs.

While there are a lot of people screaming that the Fed has bailed out the riskiest borrowers, I don’t see it that way.

Controversial, unprecedented…sure.

But it worked. It unfroze the lending markets. And that’s important to investors who look beyond the actual event.

Because the Fed really ISN’T buying the riskiest assets…If they were, they’d be buying B and CCC-rated debt or other crap. It’s also of note that they are not buying equities (although a lot of people think they should, I’m just making an observation about buying risky assets…and equities are risky assets).

One big reason the equity markets started to turn back up was that the Fed stopped the credit market from freezing by buying investment-grade credit…and seems to remain committed to that effort.

It’s boring, wonky and not as interesting as PPP, but it’s important.

There is a reason people say “Don’t fight the Fed!” and as of now, the Fed has added A LOT of liquidity into the system.

I’m also not convinced that they are done. I think there will be a lot more liquidity, loans, payments, etc., to come. This will force investors to embrace risky assets in order to find return – maybe not tomorrow, but over time.

And that’s a really important thing.

Over.

Time.

Right now, focus on asset allocations and smart equity investing because, over time, I think the equity market will be higher. The odds are in my favor on that opinion, too.

Sure, things will be interesting…As I write, people are inventing solutions to problems we never thought about in the past. And I’ll bet there will be plenty of, “Damn, why didn’t I think of that?” inventions over the next few years.

Life won’t be the same and neither will the economy. This may have accelerated the slow deaths of many industries while accelerating the creation of new ones.

Anyone out there planning to head back to the mall when things get back to normal? After figuring out how streaming works, how many people are going to the movies ever again? Anyone think that the modern workplace is going to go away or will people go back to traveling, commuting and having massive office spaces?

Hint – wait till you see what Monument looks like going forward as we continue to grow, hire, and figure out our next move with office space when our lease is up in 2023.

Industries that leverage the internet, the cloud, wireless, data centers, smart devices, services, work-from-home, video, AI, at-home learning, and tech will support a new way of living. People will still buy discretionary consumer goods – there will be new opportunities to grow portfolios.

Over time.

So…

Keep looking forward.

Dave

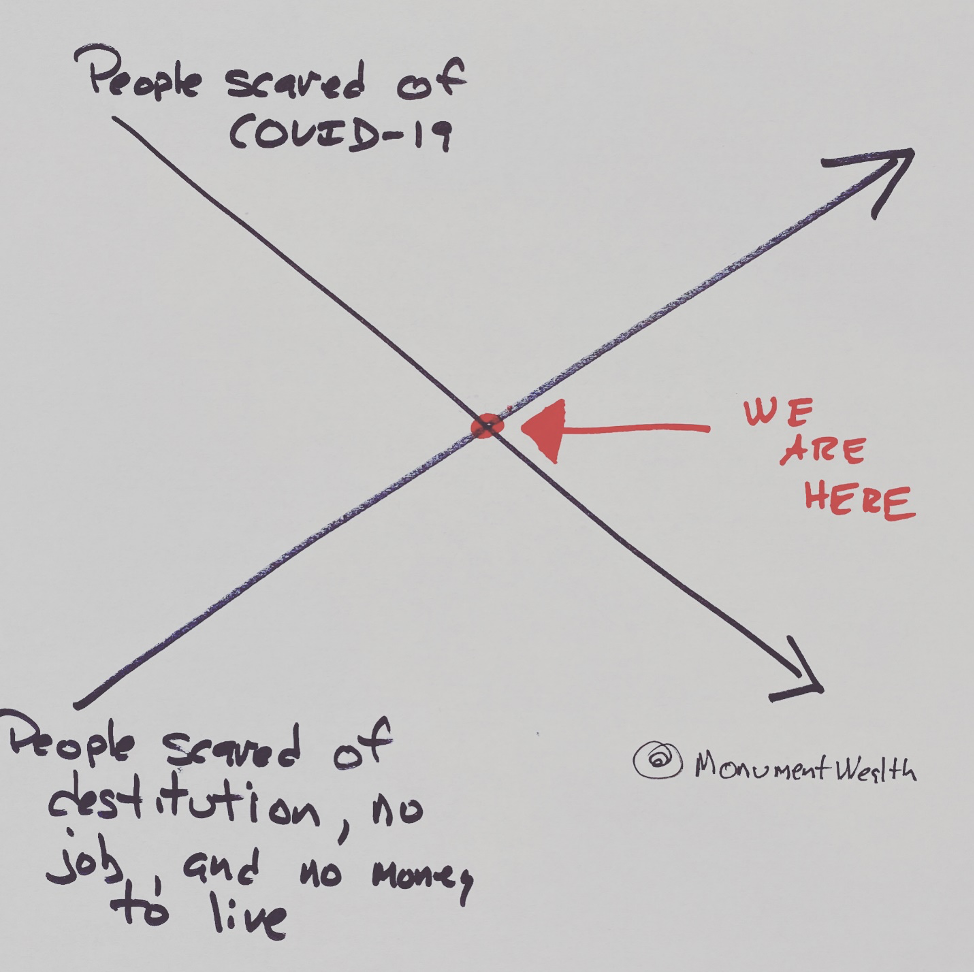

Bonus – My hand-drawn chart…I think we are here. And I think that’s a good sign for the economy.

What’s Next?

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.