Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Greece Schmeesh – I’m Moving On.

I mean, its SEC Media day for crying out loud! Who wants to talk about Greece anymore? I applaud Spencer Rand, CFA here at Monument with making that the first thing he pointed out when I saw him this morning, followed quickly with, “…and South Carolina is tomorrow.” I expected a greeting along the lines of “futures are up of 1% this morning on the Greece news.” Grasshopper. Okay, I’m taking some artistic license with the still celebrated talent of Salt-n-Pepa, so let’s talk about China, baby.

China’s stock market got ugly last week, which created some anxiety in U.S. markets toward the middle of the week.

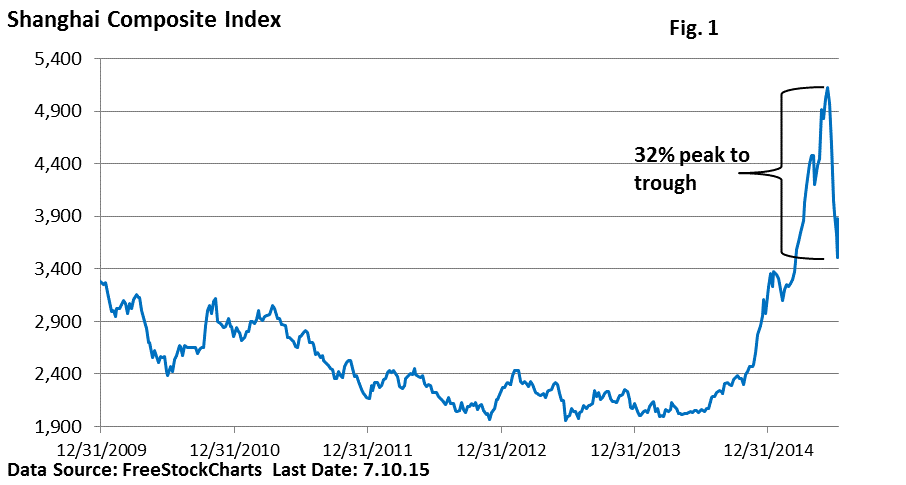

First, here’s some historical context on China. China’s fast-growing economy has slowed in recent years, and government officials felt that encouraging individuals to buy stocks would be one way to help China shift from an investment-led economy to a more consumer-driven economy. With the encouragement of government officials, the small retail investor jumped in, creating a bull market rally that sent shares into outer space. You can see from the chart below, the Shanghai Composite Index rocketed 152% from June 30th, 2014 to its June 12th, 2015 peak … I’ll get to the subsequent decline of 32% from that high a little later.

As an aside, this all occurred at the same time China’s economic growth was slowing. Anyway, in addition to this throng of new investors, heavy margin purchases contribute more fuel to the fire. Take a look at Figure 2.

Are you saying to yourself, “sounds a lot like the U.S. markets in 1999…”?

Yeah.

The reality as it relates to the U.S., (translation: why you should care), is that China is the world’s second-largest economy and has also been one of the key drivers of global growth over the past ten years or so. Investors are troubled that a collapse in China’s stock market could further dampen the Chinese economy, (which has already been slowing rather than growing), and potentially create a financial crisis in its already shaky banking system.

Putting it all in perspective, the U.S. exported $123 billion in goods to China last year and while that sounds like a lot, you have to remember our economy runs at around $17 trillion. According to something I read on Business Insider this weekend, there are only a few high-profile firms that depend significantly on sales to China and overall revenues from S&P 500 companies amount to just 2%.

Worries about the stability of the Chinese financial system and global repercussions are the bigger concern for right now. Basically, the Chinese government stepped in and intervened to stop the sell-off. I read speculation that Chinese stock brokers stopped taking sell orders. I guess that’s one way to stop a sell-off.

I’m not sure anyone other than a qualified trader, (you are most definitely, certainly, positively, probably not one), should be messing around with playing any China trade. In the blink of an eye last week, the index reversed positive over +10%. Traders who called that and got it right are geniuses … all two of them. They will follow that up with three consecutive wrong calls this week. Trust me.

Where We Stand

• I still don’t think this Greece thing is going to spread or become a big deal for anyone other than a person standing in line for dough at a Greek ATM.

• China could actually become a big deal but only if the financial system implodes. I don’t see any warning signs that something like that is actually on the horizon.

• Oil is lower … again

• Earnings season has kicked off. I’ll get into that next week. While the first four months of the year have been ho-hum, the economic picture is improving. Construction, housing, consumer spending and employment are all doing better. I’ll bet earnings accelerate in the second half relative to the downtrend we’ve seen since the end of 2014. My bet is on analysts’ revisions lower are too low and we will see some surprises to the upside as the reporting season progresses.

Call with questions

Important Disclosure Information for “Greece Schmeesh – I’m Moving On.”

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.