The Future of the Economic Recovery Will Be Decided by Another Lockdown–Is One Coming?

I believe that if fatalities stay in their declining trend, the likelihood of a second public lockdown stays low and the economy will continue its recovery.

The topic of COVID cases increasing has become a touchy one…and I think a lot of it has to do with media coverage, politics, the upcoming election and, a trust factor. It’s really becoming harder and harder to know what data is true or not and what sources are an actual authority.

There are so many angles to this that I want to focus in on the one thing that I think is important to what Monument does every day – provide straightforward opinion and unfiltered advice as it relates to financial planning and investment management. So, I decided to look at it from the perspective of “What does the data say about the PROBABILITY of the US economy going back down into a lockdown like we saw earlier this year?”

I understand there is a personal element to all of this – real people with friends and families are getting sick and even dying. I’m not dismissing that aspect of this epidemic, I’m just taking a look at a small sliver of this and offering an opinion.

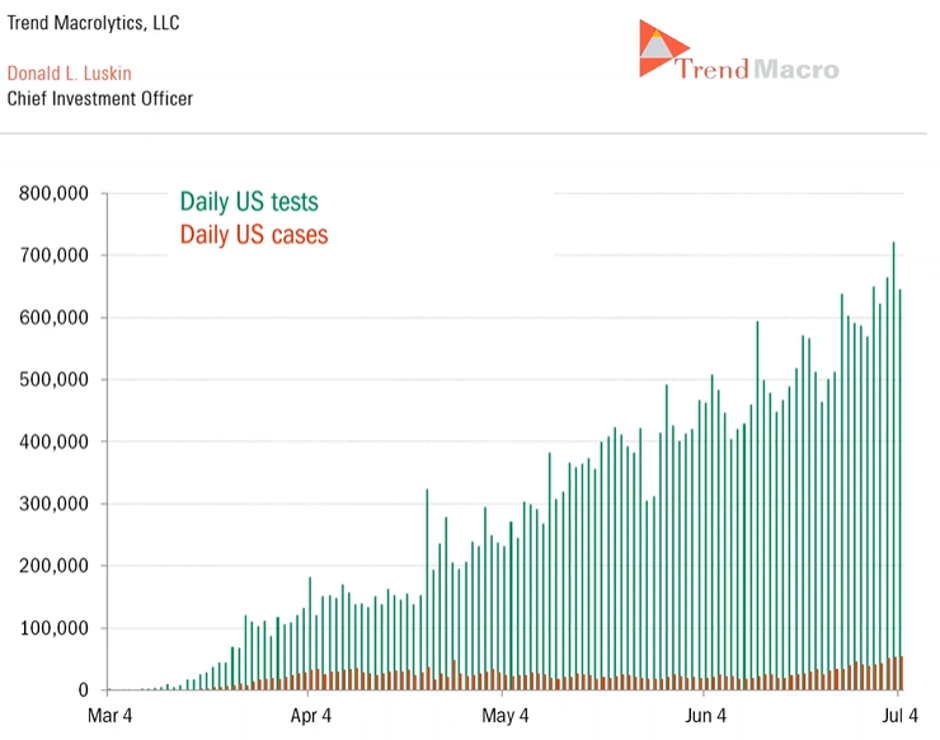

It is undeniable, there is a surge in positive tests, but a common theme I keep hearing is that it’s only natural that the number of positive results will increase as the number of test increase. That’s not wrong, but to me, it’s more about the positive RATE. See below chart from TrendMacro

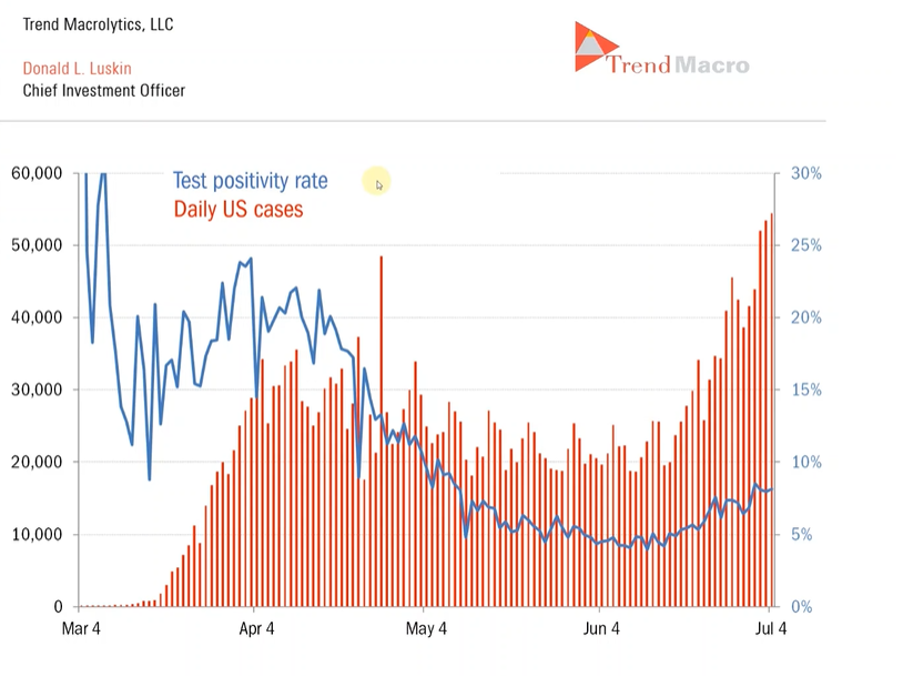

It makes COMPLETE SENSE that the orange line (cases) is trending up because the green line (tests) is going up. BUT, we need to consider the RATE…the number of positive cases divided by the number of tests. Again, see TrendMacro chart.

We are doing 650,000 tests a day (first chart), so we are definitely going to get more cases – nothing wrong or seemingly controversial about that statement or observation. Above, we see the blue line which shows the RATE…and that’s increasing too. It looks like it hit its low in June around 4% and now it’s doubled to about 8%.

So, we are doing WAY more testing and we are seeing a rise in the positive rate.

Not good – the disease is spreading and the test positivity rate has gone up.

But this is where people start debating…but forget all the back and forth bickering about sample bias, the double and triple counting of positive results (which is factually happening), the abundancy of tests available now vs March, and the likelihood asymptomatic people are now getting tested…I don’t think cases and positivity rates matter when it comes to the economy.

OK. So, what DOES matter to the economy?

Well, in the short-term (meaning between now and any vaccine) I think the economic outlook hinges on whether the population gets locked down again.

And any second locking down will most likely depend on fatalities increasing.

Again, I get it, from a societal perspective, it’s not good to see it spreading and increasing, but I’m focusing on what I think it means for the economy.

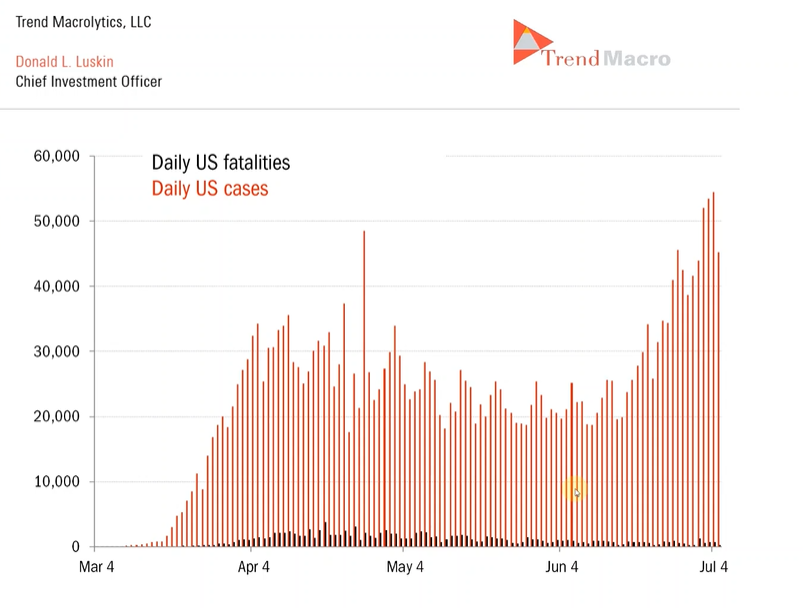

For that, see this chart-

Fatalities (black bars above) look to have made their highs in April and thankfully have been on a generally steady decline. The good news is that for three months, even as positive cases and the positivity rate have risen over the last month, fatalities have not.

My opinion is that we will not see a lockdown as we had in March and April materialize unless that fatality rate starts to spike up.

That could begin to change and if it does, then the likelihood of public lockdowns remerging increases along with an increase in the fatality rate…and that will be bad for the economy.

As always, the best way to hedge against my opinion being wrong is to know your cash needs for the next 12-18 months. If you were kicking yourself for not raising cash (otherwise referred to, “I knew we were at a top, damn it, I should have sold”) in Feb, I think now is a great time to reassess that idea.

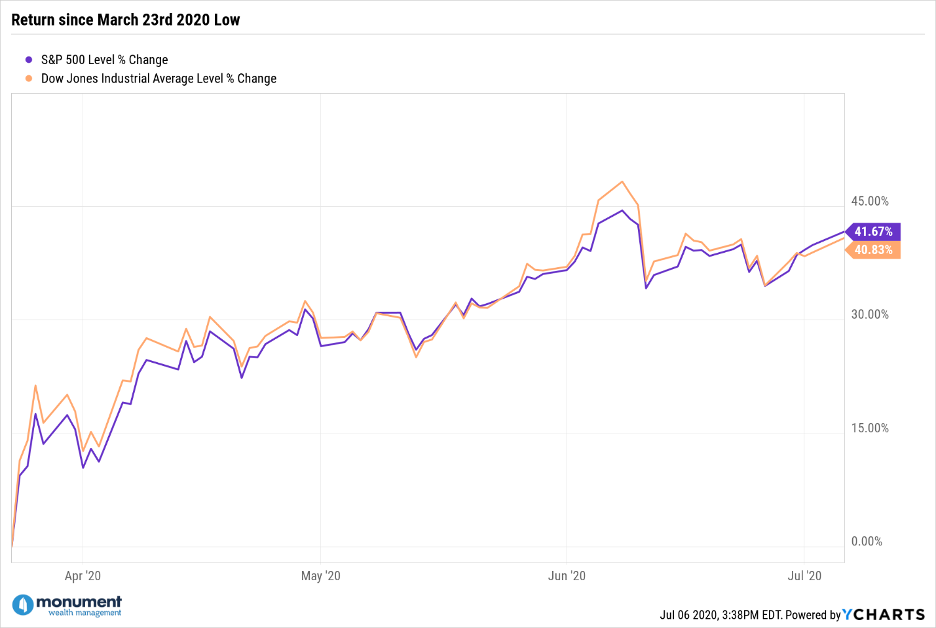

Consider these two charts, specifically the S&P 500 – we are up close to 42% off the low set on March 23rd and, we are only off -6.35% off the high of Feb 16th.

If you need cash, now is a great time to formulate a plan. That plan should include thinking about selling any securities trading at a loss from where you bought them…raise cash and get a tax break too.

Remember, when assessing whether or not now is the right time to convert equity exposure into cash, I think it’s more constructive to focus on the CURRENT OPPORTUNITY rather than nailing THE PERFECT TIME (which only materializes itself in hindsight).

Investing is rarely just about making more money. It’s usually more of a balance between protecting capital, planning for cash needs, AND making more money.

Build a solid, all-weather plan because there will always be things to worry about…the November election, 2022 midterms, 2024 election, 2026 midterms, 2028 elections. You get the point.

So just keep looking forward,

Dave

What’s Next?

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.