Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Oil, Deflation, Earnings & the Fed – OH BOY!

Last week was a major disappointment on a lot of different fronts… sometimes you expect one thing and you end up with another. But not at the gas pumps! Oil is still a hot topic in anything you read or see on TV. The thing that has everyone all worked up is the thought that declining oil prices will cause deflation and deflation is bad. It all starts when corporations and consumers decide to wait to buy goods because they suspect they will keep getting cheaper. Prices go down on things when demand goes down and/or supply goes up. When purchases are delayed, the demand for those goods goes down and that obviously causes the supply of unsold inventory to go up. This causes a few effects:

- Spending obviously gets delayed

- It makes it hard for companies that have borrowed money to service their debt payments if they are not selling goods

- If a central bank decides to lower interest rates to stimulate an economy it won’t get people to buy goods when they are waiting for them to get even cheaper

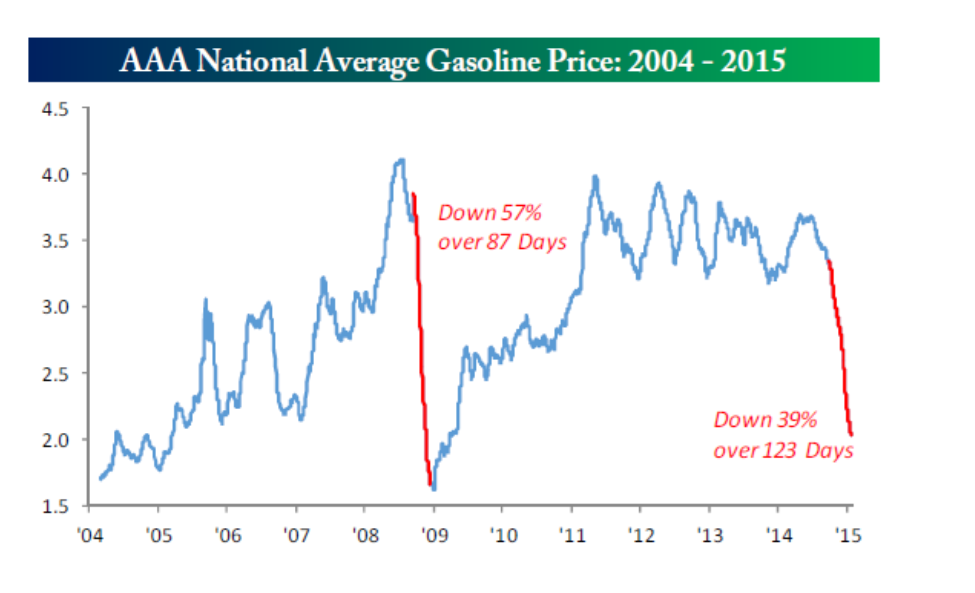

But lower oil puts more money NOW into consumers’ pockets so they can buy more and pay down their debt. This actually encourages spending… which is counter to deflation. This is a basic statement, and yeah, I know, no one is inviting me on CNBC to talk about economics. However, I’m not buying into the deflationary scare related to oil prices being so low. The chart below is from Bespoke.

The Fed

Last week’s Federal Reserve meeting was interesting. On the one hand, the Fed upgraded its assessment of the economy and labor market and left a June rate hike on the table. But the Fed also suggested that inflation could take longer to move back to its 2% annual target. And for the first time, the Fed explicitly stated that “international developments” are part of its rate-hike equation.

Here’s what that means… many other global central banks are easing monetary conditions to fight their own problems with low inflation and slow growth. The Fed, on the other hand, would like to start slowly raising interest rates. If the Fed decides to go in the opposite direction of the other central banks, there is potential to further unnerve markets.

Basically, they are gradually opening a door to allow for a possible delay in what had been an expected mid-year rate increase.

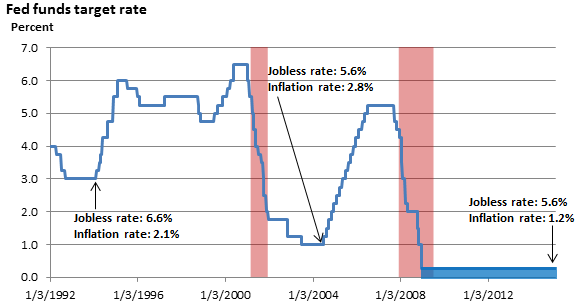

The below chart from Charles Sherry is an interesting one. Pay attention to the unemployment rate (Jobless Rate) at each point where the Fed has begun raising interest rates in the past.

Earnings

We follow Bespoke Investment Group for earnings research. So far, over 1,000 companies have reported their earnings and revenue for the fourth quarter (4Q) of 2014. Here’s where we stand:

• The percentage of companies beating their revenue estimates for the 4Q currently sits at 57% versus the reading of 60.1% from last week, and below the average of 60% that we’ve seen since 2001. As a point of reference, the 3Q of 2014 came in at 57.2% and the 2Q came in at 60.7%. Since the revenue readings bottomed out in the 4Q of 2011, quarter-over-quarter readings have ping-ponged but the trend has been steadily moving UP for revenues.

• The percentage of companies beating their earnings estimates also stands at 63.5% which is up from last week’s reading of 60%. This is slightly above the 62.1% final reading from the 3Q of 2014, and well above the 58.6% final reading from the 2Q of 2014.

Bespoke also publishes a chart that shows the spread between companies guiding future earnings higher or lower on a percentage basis. Up until the 1Q of 2014, the spread had been negative for the TEN previous quarters, meaning there are more companies stating they will earn less in the upcoming quarter than the same quarter a year prior. That’s 2.5 years of pessimism coming out of corporate America.

After two flat quarters in the 1Q and 2Q of 2014, we saw the 3Q revert back to a negative reading. As of Friday, the spread between companies posting negative guidance versus companies posting positive guidance in the 4Q stood at -8.6%! If it stays at that number it will be the worst spread reading since the 3Q of 2008!

One thing driving this is that several high-profile companies representing a broad cross-section of industries have been warning that the strong dollar is taking a toll on revenues and profits. What happens is that while a firm’s overseas sales may be growing in the local currency, they are actually smaller when converted back into stronger U.S. dollars.

The good news is that leaves a LOT of room for companies to surprise to the upside in the future. It should also be interesting that from 2011 through the current reporting season we have seen all but two quarters with negative guidance, yet we are still in a pretty strong bull market.

Go figure.

This week we will see reports from big names like Disney, Exxon Mobil, Twitter, Sony, and Merck.

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.