Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Are You Swinging for Those “Hot” IPO Home Runs?

The market has been buzzing with anticipation for computer chip designer Arm Holdings’ initial public offering, or IPO, that happened yesterday, 9/14/23. A lot happens when a company decides to go public and lists its shares on exchanges like the NYSE (New York Stock Exchange) or the Nasdaq. There is an immense amount of background work leading up to listing day, but that’s not what’s important to me. Where I find real value is watching an IPO’s price action after its launch.

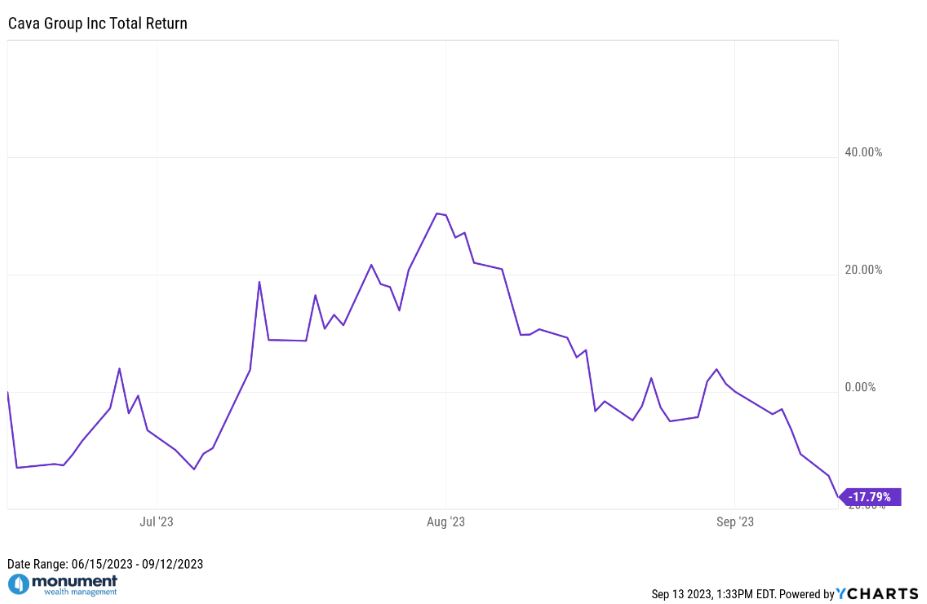

A good example is $CAVA. Back in June, I posted on LinkedIn that Mediterranean restaurant chain Cava (ticker: $CAVA) went public and was up as much as +117% during its first trading day. For a variety of reasons, investors piled in to get a piece of its potential future growth even though Cava was still a relatively young and unprofitable company.

Fast forward about 3 months to its close on 9/12/2023, and Cava has roughly a -17.8% total return since it went public. Talk about volatility – both to the upside and the downside. Investors who were chasing the potential outsized gains from this “hot” IPO, could’ve easily been burned after the initial hype faded and there wasn’t enough investor demand to support the elevated price. Without enough buyer demand, the stock price drifted lower below its initial trade price. Meaning, even those investors who got in right away and experienced the rocket ship +117% increase, would be down today if they still are holding onto $CAVA.

Admittedly, 3 months is a very short time period, and the book is not closed on Cava as a company or stock. But this type of price action, while arguably ridiculous, isn’t abnormal for IPOs. This wasn’t the first IPO to have insanely strong performance in its first trading day, followed by selling pressure that pushed the price lower over time. Not every IPO will go through this process, but I am confident that $CAVA won’t be the last.

I can see why so many investors become enamored with IPOs and other highly speculative investments that seemingly offer the opportunity to get-rich-quick. These are home run swings and if you hit one, there is no better feeling in the world. However, with home run swings, comes increased probability of strikeouts, and those can be detrimental to your financial plan’s long-term success. Don’t take home run swings if you aren’t financially stable enough to handle a strikeout.

All too often I see investors making the mistake of being overly obsessed with possible home runs. They sound great in theory but, in my experience, rarely work out. For most people, their allocation shouldn’t be dominated by home run hitters, but instead be filled with doubles hitters. If you’re a baseball fan, I’m talking about investments with a good slugging percentage. Investments that could produce solid (but likely not massive) gains while also hopefully offering lower volatility than those highly speculative investments that sometimes have gigantic gains.

My favorite baseball player to this day is Joe Mauer. He played his whole career as a catcher for his hometown team the Minnesota Twins. He had a career batting average of .306 and 923 runs-batted-in (RBIs) over his 15-year career, but he only hit a total of 143 home runs, or about 12/ per year while he played. Francisco Alvarez, a rookie catcher for the New York Mets, has 23 home runs in just his first 109 major league games this season, but he also has a batting average of .216.

Even without being known as a home run hitter, Joe Mauer was a superstar. He had the best batting average in the majors 3 out of 4 years through the 2006 to 2009 seasons and was the American League MVP in 2009. His success was largely due to his ability to avoid strikeouts and consistently get hits – especially when it mattered most to his team.

So, who would you rather have on your team? The steady, kind of boring player with a better chance of getting a hit? Or the young unknown upstart who’s more likely to crush home runs but also more likely to strike out? Which player you choose says something about your risk tolerance. For me, if it isn’t already obvious, I’d take Joe Mauer’s production almost every time because I value consistency, and normally I don’t need home runs.

My little league coach told me long ago, “Base hits win ball games; not home runs.” I’d argue the same is true for investing. You don’t need insanely high returns (home runs) to have a successful investment strategy or financial plan. For most people, all they need is benchmark or index-like returns year-over-year (consistent base hits) to help them achieve their goals. Said differently, don’t swing for the fences if all you need is a single.

Nate W. Tonsager, CIPM

Private Wealth Advisor

What comes to mind when you think of Wisconsin? Farmland? Cheese? Growing up in a small Wisconsin town, Nate can confirm that the cheese is as good as they say it is, but what shaped him most was being a part of a strong, close-knit community with a desire to help your neighbors. Nate got his first taste of the financial industry during high school...

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.