Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

October: A Scary Month for Investors?

Historically, October is when all the bad stuff happens: the Crash of 1929, Black Friday of 1987, and who can forget the 2008 implosion? Certainly not Dean and I who had JUST started Monument in May of 2008! I’m not aware of many other things that will test the resolve of two humans like starting a new wealth management firm in the middle of the largest financial crisis this country has seen since the Great Depression! Oh, and last year we had the October EBOLA SCARE sell-off.

Let’s get back to the market as it relates to October. If you look back over the data, September has been the worst month for stocks while October has been positive. With one week to go, October has been a nice treat for investors. That’s a Halloween reference.

Last week saw a strong finish, extending the S&P 500 winning streak to four weeks, which is the longest since last October’s recovery from the Ebola scare. Since the end of September, the S&P 500 is up an impressive 8.1% through October 23rd.

This next part is really important to read. It should convince you that there is nothing more important than:

- Having a plan from which an investment strategy is built around

- Having an investment strategy that is not subject to emotions and reactions

IMPORTANT PART

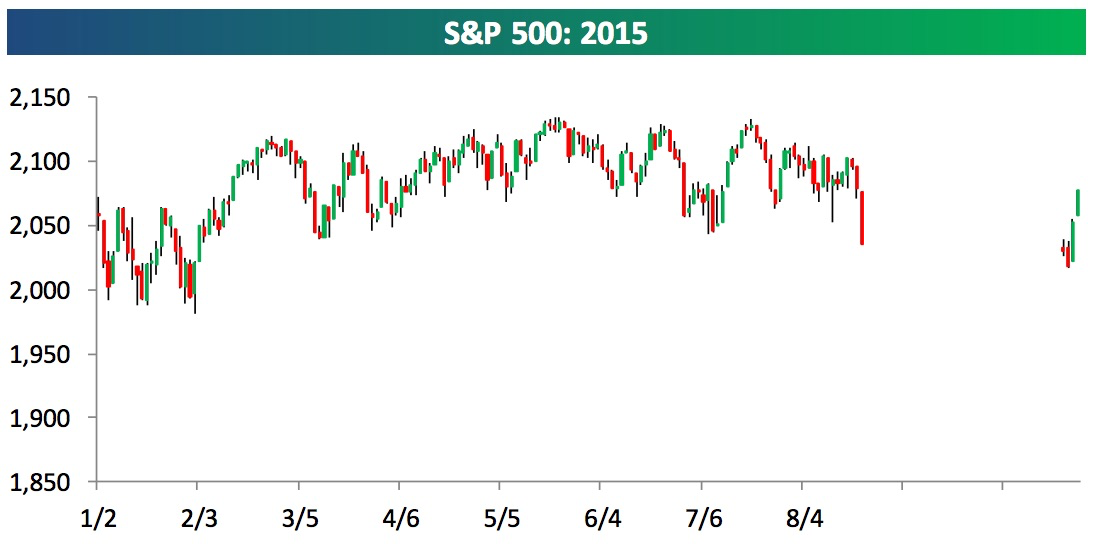

This summer has been a rough ride in the market, but if you had gone to sleep or on a vacation in mid-August (where you could not watch the market) and returned this weekend, here’s what you’d come back to… (Chart: Bespoke)

WOULD YOU HAVE CARED WHAT HAPPENED IN THE BLANK SPOT???

The answer will probably be dependent upon whether or not you needed cash during that time. If so, then hell yes you should care. If the answer is no, then you should not give two toots. These pullbacks happen, but if there is no accompanying evidence of any sort of impending financial catastrophe, don’t do anything.

So basically, since the closing low point on August 25th of 1,867.61, the S&P 500 Index has rallied 11.1% to 2,075.15 as of October 23rd. That puts the index just 2.6% below the May 21st closing high of 2,130.82.

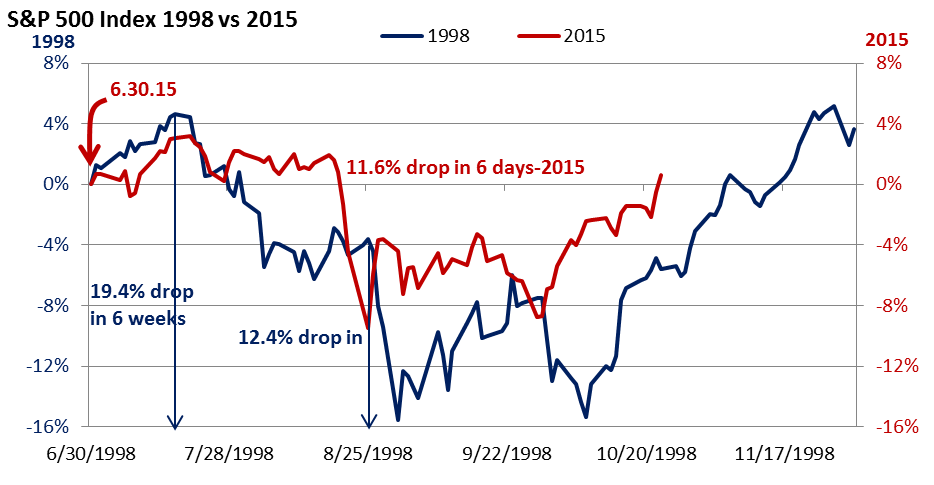

For those who are worried that we are heading towards another 2008, I think this looks a lot more like the 1997 Asian currency crisis or 1998’s Russian default and Long Term Capital Management debacle. This is because unlike 2008, it was troubles overseas that led to the recent 2015 stock market correction.

As the chart from Charles Sherry below highlights, stocks took a dive in 1998 (including a 12.4% decline in just four days) that compares to a nearly 12% sell-off over six days in August.

I understand that the troubles overseas have not gone away. But I also believe that investors don’t think a U.S. recession is imminent, which has been a tailwind for stocks.

One more thing I’d like to point out is last Thursday’s strong market gain. It was driven by European Central Bank (ECB) talk that more monetary stimulus might be on the way, and was followed up by Friday’s announcement of rate cuts by China’s central bank.

Prospects of more stimulus from global central banks, combined with growth at home, are stereotypically a recipe for a U.S. rally.

We read data on earnings from several different sources but according to Thomson Reuters, U.S. firms are once again beating low expectations on the earnings front. While Thomson Reuters continues to project that profits will dip slightly in the third quarter versus one year ago, the general trend suggests that earnings will begin to rise again for S&P 500 firms in either the fourth quarter or by early 2016.

While there are always risks as we head into the end of the year, I offer this formula:

Super easy monetary policies + Modest U.S. economic growth + Expectations U.S. corporate profits should begin to rise = Recovery in U.S. stocks

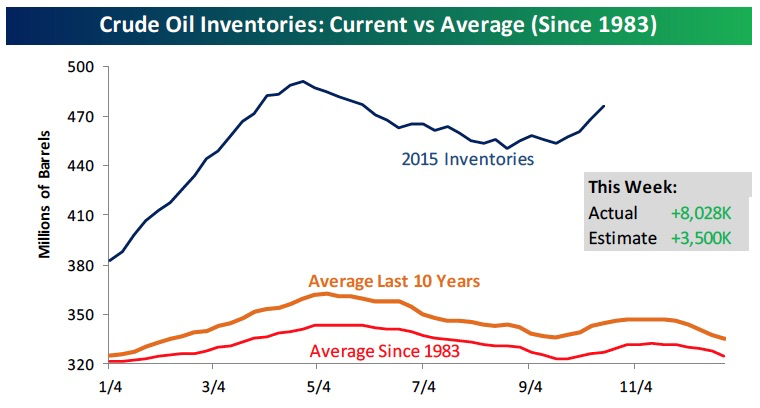

Oil

Want to know what’s up with oil? This Bespoke chart says it all. Look at the upward move in the 2015 inventories – When inventory goes up, prices tend to go down, so don’t expect a rise in oil prices in the short-term. This is a huge benefit for the consumer (remember, 70% of GDP is based on the consumer), but bad news for commodity investors and energy companies, which make up a lot of the S&P 500.

Earnings

Almost 500 companies have reported their third quarter (3Q) earnings so far and this week will be the big daddy week. Expect to see lots of news on company reports and probably some market volatility.

According to Bespoke, here’s how we look:

The percentage of companies beating their revenue estimates for the 3Q of 2015 stands at 42.8% which is currently WAY below the average of the 60% that we’ve seen since 2000. I’ll write more on this at the end of earnings season. The percentage of companies beating their earnings estimates stands at 60%, which is just below the average of 62% dating back to 1998.

Call with questions or concerns.

Important Disclosure Information for “October: A Scary Month for Investors?”

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.