Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Let’s Party Like It’s 19,999

RIP Prince, but I thought it was a fitting title for my first blog since the end of 2016. If someone had bought around 1,000 more shares of any stock in the Dow Jones Industrial Average, we would have reached the vaunted Dow 20,000.

Anyway, I took some time off for the holidays to relax and read and I hope that everyone had a great end of the year. It was a crazy one, and I’ll be out with my end of the year thoughts soon with a blog and corresponding video. Until then, here’s what’s happening…

Earnings Season is Upon Us

Ahh yes, the quarterly ritual known as earnings season is here and it unofficially begins today with our old friend Alcoa. In reality, earnings are released all throughout the year so in order to break it all up, Alcoa’s earnings announcement is the traditional start to the quarterly earnings season. This week will offer up a parade of fourth quarter and annual profit reports from the world’s largest publicly traded companies.

It can be a volatile time in the market, but as we know, longer term corporate profitability is the biggest driver of stock prices.

Read that again.

Sure, we can get daily and weekly volatility that is inspired by various incidents, both home and abroad. I allude to my disdain for the day-to-day hyping of the news by the mainstream financial media, but the reality is that it has been the problems in Europe and in China that have hampered sentiment over the recent past.

As an aside – here are some of my more favorite TV moments from the past year.

But when these one-off happenings fail to alter the U.S. outlook, the focus returns to earnings and expectations of earnings. And what happens to the bottom line is heavily influenced by the economy.

So, how are earnings shaping up for the fourth quarter?

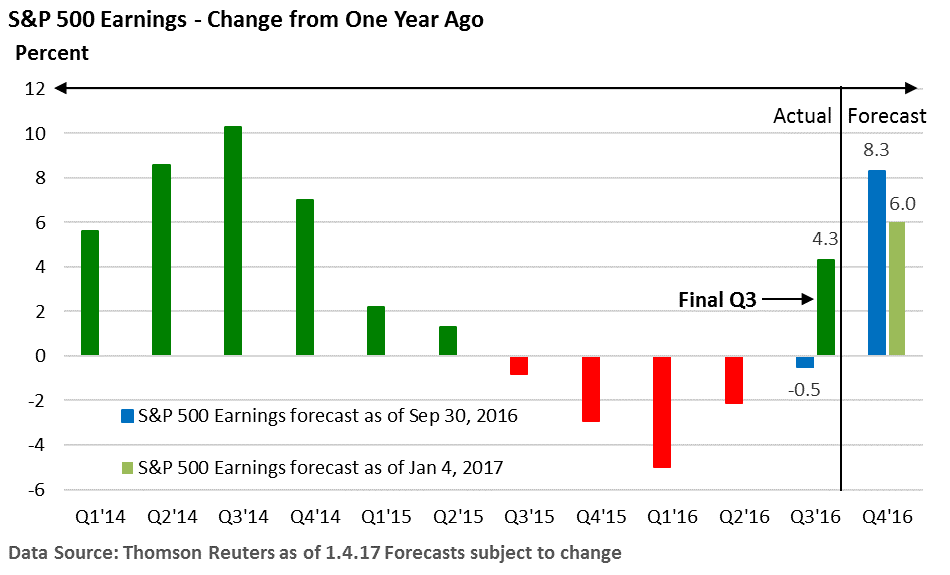

The short answer is…respectably. Especially relative to what amounted to an “earnings recession” over the past year or so. You’ll see that below represented by red bars in an upcoming chart, BUT DON’T SKIP AHEAD YET!

If we look at data going back over 100 years, the correlation between stocks and profits is over 90%. (+100% means the two variables move together perfectly, 0% means the two variables have no relationship, and -100% means they move in exactly the opposite direction.)

Take a look at the chart below from Charles Sherry. You’ll see that earnings in the fourth quarter (Q4) are forecast to rise 6.0% versus one year ago (green bar on the right). That is down from a forecast of 8.3% on September 30…which was the last day of Q3 2016.

But, as we’ve seen through much of the current economic recovery and expansion, a reduction of earnings forecasts has been quite common, as companies issue conservative guidance and analysts reduce their estimates. It’s an under-promise, over-deliver strategy for many firms…remember it’s always easier to clear the bar when it’s lying on the floor.

Now take a closer look at Q3 2016 in that chart. You will see that analysts were expecting a 0.5% drop in profits, but investors were treated to a 4.3% rise when all the numbers had been counted.

In other words, companies as a whole came in well ahead of expectations.

Want more good news? Well, diligent reader, since you didn’t skip ahead earlier, I’m coming back to tie it up on that earnings recession sentence. Just as important, the four-quarter earnings recession (caused primarily by the collapse in oil prices and the subsequent effect on profits among energy-related firms) is over, and growth is expected to accelerate in Q4.

If such growth materializes and actually exceeds current estimates, it seems likely to create momentum in the new year.

We’ll have a clearer picture in February. In the meantime, be on the lookout for my end of the year piece that we’ll be sending out soon.

Call with questions.

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.