Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

This Greek Drama Has No Mask

Just like that friend who keeps saying they hate drama by over-dramatically complaining about it on their Facebook feed … the Greek drama continues. While we all use Muses for different things, I will attempt to draw on all nine Muses of Zeus for inspiration in writing my blog, because what else is there to say about this subject? Jimmy McMillan in the picture kind of says it all, but I’ll try.

Greece

At the heart of the problem, Greece simply has way too much debt relative to its capacity to be able to repay it. If Greece were Colt Defense, LLC or a 2008 Detroit-based unionized American automobile company, this would simply be a case of bankruptcy and reorganization.

Here’s the rub – everyone in the European Union (outside Greece) finds the idea of debt relief … how do I put this without inserting the “F” word … unreasonable. Of course Greeks find the idea of reform plus austerity without debt relief even more (again without an obscenity that begins with “F” and ends in “ing”) unreasonable.

It seems obvious that the solution is reform in exchange for debt relief, but the issue is now much more of a political one than an economic one.

What’s interesting is that euro-zone officials are formally discussing a Greek default. This is a first, and I think it probably has a lot to do with strategy, public posturing and maybe even a little bluffing. This is ratcheting up some short-term volatility and has caused tension to rise between Greece and its creditors.

So what’s our guess? Probably another short-term deal that puts off the tough decisions to a later date. It’s possible that we actually see real reform that helps put Athens back on the road to success … but don’t hold your breath for that outcome. Those odds are extremely unlikely.

As for an actual default? Well, while rising, the odds of an outright default remains relatively low since both Germany and the European Central Bank actually want Greece to stay in the European Union (there are 19 nations that share the Euro as its common currency).

If Greece defaults, we enter uncharted territory and the consequences in Europe and beyond are unknown. Since no one can predict the outcome, equity investors will have to ride it out. See some of my recent advice here, or if you really want to go back in time, see my thoughts and advice in this blog from 2011.

Economic Data

We have written extensively about how economic growth slowed sharply over the cold winter months. Like Stannis Baratheon’s food supplies in Game of Thrones, good economic news was in short supply. However, recent data are finally signaling a long-awaited pick-up in economic activity.

Initial claims for unemployment compensation, which is a good leading indicator of economic activity, has been holding at pretty low levels over the past few months. First-time claims have been below the historically low level of 300,000 for 14-straight weeks. Since layoffs are low (otherwise that initial claims number would not be low and would probably be going up), it’s a sign that companies are holding onto workers among stronger activity.

During the first week of June, employment jumped by a solid 280,000 in the month of May. This marks the 14th month over the past 15 where employment has risen by over 200,000.

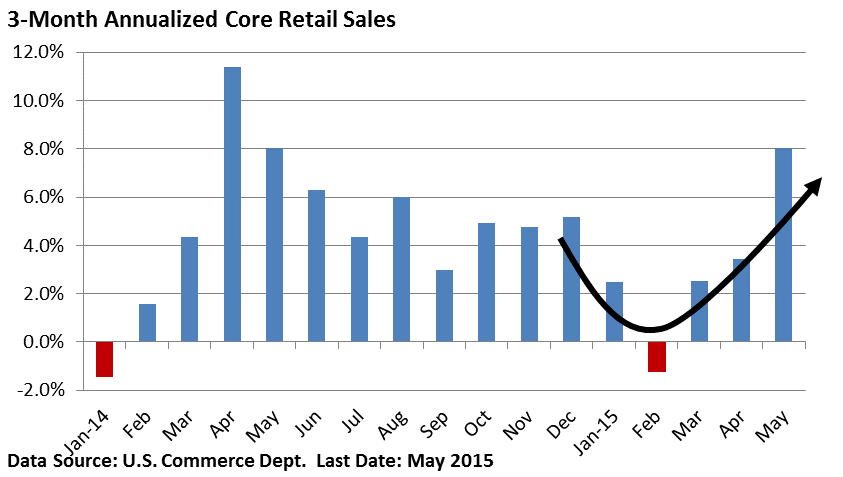

Next we have some retail sales data. Last week’s report revealed that retail sales rose 1.2% in May. If you remove auto sales, which can be volatile on a month-to-month basis, and gas station sales, which help filter out the wide swings in gasoline prices, then so-called core sales were up a very respectable 0.7%. We wrote about hot car sales in this recent blog.

Keep in mind, we need to be careful about taking monthly numbers out of context, because we can get volatility on a monthly basis that shrouds any trends. The chart below shows that the three-month annualized rate for core sales, which evens out some of the volatility, is signaling that consumers are re-engaging. The arrow swooping up is a good thing which any self-respecting Gen-X’er from Northern New Jersey would tell you, “No Doi.”

What to Do Now

If you know you will need cash for something over the next 12-18 months, either raise it now or have a plan to access it in a way that will not be swayed by any potential market pullback. If you have cash to invest, use market pullbacks to get it to work. If you are fully invested, plan to stay that way. You should be a long-term investor, and should not be messing around guessing about things that may or may not happen.

Please call with questions.

Important Disclosure Information for “This Greek Drama Has No Mask”

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.