Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

What’s Up with Inflation? (And Why the Answer is M2 Money Growth)

Dork alert – this blog may be dry, but I’ll try to keep it snappy.

I know this part is just re-writing the news, but let’s start with the facts:

- The Consumer Price Index (CPI) increased 1.0% in May, well above the +0.7% that was expected.

- The CPI is up 8.6% from a year ago. This is what a lot of dorks on CNBC refer to as “Headline CPI” because, well, it’s the number you see in the headlines.

- Headline CPI is usually broken down by the same dorks into something called Core CPI, which is everything EXCEPT food and energy prices. This is done because, historically, food and energy prices are very volatile, and with inflation, there is another group of dorks trying to identify a trend. Since these two components make that hard, they are stripped out to create the Core CPI.

- Core CPI rose 0.6% in May, above the 0.5% expected. By the way, the core prices are up 6% compared to a year ago.

- Energy prices increased 3.9%…that’s probably a big surprise to those of you who haven’t been to a gas station in a while.

- Food prices increased 1.2%.

So, looking more closely at the details of the latest report, energy prices with a +3.9% increase were the biggest contributor to the higher headline CPI reading – mostly thanks to gasoline.

Then there is the war tension in Ukraine and the re-opening of China from strict COVID lockdown enforcement that assure us energy will continue to impact consumer prices into the immediate future.

Food prices, the other volatile category, were driven by prices for dairy products. Dairy products posted their largest monthly increase in fifteen years.

SO, after removing these two components, it’s clear that there is additional inflationary pressure.

For example, housing rents (which is both rent prices AND the rental value of actual homes) were up +0.6%. That’s important because rents make up more than 30% of the headline CPI, and I’m not sure rents have caught up with actual home prices, which have skyrocketed more than 30% since COVID started.

Then there are the price increases across service categories like airline fares (+12.6%), car and truck rentals (+1.7%), and hotels/motels (+1.0%).

And go ahead, I dare you to tell me you DIDN’T just sing Sugar Hill Gang “Hotel, Motel, Holiday Inn” to yourself…

Anyway, back to the dorks…prices for new autos continued to rise, and used car prices rose 1.8% for the month as well.

No matter where you look or which way you cut it, inflation is high, and it has continued to rise.

But wait, you know I have a “but”.

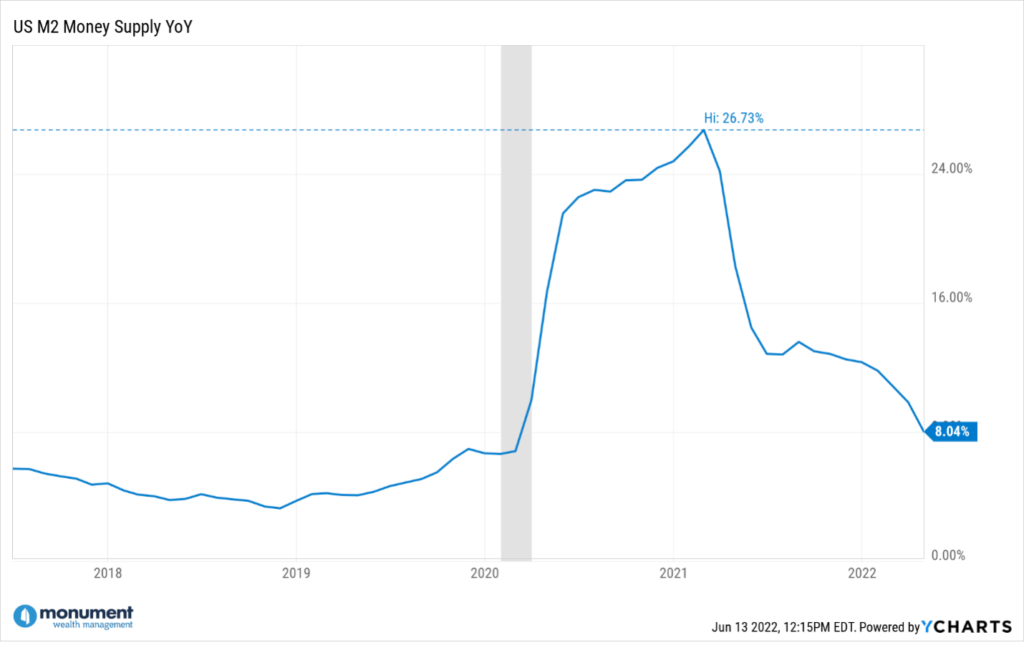

There is this thing that a whole OTHER group of dorks calls the “money supply” …AKA “M2”.

The M2 or money supply skyrocketed during COVID. See the chart below.

According to a research firm we follow, Trend Macro, there is a huge correlation between M2 and CPI, but CPI lags M2 by about 13 months.

So if M2 peaked at the beginning of 2021…and it’s now the summer of 2022…maybe…just maybe…we will see CPI come down based on M2 growth slowing.

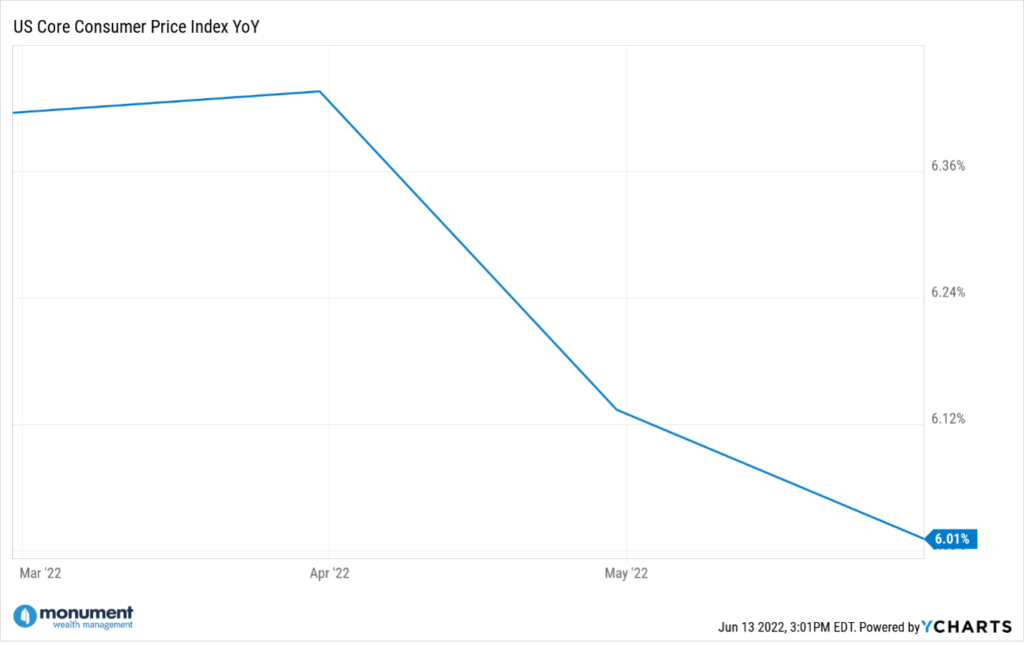

Meaning we’d need to see the year-over-year (Y/Y) Core CPI’s monthly reading start to trend DOWN.

But as I previously stated, the Y/Y Core CPI was up 0.6% in May, and we need to see the Y/Y Core CPI trending DOWN. We’d need to see something like this…

Wait, what?

Yeah, the Y/Y Core CPI has been LOWER for two straight months, almost exactly in line with the M2 downtrend that started in February 2021.

What if, and I’m just wondering here, but what if Core inflation keeps going down? Well then, all the Fed will have to do is wait.

Since most of the market tantrum we are seeing (Friday and today) is based on expectations that the Fed will take an even MORE aggressive stance on raising interest rates than was expected a few weeks ago, what happens if Chairman Powell DOESN’T get more aggressive?

Wednesday will tell all…I’m reading some dorks are expecting an increase of 75 basis points (bps), but what if it’s not?

If the Y/Y Core CPI keeps falling over the next few months in line with the reduction in M2 that started in February of 2021, it’s not inconceivable that Core CPI is back down to the Fed’s own target rate of 2.5% all by itself.

I’m not making a prediction, I’m just saying that it’s possible M2 is what was (and is) driving a lot of the CORE inflation.

And I’m saying that right now, any surprise of good news will have a similar effect as we see with the bad news.

So don’t mess around with your portfolios trying to guess all of this. Everything can change very quickly (of course, both for the good and the bad), but you can’t guess these things. Need more proof? Listen to our recent Off the Wall podcast with Dr. Daniel Crosby where he explains why.

The best news is that whether I’m right or wrong, it’s irrelevant because none of this is coupled with a recommendation to do anything. You should have the portfolio you need for tomorrow and not try to build the portfolio you WISH you had on January 5th.

Again, I’m not in the prediction business, but I am in the probability business, and no matter how you feel, there is NOT a 100% chance of anything. Someday a recovery will start, and I’m here to tell you that on March 9th of 2009, no one felt like that was the day it would all start to turn around.

And don’t even get me going on the topic of Christmas Eve of 2018.

(But if the Fed doesn’t raise by 75bps on Wednesday AND Powell is upbeat in his report, I’ll happily accept an opportunity to take a victory lap while you chant “Dork Dork Dork”!)

Keep looking forward.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

Recent Posts

By David B. Armstrong, CFA

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.