Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Invest in Silicon Valley?

Before I delve into this week’s blog, I need to mention two things. The first is that I’m filling in for Dave while he’s travelling to South Carolina, home of his beloved Gamecocks. To learn a little more about me and my background, click this link to go to my biography.

The second is that we’ve just launched our own mobile app in the iTunes store! It’s called Monument Wealth Management News. With all of the emails we receive each day, we wanted to provide an easy way for you to read our blog posts at your convenience. Click here to download it from the iTunes store.

Back to the topic at hand. I’m not talking about investing money into the tech heavy NASDAQ index because it’s been battered down since the start of the year. I’m of course talking about investing some time to watch Silicon Valley, which is a new series on HBO about a bunch of awkward computer programmers trying to start up their own company. For anyone who has thought about becoming an entrepreneur, I recommend watching a few episodes to see what life is like at a start-up company. It’s good for a few laughs.

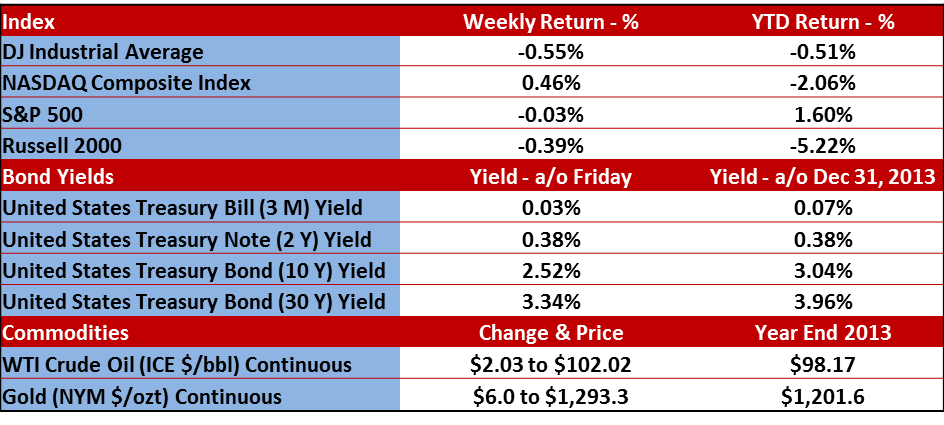

Last week was a mixed bag in terms of stock market returns, just like the week before, only this time it was the NASDAQ that was the only index that was positive. The Dow hit an all-time high on Tuesday, but then retreated a bit and finished the week lower than where it started. Here’s how everything ended up last week.

Did you notice anything special in the market summary table above?

The yield on a 10-year treasury note is now hovering above 2.5%. The last time it’s been that low was back in October of 2013 when the U.S. government shut down for two weeks. What a spectacle that was. For those of you who saw our blog posts (below) during those weeks in October and stuck to your guns, your equity portfolios were most likely rewarded throughout the remainder of the year.

- Government Shutdown – Our Quick Thoughts

- Don’t Trade in this Market – Keep Your Cool

- “How Will You Live John? Day by Day…” – Rambo II

Economic Data Update

It was a busy week for economic data, but much like the stock market, the results were about as clear as when my nine month old son tries to talk to me. On the one hand, April housing starts and jobs data came in stronger than expected, but industrial production and retail sales fell short of expectations.

Overall, no major shifts took place. Most of the items reported remain on the trend that they have been riding over the past year or longer.

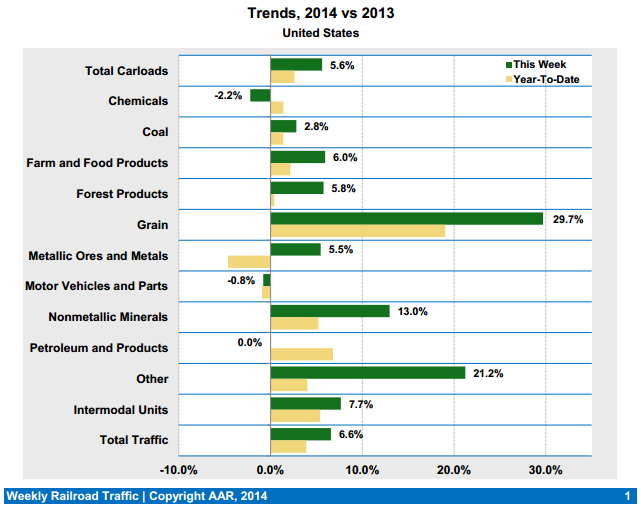

Speaking of trends, there is one area of the economy that has continued to chug along, and that would be rail traffic. Rail traffic is one of Warren Buffett’s favorite indicators of economic growth and it’s one of the many data points we track as well. The Association of American Railroads (AAR) produces a report that shows how many goods traveled across the U.S. such as coal, grain, and auto parts. At this point last year, we were only up 0.9% compared to the prior year. Looking at the very bottom bar in the graph below, you’ll see that 2014 traffic is up nearly 4.0% over last year. Based on these readings, it looks as if the economy isn’t showing any signs of losing steam quite yet.

Small-Caps – A Redux

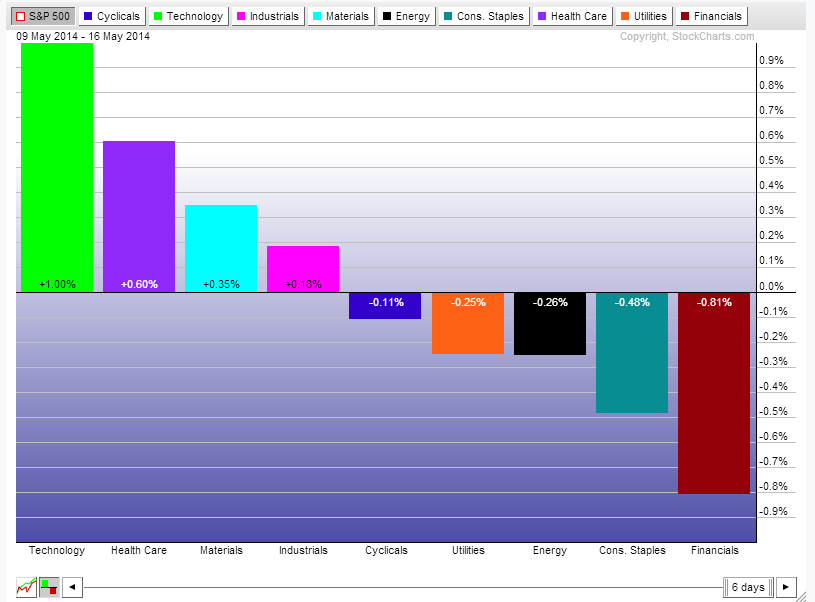

Last week, Dave discussed how small-cap stocks, as represented by the Russell 2000 Index, were getting crushed. Much like Donald Sterling and how his apology backfired, things haven’t gotten any better for small-caps either, as noted above. Everyone is concerned that small-caps will fall by 10% or more, which means that they will officially be in a correction (we don’t turn to a bear market until it reaches 20%).

I came across a statistic that was intriguing.

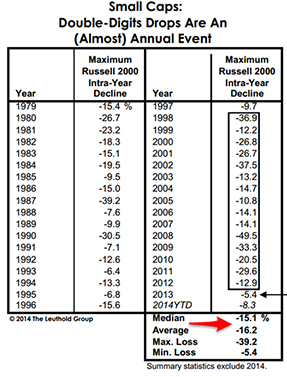

The Leuthold Group, out of Minneapolis, Minnesota, looked at the performance of small-cap stocks over the past 35 years and found that a double-digit drop from its intra-year high was actually fairly common. Based on their findings, the Russell 2000 fell by more than 10.0% in 15 straight years between 1998 and 2012.

Let me say that again. That’s 15 consecutive years where small-cap stocks experienced a correction from a technical standpoint.

Let me say that again. That’s 15 consecutive years where small-cap stocks experienced a correction from a technical standpoint.

As Dave astutely pointed out, stocks don’t move in a straight line, so if you had a strong enough stomach to sit through European debt crisis of 2010 and the U.S. credit rating downgrade of 2011, then you can weather this pullback as well.

The fundamentals of the economy haven’t deteriorated enough to justify taking any action, so bailing at this point would just be following the herd.

Earnings

Earnings season came to an end last week, and here’s where we stand according to Bespoke Investment Group earnings research.

The percentage of companies beating their earnings estimates finished at 56.7%, which is lower than last week’s reading and lower than the final reading of 61.9% from the fourth quarter of 2013. As we noted in last week’s blog post, this figure was pulled down by poor performance from smaller companies and officially represents the worst reading since the bull market began in 2009.

Bespoke also publishes a chart that shows the spread between companies guiding future earnings higher or lower on a percentage basis. Up to this quarter, the spread has been negative for the TEN previous quarters, meaning that there are more companies anticipating they will earn less in the upcoming quarter than the same quarter a year prior.

As of Friday, the spread between companies posting negative guidance versus companies posting positive guidance finally ticked up to +0.3%. That means that for the first time in the last 11 quarters, more companies have a rosier outlook for their earnings than those that are pessimistic. This should be a positive sign for the second half of the year.

Important Disclosure Information for the “Off the Wall” Blog and Market Commentary

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.