Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Hedge Funds Suck – Here’s Why

Goldman Sachs puts out some pretty interesting information on hedge funds. In their most recent report published in February, they analyzed 788 different hedge funds which account for $2.6 trillion of gross equity positions. That is a fancy way of saying those hedge funds manage $1.7 trillion and $873 billion of short positions.

Using something called 13F filings, Goldman breaks down their observations and gives some insight into what is happening.

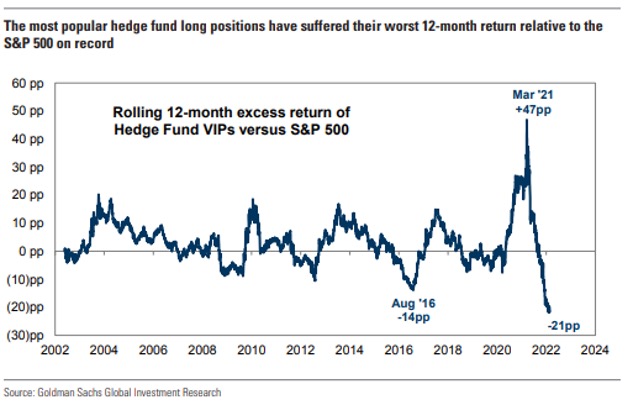

First, let’s take a look at hedge fund and S&P 500 performance. While the S&P 500 has logged the worst start to any calendar year since 2009 (down 9%), the basket of the most popular hedge fund positions held (as tracked by Goldman through those 13F filings) is down 12%.

Looking back at the trailing 12 months, The S&P 500 has a positive 14% return while their basket of hedge funds is down 7%. That is a 21 percentage point difference in performance.

That is also known around finance people as something we call, “massive”. Chart below.

I’m not a fan of hedge funds…and I’m even less of a fan of the fans of hedge funds.

Why?

Here’s one reason:

The top five stocks held by these hedge funds are – MSFT, AMZN, GOOGL, FB, and AAPL.

The top five stocks of the S&P 500, by descending percentage weighting, are AAPL, MSFT, AMZN, TSLA, GOOGL.

So generally, the hedge fund investors pay 2% a year in management fees, 20% of any profits above some high water mark (for example, any profits above the first 8% of gains), and have very, very limited liquidity.

And you get negative 21 percentage points of UNDER PERFORMANCE…But hey, it’s impossible to attach a price to slinging around that you are invested in a hedge fund at a cocktail party.

Someone: “Oh, you do wealth management…I’m an investor in a hedge fund that’s super exclusive and specilizes in…”

Me: “Oh, look! There’s my Aunt Jenny’s cat groomer from back when I was in third grade. I’m gonna go say hi. Excuse me, I’ll be right back.”

By the way, I always disliked Aunt Jenny’s cat groomer… She smelled funny…but hey.

For those who say, “Yeah, but what about that part of the chart where the outperformance was up 47 percentage points (pp)???” Ahh, yes, good observation.

It’s the tumble from +47pp to -21pp that has me shaking my head. I mean, be better than a 77pp swing from +47pp to -21pp…especially for those ridiculous fees.

I’ll sign off with this opinion: No one needs these BS hedge funds unless you are so boring that you think you need that sort of weight to be interesting at a party.

In that case, you’ll find me with Aunt Jenny’s cat groomer.

Be sure to check out our most recent episode of Off The Wall Podcast where Jessica and I interview Michelle Diamond and Heather Savage with Cumberland Trust, and learn more about why people should consider naming a corporate trustee when they establish their family trusts – really interesting info that I never knew before the interview. Check it out.

Keep looking forward.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

Recent Posts

By David B. Armstrong, CFA

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.