Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Traits of short-term investors

It would be great if we could identify the market bottom and time every buy-and-sell trade to perfection, but the reality is that those who try are often rewarded with nothing but regret.

Buy too early and stocks continue to fall = Short-term regret, pain, and second guessing.

Buy too late after stocks have recovered = Short-term regret, pain, and second guessing.

There is a common chorus among investors, “Why not just invest in the S&P 500?”

While that sounds easy, in reality it is rife with complication and its simplicity and effectiveness are often the casualty of investor meddling.

In market and economic environments like this, people start to overthink things and I think that’s when a lot of damage gets done. There is often both panicked selling and delightful overconfidence at the wrong moments.

These behaviors weaken our chances of real success…and make people poorer.

Despite the repeated reminders not to try to get too smart for their own good, a lot of investors still believe they have some sort of superpower – the ability to know what’s coming next. It’s proven every year in something called the Dalbar Quantitative Analysis of Investor Behavior, or QAIB.

According to Dalbar, the QAIB uses data from the Investment Company Institute (ICI), Standard & Poor’s, Bloomberg Barclays Indices and proprietary sources to compare mutual fund investor returns to an appropriate set of benchmarks. The study utilizes mutual fund sales, redemptions and exchanges each month as the measure of investor behavior.

The 2019 report shows that in 2018 the average investor underperformed the S&P 500 by 5.04%. (I’m thinking the 2020 report on 2019 should be out shortly.)

Here’s a look at longer-term underperformance from a New York Times article in July 2019. It shows that the annualized return of the average mutual fund investor underperforms the S&P 500 by 88 percentage points over 30 years, 46 percentage points over 10 years, and 35 percentage points over five years.

Annualized – not total, ANNUALIZED.

The real superpower is patience and discipline, but I know it’s hard to stay disciplined and keep a long-term perspective when the media is barraging us with daily news. That racket draws our attention and tempts us to DO SOMETHING.

But “doing something” is often times the worst possible response to the short-term news. Presuming you have a well thought out financial plan and investment strategy specific to you and your unique needs, doing nothing is almost always the best thing to do.

This is why we advocate for having a wealth plan, identifying your cash needs so that you are not forced to sell during a crisis, and having an appropriate investment. A wealth plan should provide you with the level of comfort necessary to DO NOTHING. Doing nothing ensures you are properly invested during the recoveries which come more quickly than most people realize.

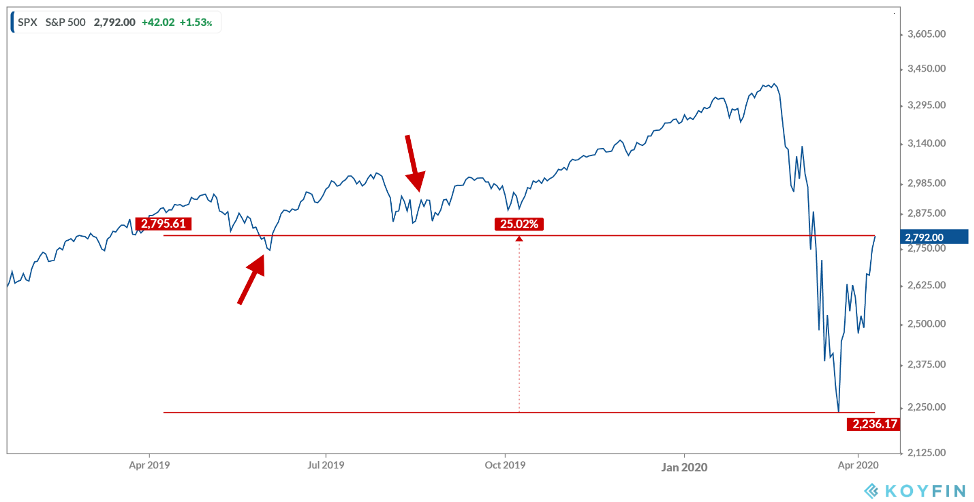

Right now, the market is back around where it was last summer. Hardly crushing. If you didn’t think your portfolio value was horrible in August of 2019, I think you are probably okay.

We are not out of the woods yet, but those who have weathered the storm so far have seen a nice recovery, that is if it can hold and continue from here. See this chart for what I mean.

Keep looking forward,

Dave

What’s Next?

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.