Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Vlog: Goldman Sachs 5 Questions Review

It’s no secret that interest rates have jumped a lot over the first few weeks of 2022.

While there is a lot of commentary out on it, a recent report published by Goldman Sachs Global Investment Research Group reviewed five questions they believe are most commonly asked by investors about interest rate moves and the implications for the overall equity markets.

I’m going to review TWO of the questions along with some of their charts, and of course sprinkle in my opinions which I feel are most important to the general investor…because, and no offense, but the general investor is different than the more institutional clients of Goldman.

But don’t fear, I’m here to make it relevant to you since I don’t think George Soros or Carl Icahn are tuning in to this video. But if you are, I mean, please reach out, I’d love to have dinner with you.

How do equity valuations look in light of the sharp recent rise in interest rates?

OK, one of the questions they address that is relevant and interesting to an investor is … “How do equity valuations look in light of the sharp recent rise in interest rates?”

Goldman, and I’m paraphrasing to cut to the chase, says:

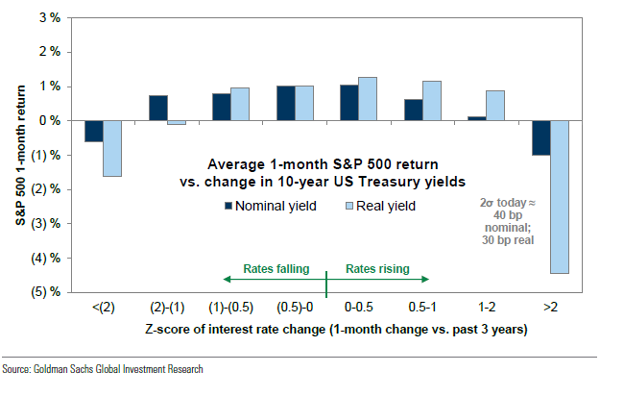

Regardless of the level of interest rates, equities typically react poorly to sharp changes in the interest rate environment, and the past week has been no exception. Historically, equity prices have declined when interest rates rose by two standard deviations or more. This is true for both nominal and real interest rates across both weekly and monthly periods. The two standard deviation threshold was exceeded on both horizons last week.

Here’s the chart for a visual, pause this if you need to dig in, but is shows all the way over on the right-hand side that it’s pretty typical for the one month return on the S&P 500 to dip between 3/10 and 4/10 of a percentage point with large interest rate changes like we’ve recently seen in the 10-year Treasury yield.

What is the outlook for growth stocks versus value stocks from here?

Another question they address is, “What is the outlook for growth stocks versus value stocks from here?”

This is a good one…They highlight that the recent rise in interest rates has accompanied a sharp equity rotation from growth and into value and that many of their clients have recently voiced expectations for an extended period of value outperformance going forward.

I’m not surprised that their clients have voiced those expectations as I have read several other articles that echo those same expectations and in fact have fielded a few questions about that from clients and other folks I regularly chat with in the industry.

I think that the tech bubble of 2000 is going to become a common point for comparing today’s environment. In fact, it already is the common point.

So, the report goes on to highlight a lot of interesting things about this outlook of growth versus value. But they also go on to say that while there are a lot of factors that support this current and popular outlook for value outperformance going forward, there’s also a couple of key differences between what we’re seeing in today’s market environment and what we were experiencing back in 2000.

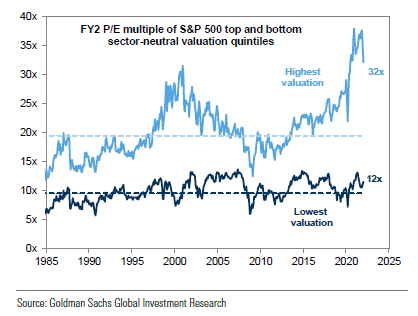

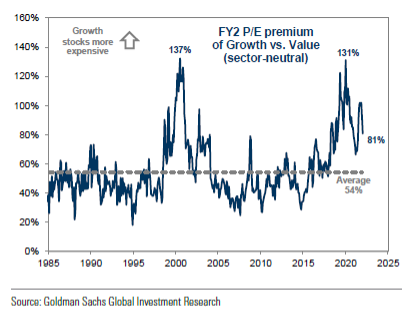

One of the similarities that they note between today and 2000, and they also feel is one of the strongest arguments in favor of value, is an extraordinary degree of dispersion that we are seeing inside of the US equity market.

They note that the valuation spread between the highest and lowest valuation stocks in the market has always been a pretty good indicator of the return potential for value, but it’s also a poor timing signal.

Check out these two charts real quick and what you’ll see is that while the spread has definitely narrowed recently, it’s still pretty wide relative to history. Pause on these next two charts if you need to dig in.

They are essentially showing the narrowing of the dispersion and the valuation premium of growth over value.

The first chart is essentially showing that that dispersion in valuation has narrowed but it’s still very wide. The second chart is showing you that the premium for growth versus value has declined but it’s still well above the average.

The report goes on to highlight that the Goldman Sachs research forecast for the continued rise in interest rates supports the outlook that value stocks will likely outperform growth stocks while interest rates are going up.

This makes sense to me, and I agree that is likely going to be the case since rising interest rates is indicative of an improving economy and economic growth. So it’s natural that interest rates will go up and that in turn will likely increase the expected earnings of value stocks over growth stocks.

It is not a function of growth stocks losing money while value stocks make money. It’s not like that. In fact, the report goes on to say that the economic growth environment of today is a little bit different than it was in 2000. Because the expectation for long-term economic growth is actually much lower today than it was back in the 2000s. It’s that whole irrational exuberance thing from way back when for those of you who remember that term. A lower expected growth rate going forward for the next ten years will be a headwind for value firms to grow their earnings. In fact, that’s probably the major reason why growth stocks have done so much better over the past ten years then they have over anytime that I can remember and probably longer. So this likelihood of slowing economic growth going forward is actually an argument in favor of growth stocks.

There’s no rocket science here. It just makes sense to me and I agree with them.

I also agree that this is a horrible indicator for timing.

Have a solid portfolio.

I’m again going to beat the drum on following a process, following a plan and keeping all the pistons in your engine firing to keep the car moving forward at the speed that makes sense for your plan and risk tolerance.

Do not under any circumstance wholesale eliminate the exposure to growth stocks and load up on value stocks. That would not be smart. Period. Now it’s my opinion and I could be wrong, and I get it, but hey, you know me—you’re always going to get my unfiltered opinion. The good news is it really doesn’t matter if I’m right or wrong if you have a good, solid portfolio.

Look, this is all interesting stuff. I love it. Lots of people love it. But it’s nothing more than just interesting stuff to know about and to use as a tool to evaluate what you’re doing with your own portfolio. Just use it as a litmus test. You either do or do not have a good portfolio. Don’t mess with it any more than that.

That’s it, reach out with questions and as always, keep looking forward.

Dave

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

Recent Posts

By David B. Armstrong, CFA

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.