Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

You Can’t Change My Mind On This One

I don’t mean to sound the broken record alert, but I want to highlight something I wrote in a recent blog.

Pullbacks happen. All the time. It’s the cost of admission into the Investing Theme Park. Turn off the fucking financial news stations and be financially unbreakable – raise the cash you need when the markets are up, so you don’t have to sell assets when they are down. Yes, I’m a CFA Charterholder, and sometimes I like to use bad words to get your attention.

In fact, I’m not even going to link to the blog (OK, yes I will…here it is) because that was the blog. There were some charts, so it’s still worth going back and looking at, but I want to punctuate the point I was making given the continued sell-off and the recent market volatility.

In case you haven’t read a financial services industry disclosure lately, it says something along the lines of this: Investing involves uncertainty.

That may sound like a bad thing, but not only is it a good thing, it’s the whole damn point because anything certain will earn about as much of a return as a dollar bill under your mattress.

You have to assume risk to compound growth over time, again, which is the whole damn point of all this.

The trick is how you manage and reduce the risk.

Again, broken record alert: the best hedge against risk is the cash you need to fund 12 to 18 months of the things you need, so that you do not have to sell assets when they are trading down.

Now, people will argue that cash is subject to a negative rate of return after inflation. They are not wrong, but I will counter that all other vehicles that provide hedging for risk (like options) probably cost more than that, even with today’s inflation. Coupled with the emotional stability that cash provides, it’s my preferred method for managing risk.

I will entertain debate, but you will never change my mind.

With that all said, it’s important to remember a few things when assessing current market volatility and the emotions that go along with seeing your portfolio go down from an all-time high.

- Since 1980, the S&P 500 has had positive calendar year returns 32 out of 42 years…that’s 76% of the time.

- Over those 42 years, the AVERAGE decline from peak to trough is -14%.

- From January 1, 2020, to January 1, 2022, the S&P 500 index return was 224%…READ THAT AGAIN.

- As of this afternoon, the S&P 500 is down roughly 11.7% year-to-date…or in other words, for some perspective, the S&P 500 is at the same level it was on July 20th, 2021.

So…investors in the market (using the S&P 500 here) have a 76% chance of positive returns in a calendar year. We are down 11.7% compared to an average drawdown of 14%, and that’s off a 224% return over the last two calendar years.

I’m not dismissing the pain and anxiety this market is causing, nor am I saying it won’t get worse. It may.

But don’t lose your head here.

If you could get a 76% chance of winning at blackjack, you’d stay there all year, never leaving the table.

You would expect to lose an average of 14% from your stack of chips at some point, and the fewer chips you had when that happened, the more you’d feel it.

But if you were sitting there since January 2020 and grew your pot of chips by 224%, you probably would not even feel -11.7%…or even -20%.

It’s impossible to have a portfolio where you are protected from all of the different risks. You cannot have a portfolio that protects you against down markets, rising rates, catastrophes, recessions, expansions, deflation, down markets, falling rates, increasing oil, decreasing gold… you get the point.

The closest thing to a portfolio that protects against all that is cash.

It’s all about accepting compromises. The most basic example of this concept is the compromise or tradeoff between time and compounded returns. You are trading time for returns. It’s synonymous with trading liquidity for returns.

What I’m trying to express is that there is no perfect portfolio, and there is no proverbial “brass ring.” Investors who come to grips with this are likely to be emotionally capable of creating a portfolio that leverages the high probability of being right.

When the probabilities are in your favor, and you sprinkle in the benefit of letting time do its magic, you have positioned both yourself and your portfolio to do the most significant amount of good.

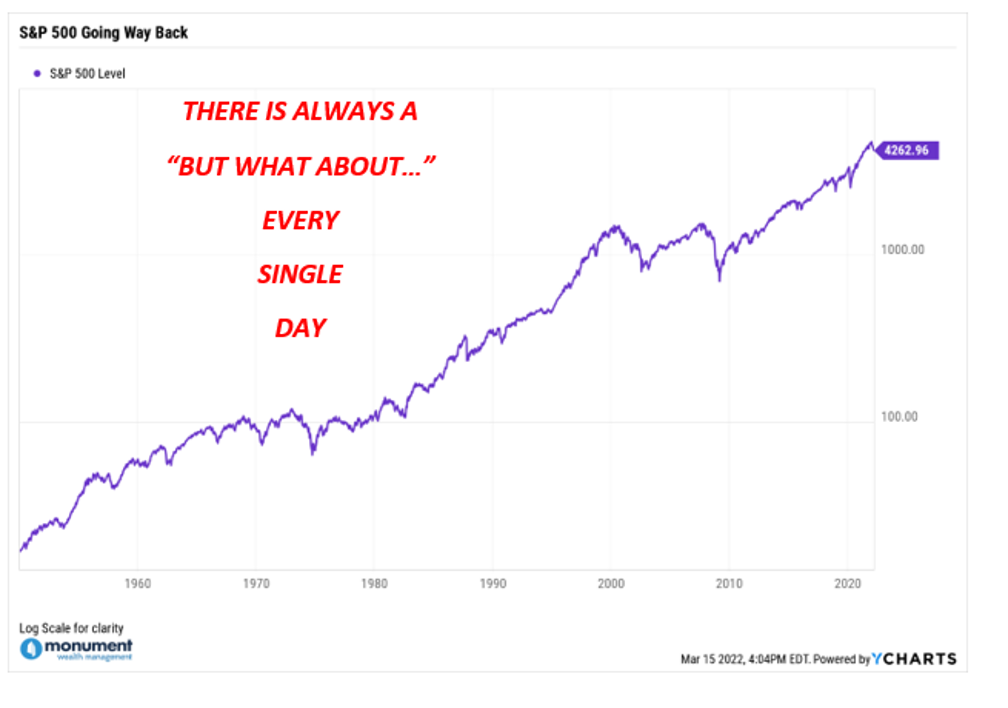

If I still have any doubters…if there are folks out there saying, “But there are new facts, the war, inflation, oil, and (on and on and on),” I say this:

There are always new facts. There is always a new “But what about…” to surface.

But the answer is here…

Keep looking forward.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

Recent Posts

By David B. Armstrong, CFA

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.