Explore Our

“Off The Wall” Blog

Read our Private Wealth Advisory team’s unique thoughts on the markets and investing.

The Kevin Dilemma

If you planned on winning Buffett’s $1b Bracket Challenge, you may have had the same reaction as Coach K in this picture. Even still, you probably enjoyed making Thursday and Friday a completely unproductive day for your employer. Wait, what? You thought you’d win the Buffett $1b Bracket? So did I…for like five minutes. I had huge plans to become my own biggest client. But there was that Kevin Dilemma too…

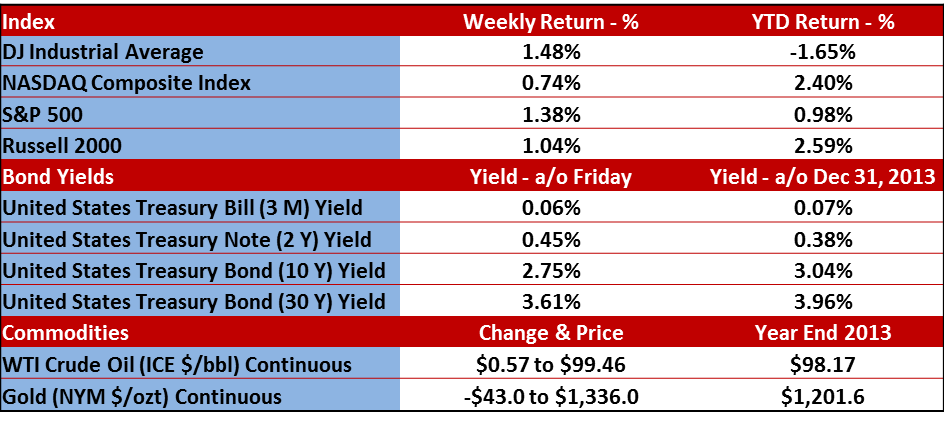

By the weekend, all of the $1b brackets were busted…What a relief to a guy with $64b that he didn’t have to pay that out, huh? But it’s funny that I think more people know that number three seed Duke lost to number fourteen seed Mercer than know that the S&P 500 had a 1.4% gain for the week. And for those of you into politics more than basketball, I’ve included a bracket for you to fill out over the next year or so. Thanks to Charlie Daniel, Knoxville News Sentinel.

So since I know no one really cared about anything having to do with Yellen’s first public, post-Fed meeting appearance, Crimea, China, the effectiveness of the P-8 Poseidon, etc…I’m going to just focus on March Madness this week and tie it into investor behavior, outlook and discipline. But before I get into all of that and an explanation of the heretofore obscure and relatively unknown Kevin Dilemma, here’s how the big indices faired for the last week.

Starting last week, the field of 64 teams began playing to see who would be the NCAA Champion. Everyone probably knows what a bracket looks like and how each of the four divisions are “seeded” from the first seed all the way down to the sixteenth seed.

Trivia: this seeding system started in 1979 and was an effort to make sure that the best teams did not meet each other until later in the tournament. Good business, actually—especially for TV and advertisers.

Once the games start, every office is abuzz with picks, brackets, and attempts to predict the “spoilers” or the upsets. Even those who do not follow a single game all year get in on the action and even the biggest amateur knows it’s not a good pick to select a number sixteen seed to beat a number one seed. In fact, there has never been a number sixteen team that beat a number one team in the history of the tournament.

The number one seeds usually have better players, better coaches, and better facilities at their schools than the number sixteen seeds. Given all of that, it has been a bad bet to select a number sixteen to beat a number one seed.

I’m not saying it will never happen; I’m just saying that it’s not a good bet.

However, every year, some low-seeded team pulls off an upset. This year it was number fourteen seeded Mercer who knocked off the number three seeded Duke Blue Devils.

Teams like Mercer are called “bracket busters.” In fact, in 2011, a number eleven seed (the VCU Rams) made it all the way to the Final Four!

Over the course of the past 27 years, there are a decent amount of number twelve seeds that beat number five seeds, but over the long run, the number five seeds win more than 50 percent of their games, while the number twelve seeds win only about 34 percent of their games.

Even when knowing these stats, everyone seems to spend all of their time looking for the upsets.

Flip on any sports TV station and they are all talking about the “bracket busters”…both the predicted upsets along with the actual upsets (ahem…Mercer!).

But, what people should be looking at are the teams that have the best chance of winning the whole championship, and that means looking at the teams that are most highly seeded, because they have the best chance of winning it all.

The same goes for investing. It’s always fun to try to pick the long shot. People always feel so smart when they pick the dark horse investment, but they lose sight of how important it is to pick the winners that will go the distance. It’s the investments that have the best chance of winning over the long haul that will provide investors with the greatest probability of success over the long term.

I’m not saying that investors should not pick a few investments from time to time that are long shots, but that risk must be controlled.

Having a financial plan that focuses on the long term is the first step. Having an asset allocation and investment strategy that corresponds to the financial plan is essential as well. These are your top-seeded teams.

If after you have your financial plan and investment strategy fully implemented and funded, you find that you have some surplus money, go ahead and pick some long shots. Also, do it in an account that is not co-mingled with other managed accounts. But keep in mind that overconfidence is one of the most destructive forces an individual investor can fall victim to.

But if you had made it with a perfect bracket all the way to the Final 4, what amount of money would you have taken from Buffett / Quicken Loans to walk away from the chance to win $1b?

It’s called the Kevin Dilemma. Why? Because I had this conversation with my friend Kevin. I told him I’d want $10m to walk away from the chance to win $1b. He argued that most people were likely to take a payment much smaller. Call it the “Kevin Dilemma” or the “Bird in the Hand” Dilemma, but given the amount of over confidence I’ve seen people have in their own stock picking ability leads me to believe that anyone who only had to get three more games to go their way would want a lot of money to walk away.

Continue to enjoy the games – at least we don’t have BTR’s rolling down the streets.

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA®

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.