Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Pain Before Gain – And I’m Not Talking About The 50 Shades Of Grey Release.

First… WOOOHOOOO! The U.S. equity markets finished higher for a second straight week. Also, the S&P 500 gained +2.1% which propelled it to a new record high. In fact, three sectors of the S&P 500 hit all-time highs: Tech, Consumer Discretionary and Materials. So basically in the face of some disappointing retail sales numbers, investors (okay, really… I mean traders, because investors have a long-term plan and portfolio) chose to focus on the positives this week. There was a general improvement in attitude as signs of a potential debt restructuring deal between Greece and the European Union started to shape up. There was also that cease fire agreement in Ukraine… but we will see how long that lasts. Finally, oil prices rose which also helped lift the equity markets. For the week, the technology sector was the #1 performing sector and utilities was the loser, as well as the only sector with a negative return on the week.

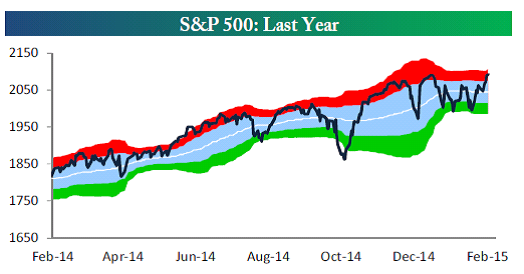

Here’s a chart from Bespoke that shows how quickly we went from oversold (the green zone) to overbought (red zone).

The Pain and the Gain

I’m talking about gas… and not the kind that would have made Mr. Grey very unhappy. I’m talking about gasoline.

Much has been made of the huge drop in gasoline prices over the last year. In reality, it’s a transfer of wealth from oil producers and related activities to consumers and the non-energy sectors of the economy. While we await the longer-term benefits of lower prices at the pump, it seems as if a day doesn’t go by that there isn’t another report of layoffs in the energy industry or a company announces it is slashing outlays on exploration.

That’s the pain.

While cutbacks won’t go unnoticed, we’re still waiting for consumers to spend their newfound windfall. Last month, retail sales fell 0.8%, as a 9.3% decline in sales at gasoline stations led the way. But gasoline prices continued to fall in January so it makes sense that we’d see lower sales from gas stations. If we subtract gasoline stations sales, which help to filter out changes in gas prices, and auto sales (which is a volatile sector), so-called “core sales” were up just 0.2% in January. That follows an unchanged reading in December.

So here’s what’s probably going on. For now, consumers are either banking their savings or paying down debt. But there is one category that has seen a surge in spending; sales at restaurants and bars are up 11.3% versus one year ago.

That’s the best level since at least 1993. I suspect it’s a precursor of better things to come. Move over chips, salsa and over-sized salty rimed margaritas… next up, durable goods orders.

Earnings Season

We follow Bespoke Investment Group for earnings research. So far, about 1,500 companies have reported their earnings and revenue for the fourth quarter (4Q) of 2014. Here’s where we stand:

• The percentage of companies beating their revenue estimates for the 4Q currently sits at 58.2%. This number is currently below the average of 60% that we’ve seen since 2001, above the 57.2% that finished up the 3Q of 2014, but below the 60.7% reading that we saw in the 2Q of 2014. Since the revenue readings bottomed out in the 4Q of 2011, quarter-over-quarter readings ping pong, but the trend has been steadily moving UP for revenues.

• The percentage of companies beating their earnings estimates stands at 62.1%. This is currently equal to the 62.1% final reading from the 3Q of 2014 and well above the 58.6% final reading from the 2Q of 2014.

Bespoke also publishes a chart that shows the spread between companies guiding future earnings higher or lower on a percentage basis. Up until the 1Q of 2014, the spread had been negative for the TEN previous quarters, meaning there are more companies stating they will earn less in the upcoming quarter than the same quarter a year prior. That’s 2.5 years of pessimism coming out of corporate America.

After two flat quarters in the 1Q and 2Q of 2014, we saw the 3Q revert back to a negative reading. As of Friday, the spread between companies posting negative guidance versus companies posting positive guidance in the 4Q stood at a whopping -9.2%! If it stays at that number, it will be the worst spread reading since the 3Q of 2008!

“Ouch” said Anastasia.

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.