Explore Our

“Off The Wall” Blog

Read our Private Wealth Advisory team’s unique thoughts on the markets and investing.

A Tug-of-War Between The Bulls and The Bears

I’m seeing, reading and hearing a lot of back and forth between people on where this market is heading and frankly, there are a lot of data that are supportive of both camps. People who are beating the bull drum have been highlighting the restrained investor sentiment, fair valuations, the improvement in the U.S. Dollar that is supportive of better earnings in the future and the still growing, yet tepid, economy. Bears, on the other hand, are underscoring that valuations may be strained by poor earnings outlook, China drama, the Brexit (Google it since I’m not getting into it in today’s blog) and the U.S. election spectacle (I’m DEFINITELY not getting into that – people are getting beat up for just having an opinion these days!).

So what do I think? Well, I think both sides have valid concerns, but I come down on the side that the current outlook for growth outweighs concerns that a bear market is around the corner.

For now.

We will eventually have a recession and that will coincide with a larger market pullback, but as I’ve been saying for a while now, the usual data suspects that pop ups prior to a recession are simply not rearing their ugly heads a this time – there is no over-confidence, over-spending or over-borrowing, no severe interest rate increases and no commodity spikes.

For some background, be sure to see my last economic update video where I go over some of the bigger reasons I see things in a more positive light and address all those ugly heads.

I think the last few weeks have been very interesting because while there has been a mix of economic news and certainly some increased global risk, the markets appear to be rather…dare I say…resilient. Despite concerns such as the recent U.S. labor market, which I discussed in last week’s blog, the upcoming BREXIT vote, and doubt surrounding future Fed policy, stock prices have not sold off.

We will always need to withstand the near-term risks. While it’s true that the market has rallied hard since mid-February, the medium-term and long-term position for equities remains upbeat in my mind…especially if we see the progress in corporate earnings that I’m expecting.

Oil

Oil remains a big factor in the economic outlook and for earnings. There are a ton of different ways to look at this but here is a basic, elementary thesis…when things are cheaper to make and ship because oil prices are low, that’s good for earnings. Someone with a Ph.D. in Oil may have a more complicated thesis, but I think mine is kinda sound.

Let’s start with gasoline.

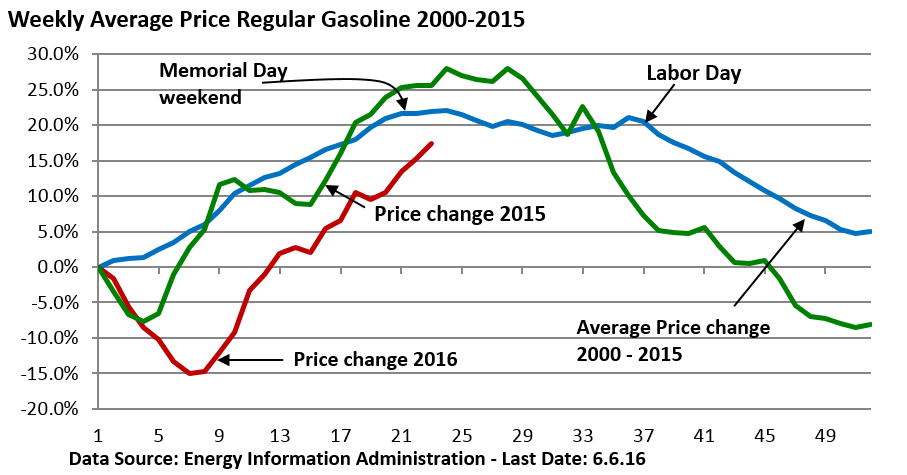

The price of regular gasoline across the U.S. bottomed at $1.73 per gallon in mid-February. While the price has risen off that February low, data reveal the average price over the Memorial Day weekend was $2.34. That’s still a pretty sweet price relative to the last few years.

If you are like most people, you’ve noticed that gasoline prices predictably rise during the spring. There is a seasonal aspect in the gasoline price equation.

That said, taken in perspective, gas prices are still looking pretty good. The chart below is from Charles Sherry. The green line is 2015, the red line is 2016 and the blue line is the 2000-2015 average.

The biggest determinant in the price of gas is the price of oil.

Duh – right? Here is the deal. About 42% of the price of gasoline is determined by the cost of oil, and oil prices have nearly doubled since bottoming in mid-February. Oil is currently hovering roughly around $50 per barrel.

So the natural question is, “What’s pushing the oil prices higher?” Well since there are several different factors, I’m going to focus on some of the big ones.

- U.S. gasoline consumption is currently up year-over-year. There is also data showing that there are year-over-year increases in key emerging markets like India and China.

- In addition to consumption, there have been some supply disruptions. Libya, Nigeria, Venezuela and Canada come to mind. Canada had that huge fire and Libya, Nigeria and Venezuela have, well, Libya, Nigeria and Venezuela stuff going on.

- Then there is the U.S. oil production that is expected to fall by 700,000 barrels per day this year as lower prices limit drilling/fracking.

- Finally, don’t forget about the U.S. Dollar. Oil is priced in dollars when sold around the globe. The recent dip in the dollar is interconnected with rising oil prices.

However, even given all that, supply disruptions could diminish and with oil near $50 per barrel, we could see fracking production stabilize (and even rise?). Both of those situations could put a cap on prices.

I realize that seasonality could reaffirm itself during the fall, but for now, higher prices have been a plus for the suffering oil industry and it has contributed to the rally in stocks. This in turn helped to calm anxiety in the junk bond market.

The bottom line? We are well off the bottom in prices but the current prices are still rather acceptable.

Quick Tips for Success Right Now…and Always

Just a few quick thoughts to help you frame a construct for success given where we are right now:

- The single greatest weapon an investor can wield is patience.

- Curb your emotions since the markets have none – they are merely a reflection of collective emotion.

- If you are looking for excitement, go take a weekend out in Vegas.

- If you are looking for drama, go binge watch a season of the Kardashians.

- Follow a principled strategy – chasing things you wish you had when you didn’t have them will only cause problems.

Have a great week – call with questions.

Important Disclosure Information for “A Tug-of-War Between The Bulls and The Bears”

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

Subscribe to our blog here!

David B. Armstrong, CFA®

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.