Peace Out, 2015

As everyone knows by now, in addition to Steve Harvey totally blowing it at the Miss Universe Contest last night, the Federal Reserve ended seven years of near-zero interest rate policy by raising rates 0.25% last week. This indicates its conviction in the vigor of the U.S. economic recovery. It was a unanimous decision by the members of the Committee. The rate increase was certainly no surprise to anyone, so the market reaction to the announcement was positive – stocks rallied and Treasury yields remain mostly stable. For the week, the S&P 500 finished down -0.3% after giving back all the early and mid-week gains. The Energy sector sustained its volatility as oil prices hit new multi-year lows, finishing the week right around $34.50 per barrel. For the year, the Dow is down -3.9%, the S&P 500 is down -2.59%, while the tech heavy NASDAQ is positive +3.95 YTD on the back of Facebook, Amazon, Netflix and Google.

Fed Tightening Has Begun.

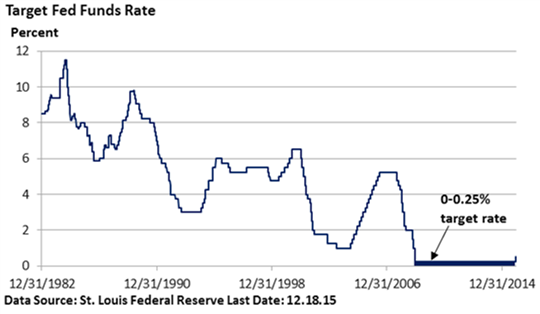

In some respects, it was the moment we were all waiting for. These were emergency rates implemented during the darkest days of the 2008 financial crisis. In reality, I think is was more of a symbolic move than a real impactful one since short-term rates remain exceptionally low. Money is still very cheap. Below is a chart of the Fed Funds going back to 1983. You can see the little blip on the very right showing the raise from last week. Relative to history, I’m comfortable with the term “symbolic.”

It’s interesting to look back at the past seven years because there were a lot of forecasts predicting that the Fed’s super-easy monetary policy would bring on dire consequences. Remember all that prognosticating that low rates and trillions of dollars in Quantitative Easing would produce hyperinflation, a collapse in the dollar, and a foreign flight out of Treasuries?

Well that never materialized.

But at the same time, the super accommodative policy did not fuel a strong economic expansion, either. It’s true the stock market has recovered from 2009 lows and more people in the U.S. are working than ever before, but this recovery has been among the weakest in the modern era.

In other words, there have been limits to what the Fed can do to promote economic growth.

Some Economic Data

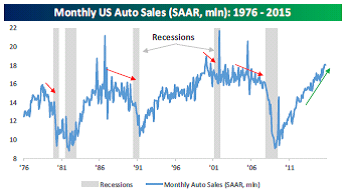

Auto sales are rocking. I write and say this all the time…housing and cars. So much of our economy is about housing and cars. Below is a Bespoke chart showing U.S. auto sales going back to 1976. Recession periods are shaded in gray. You can see auto sales usually roll over prior to the start of a recession. I don’t see anything resembling a rollover yet.

2016 Thoughts

In case you missed what I wrote last week, I’m republishing my thoughts again this week.

“You can’t swing a dead cat without hitting a Wall Street strategist talking about his or her 2016 outlook. I’ve become cynical about annual outlooks – there is nothing really magical about the change from one calendar month to another, since it does not signify any real impetus for economic change. Things just don’t change that quickly and I feel like my thoughts are always…how do I put this…rolling. So while the following are some thoughts for the next 12 months and they are coming in December, I’m not really sure they are any different than my thoughts from July.

Every year since March of 2009, investors have witnessed negative events, news stories and market shocks right alongside constant negative investor sentiment. However, somehow the economy has accelerated and equities have ranged from buoyant to outright resilient. I think the next 12 months will bring more buoyancy than outright resilience to the equity market. Concerns like a strong(er) U.S. dollar, declining oil prices, anemic manufacturing and a shift in Fed policy can exacerbate negative investor sentiment, but I believe it’s important to also focus on all the good things from above: positive consumer spending, the improving labor market, rising wages, and cheaper gas. These should offset the concerns. When the Fed starts raising rates, it will not be by a lot and will not be quarter-over-quarter, which means the Fed will remain accommodative to equity investors.

Finally, we are always on the lookout for over-borrowing, over-spending and over-confidence as a prelude to any recession. We see none at this time.

I don’t see any reason why a long-term investor would move away from the equity markets or get defensive within the equity market over the next 12 months, which is something we have been saying for a long time.”

Happy Holidays

I hope all of our clients, future clients, readers – especially those who are going to be future clients but don’t know it yet – advocates, friends, family and those who have always lent a supporting, helping and encouraging hand have a very happy holiday season. I won’t be back with another writing until next year, so I look forward to reconnecting with everyone again in 2016 when I recap some data from the 2015 calendar year and provide some more thoughts on the year ahead.

– David B. Armstrong, CFA

Important Disclosure Information for “Peace Out, 2015”

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.