Explore Our

“Off The Wall” Blog

Read our Private Wealth Advisory team’s unique thoughts on the markets and investing.

Universal Healthscare

Weakness in the Healthcare sector has been widespread on the heels of political discussions around healthcare and drug prices. Drug makers, insurance companies, medical companies and biotechs have all struggled from this. Actually, “struggled” is an understatement. While the Healthcare sector has been losing ground, one of the top performing S&P 500 sectors, Technology, has continued to outperform.

That’s just investing.

This is not going to alleviate the pain from last week’s Healthcare downturn…I get that. “That’s just investing” could be interrupted as a dismissive “Armstrong shoulder shrug,” but there is more to it.

Investing isn’t so much based on luck as it is on having a process. Using models to run different strategies is one way to have a process–one that removes luck, both good and bad. Models are central to our investing process at Monument, which is designed to consider probabilities while removing emotion and behavioral biases from the decision-making process.

Because of that, when a sector like Healthcare sells off rapidly due to speculation and emotion rather than facts, the models will never anticipate nor catch up to that kind of market action.

We can be as wrong as anyone else, but anyone with a probability-based process knows that to be mostly right, you also have to sometimes be a little wrong.

We also know that being wrong for a long time puts you out of business. Unless you are a financial news prognosticator…then you can be wrong forever. Anyway, we will be making some adjustments to the portfolio. We received a few suggestions from great clients, so thank you for those. It’s always important to hear thoughts from smart people who see things through a different lens; it really does help. Things can always be improved. The iPhone X is way better than the original iPhone because people said, “Hey, why don’t we do this?”

However, my final comment is more of a moment of introspection. You see, I can write all day long about financial and behavioral biases, and it doesn’t make me any less susceptible to them. I may catch myself more quickly than others, but I still fall victim to them.

I’ve invested in the Monument strategies right alongside clients so when the Healthcare stocks in the Growth Strategy and the Healthcare sector in the ETF strategy started selling off, I felt the pain. I felt it twice as much as the gains in other stocks. For example, Anthem (ANTM) was down -16.81% last week. Ouch.

DOWN…SIXTEEN…POINT…EIGHT…ONE…PERCENT.

Holy sh*t, that’s a lot. It’s one of the top things I was concerned about as an investor and as a Portfolio Manager.

However, there are a lot of high performing stocks in the Growth Portfolio, too. For example, year-to-date, here are the top five performers in the model:

SNPS +37.68%

ECL +24.66%

AMT + 22.51%

V +21.60%

HD +20.59%

Why aren’t I writing about those? Why am I spending time fretting over ANTM down LESS than those five are up!?

Because…losses hurt twice as much as gains, and I’m as susceptible to bias, too. I just wanted to acknowledge it.

Quick Recession and Market Thoughts

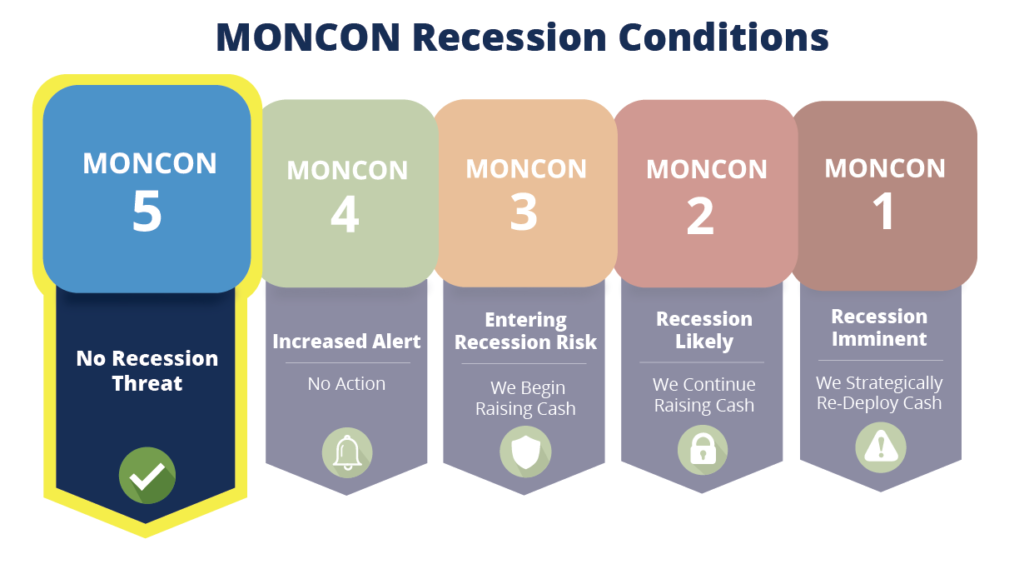

Do not confuse weakening growth with recession. Our MONCON 5 reading is consistent with our struggle to find overwhelming evidence of recession in the short term, despite the current yield curve showing some inversions. Lead times to recession from yield curve inversions are very long and widely dispersed, making them less useful for market timing purposes.

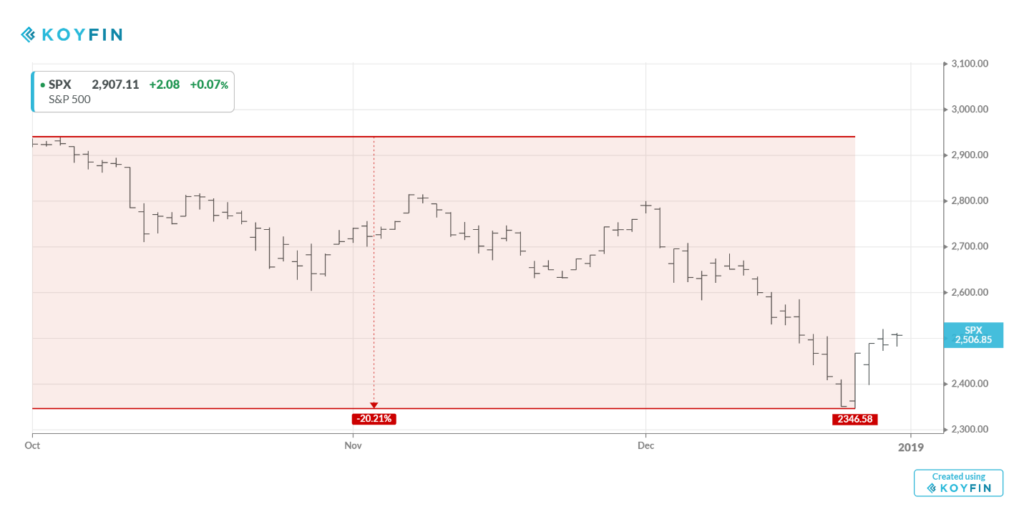

Like the equity models mentioned above, our MONCON reading keeps us from reacting…and so far, it has really kept us grounded during some scary news cycles (are there any other kind?). Remember when the world was awash in recession and interest rate panic in the fourth quarter of 2018? In case it’s a far-too-distant memory, here’s a chart from Koyfin from that time. (The top left ticker is today’s S&P 500 index level at 2907.11.)

A lot of people were panic-selling over the specter of a recession. There was a lot of emotion…and a lot of “losses hurt twice as much as gains.” However, today it seems that many people have forgotten the pain from last December.

If they did nothing, say if they had models that removed emotion coupled with a solid financial plan, they are probably pretty happy today.

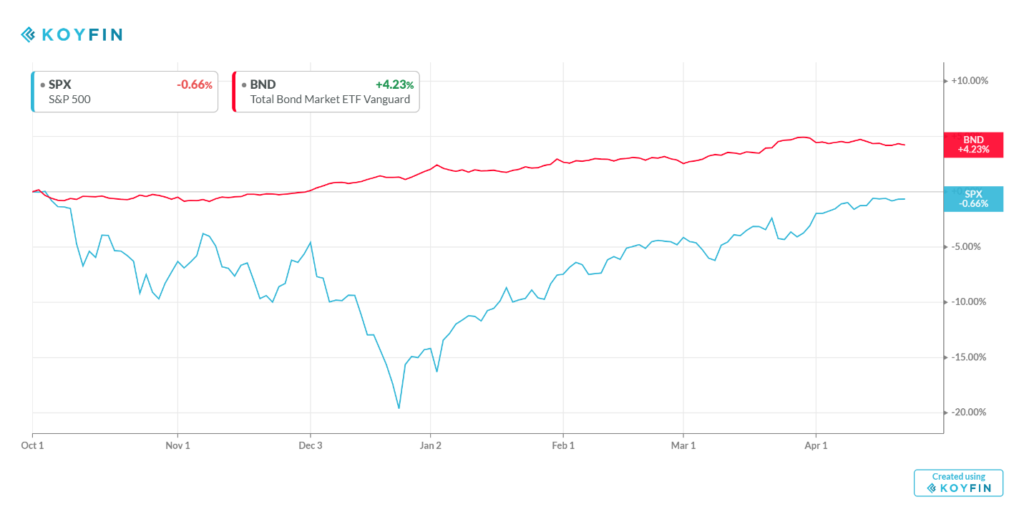

However, one way to have avoided a lot of that volatility was to have been in bonds. For example, the below chart shows the relative return of the Total Bond Market ETF (BND) in red versus the S&P 500 in blue.

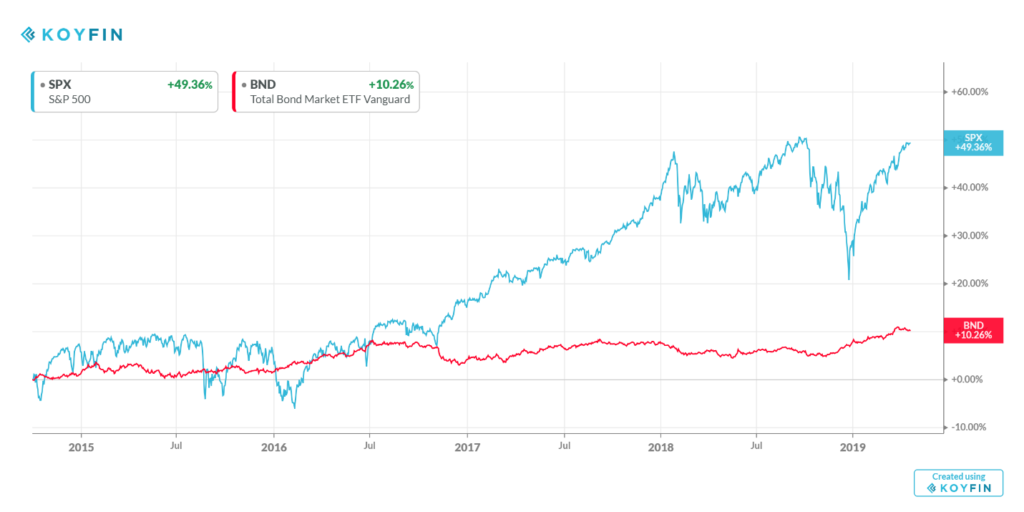

So that may prompt the thought, “Maybe I should have had bonds, look how much better they did.” Well, it depends on the snapshot of time you are looking at. In the graph above, it’s clear. But below, you’ll see another clear answer. Bonds compared to equity suck. Big time.

The real answer is that it makes sense to have both. The more time you have to let your money grow, the more equities make sense. The less time you have until you need the money, the more bonds make sense.

Never judge bonds solely by the yield or interest rates they pay. Yes, a portfolio of bonds should be optimized, but that’s not the only consideration. Be sure to consider the overall impact they have on dampening volatility if that is a goal in your financial plan.

Broken Record Bottom Line

As a general rule of thumb, have a plan that determines how much cash you need for about 18 months. From there, your plan should dictate your asset allocation and the correct combination of equity and bonds. Having models after the asset allocation is determined keeps emotion out of the game.

Like we just saw in healthcare, models won’t time everything perfectly, but it increases the probability that we are going to be mostly right even when sometimes we are a little wrong.

We remain at MONCON 5. Let’s see how GDP comes out this Friday…I suspect it surprises to the upside and that will reward patience and discipline.

Keep looking forward.

Dave

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA®

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.