Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Is it Really The Death of Equities?

For some reason the markets just do not seem to care much about headlines – President Trump ending ACA cost-sharing payments…U.S. maybe leaving NAFTA…ending the Iran nuclear agreement…Rocket Man…the tax reform debate raging on. But the S&P 500 just made it a 5th positive week on some earnings optimism. So yes, it’s earnings season again, but the peak period for this earnings season is from October 23rd through November 3rd since that’s when 1,000 companies will release their quarterly results.

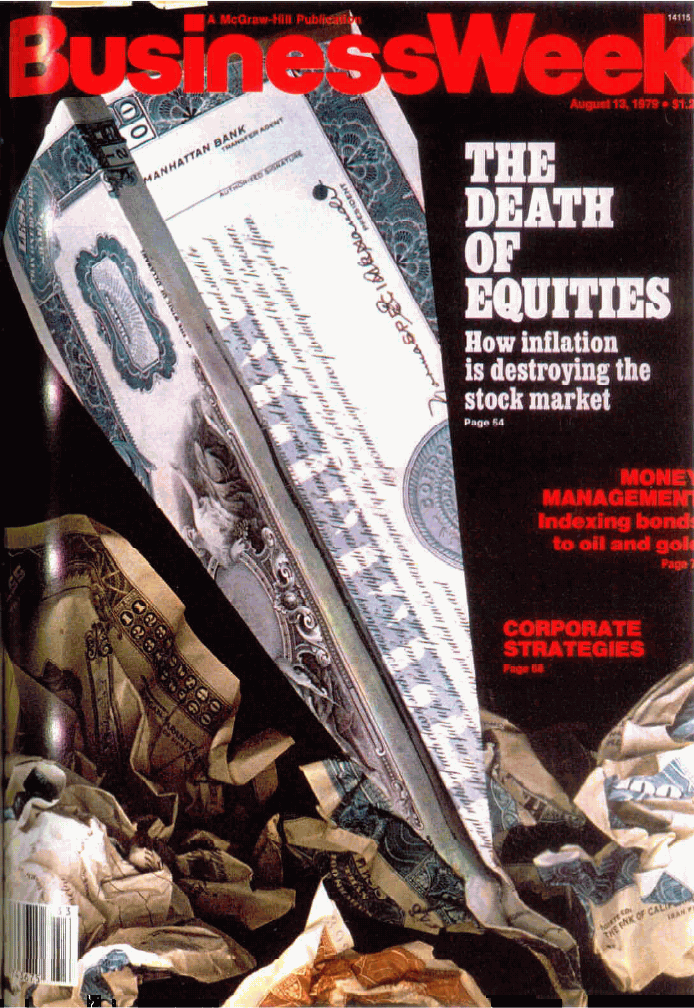

The Death of Equities.

This issue of Business Week was published on August 13th, 1979.

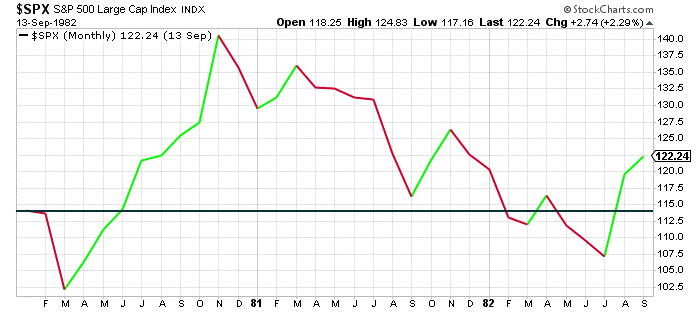

Looking at the chart below, you could have won the “I told ya so” game for the next three years…

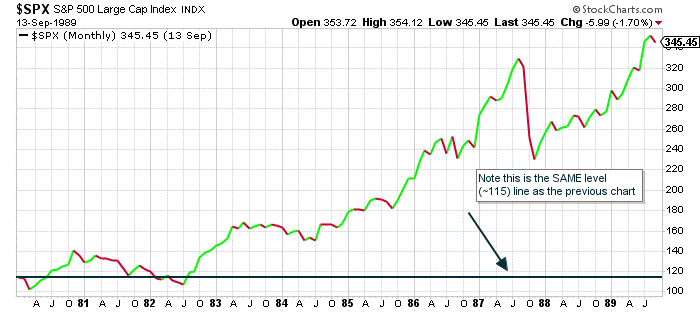

HOWEVER…if you look out 10 years, you can see that the Death of Equities was grossly wrong.

I’m going to ask you to think about this in the context of TODAY…watching the news every day and being inundated by the hyper analysis of everything all the time. Three years can be an incredibly long time day over day over day and investors need to ask themselves if any of today’s positive sentiment could erode.

Being a Monday Morning Quarterback and looking at the charts it’s easy to say, “Duh, that Business Week cover was SO WRONG.” But how much sleep do you think was lost from August of 1979 to August of 1983?

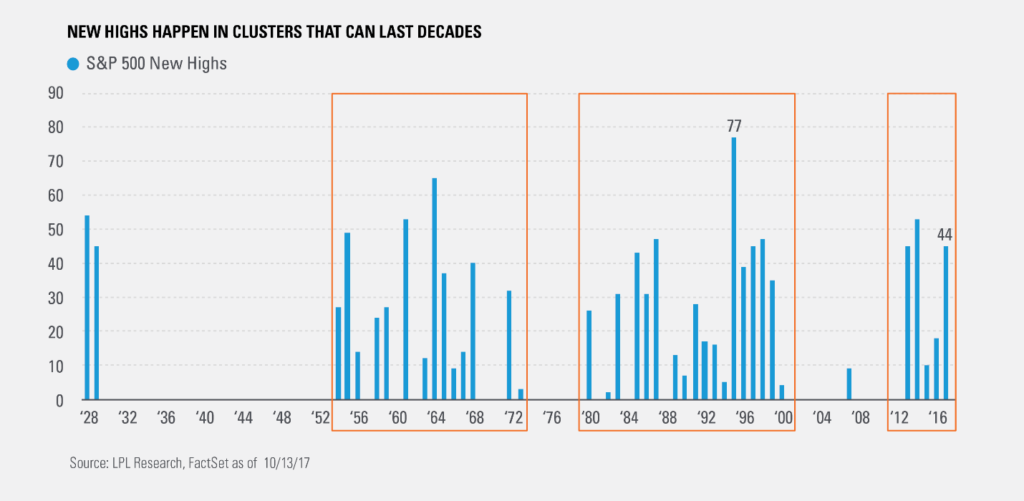

Ryan Detrick, Senior Market Strategist at LPL Financial was out with a research report last week where he stated, “It is important to remember that new highs tend to happen in clusters that can last decades, but in between you can have years without new highs. Recalling this can be one clue that this bull market may not be as old as many think.”

Here’s a chart of the S&P 500 that accompanied that statement.

By the way, the Dow and the NASDAQ charts show the same clustering, I just didn’t want to paste in two more big charts.

Here’s my point – Be the investor who looks at the 10-year chart of the S&P 500 above and says, “yeah, that’s what I focus on!”

Societal Distress

Trump has been the President for ten months. It feels like ten years…in dog years!

As I’ve written about before, I know there is a great deal of…oh how can I put this so no one gets really mad…psychological stress? Mental discomfort? Consternation? Societal distress?…over the current presidency and frankly the guy really brings most of it on himself. It’s even arguable that he’s doing it on purpose. Then there is the issue/perception of the Republican Congress not getting anything done. Regardless, be careful about it clouding your ability to see what has been accomplished and extrapolating how much can still be accomplished.

What’s been accomplished? Record highs in most major indices. That’s a big deal.

I’m coming back to TAX CUTS AGAIN. I think they will happen and frankly I think the market agrees. I’m at 75-80% conviction they happen. If I’m wrong, well, hey, I’ll eat crow down the road.

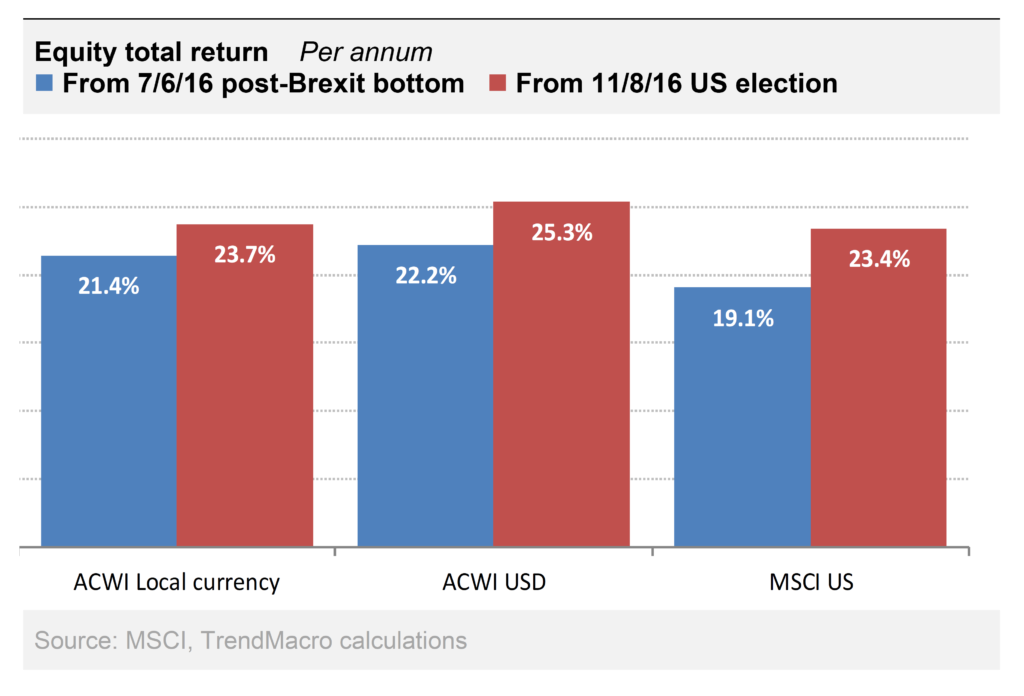

Yet I come back to the news and the consternation over the current political picture that everyone seems so focused on and maybe people are missing a bigger global picture of the market. The reality is that while U.S. stocks have lagged other world indices a little since the July, 2016 post-Brexit bottom (read: panic), U.S. stocks, post-election have performed in-line with world stocks.

See this TrendMacro chart-

Don’t focus on the point that U.S. stocks have caught up since the election…look instead at how well ALL STOCKS have done. Some people talk about the “Trump Bump” or “Trump Trade” but how does that explain how well everything is doing?

It’s because there is a lot of “Pro Growth” going on everywhere, not just in the U.S. The conditions for the markets continue to be exceptional as the growth is clearly accelerating…all without any real inflationary pressures. The Fed seems content to wait until they see inflation close in on 2% and interest rates remain unbelievably low for this stage in an economic recovery, even though the yield curve has finally started to steepen. Oh, and corporate earnings are finally increasing due to revenue growth versus cost cutting.

Don’t let the “news-tertainment” industry focused on ratings and advertising eyeballs cloud the visibility of what’s happening around you. It’s like I reminded my Mom this weekend, “There are always three sides to the story – one guy, the other guy and the truth.”

The bottom line is to stay invested and true to a long-term plan. As they say, “The Trend is Your Friend”. It’s possible that Trump’s bullying, name calling and twitter fighting will bring both the Republicans and the Democrats to the table and undertake some of the major issues confronting our country. No one seems to disagree that we need change in D.C. and 2018 mid-terms, like winter, are coming. Lots of people are on the hot seat and I’m just wondering if Trump (like him or not), and more specifically his antics (like them or not), actually become the catalysts that bring about real change.

Until then – look forward.

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.