Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

GDP was a DOG

According to the just-released first round of data on the first quarter’s (Q1) Gross Domestic Product (GDP), which is considered the gold standard for the measurement of goods and services, 2017 has pretty much sucked.

It looks like GDP growth slowed from Q4 2016’s annualized pace of 2.1% to 0.7% in Q1.

Remember, that’s the first announcement of preliminary data…but still. Poopy pants.

A quick summary is that there was a significant increase in spending by businesses, BUT, that was more than offset by a sharp slowdown in consumer spending. In fact, the 0.3% annualized rise in consumer spending was the slowest since 2009.

We can pick the report apart, but as I have written about in previous years (for example, see “A Review of First Quarter GDP” and “Are Things Getting Better While The Market Sells Off?“), there is evidence that there are peculiarities in the models that seasonally adjust each quarter’s data. This has resulted in significant underperformance in Q1 going back over 25 years.

That means we should expect a Q2 bounce.

But still…it was a lackluster report.

Let’s check out more of a bigger picture. The chart below highlights annual changes in GDP going back to 1930.

Here’s what you should notice – ever since the 2008 recession ended, we have not had one year when annualized growth has exceeded 3%. That has not happened going all the way back to the 1930s.

However, the major stock market indexes are near or at record highs.

My opinion? This is ALL about corporate profits and low interest rates, which offer less competition for stocks. Mom – this means that interest rates at banks, and for CDs and even bonds are SO LOW that you figure, “What the heck, I may as well be in the market where I’ll get some possible growth and some dividends.”

Companies have done a good job managing their bottom lines, and Q1 is no exception. Revenue is growing too. More on that below.

Despite the weak GDP report, many of the larger industrials, which do a significant portion of their business overseas, have raised full-year forecasts…which also suggests the global economy is accelerating. More on that below, too.

Anticipation of faster growth is driving the equity markets higher. That’s what’s happening.

Earnings

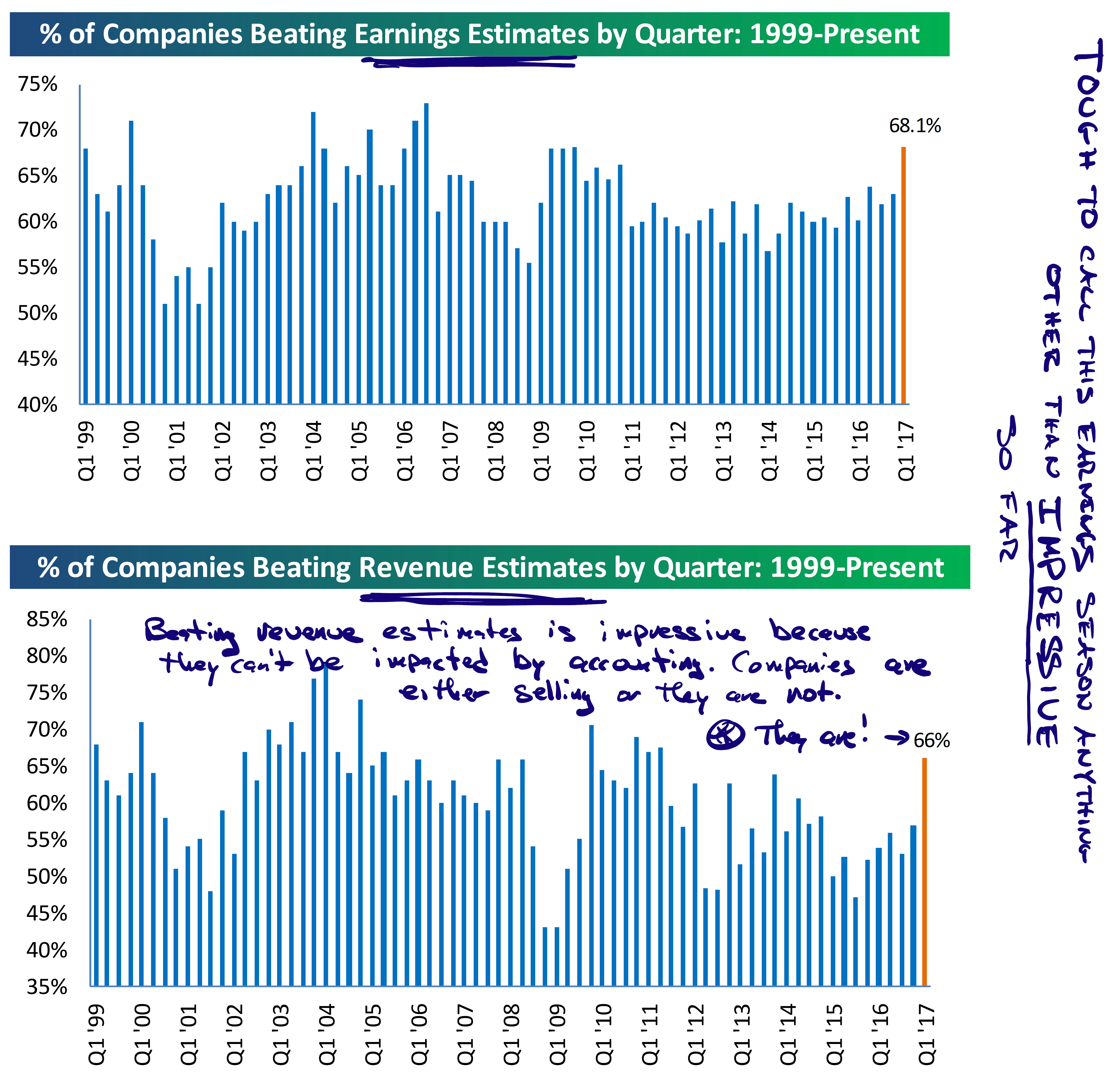

As it stands, Q1 earnings look strong, even as GDP was not. Let’s see how things go when the major retailers report over the next couple of weeks. See these charts from Bespoke and my scribbled thoughts.

All I can say is…IMPRESSIVE.

Some Random Thoughts

I’ve been collecting some charts and scribbling…I’ll let the charts do most of the talking this week.

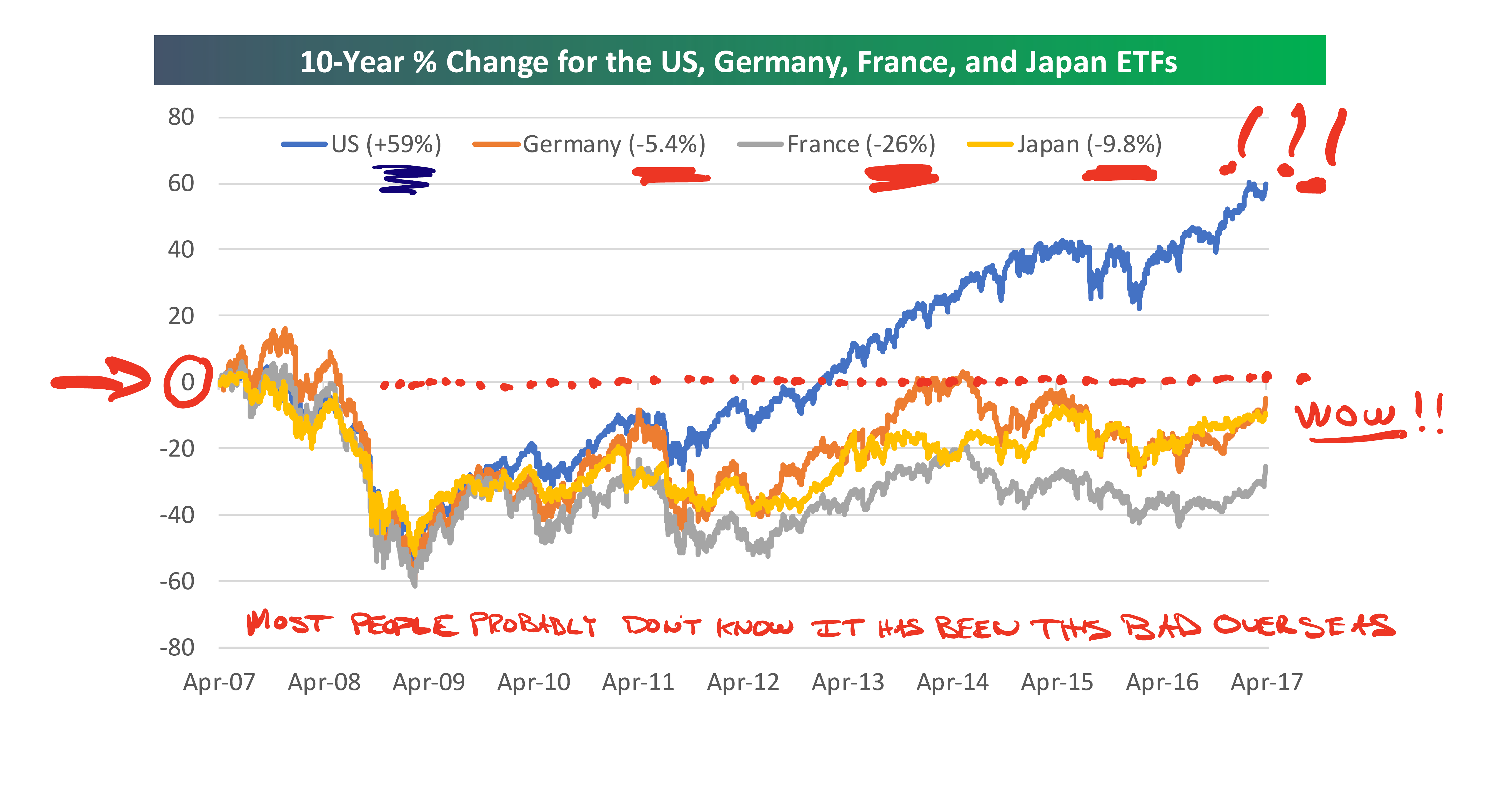

It’s nice to see France and others ticking up lately…I don’t think many people know how poorly the markets have been doing for 10 years. From Bespoke:

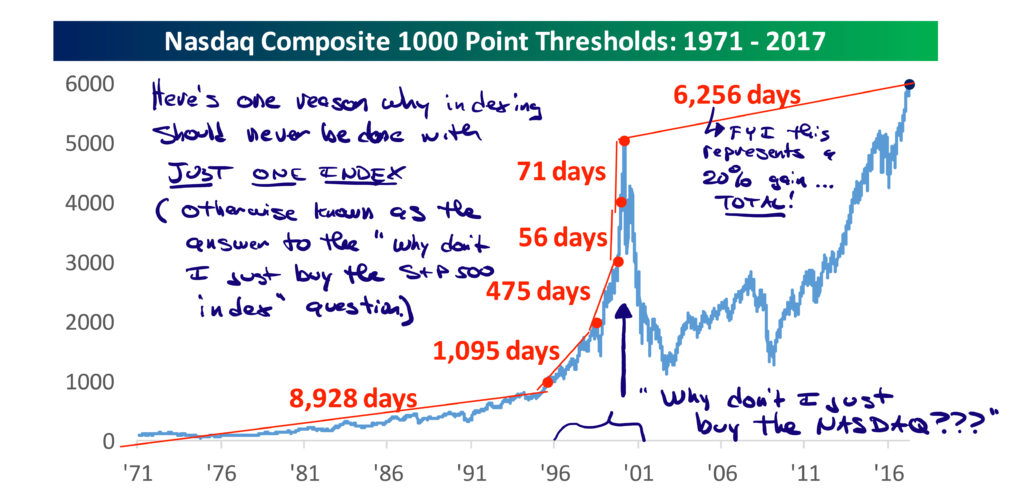

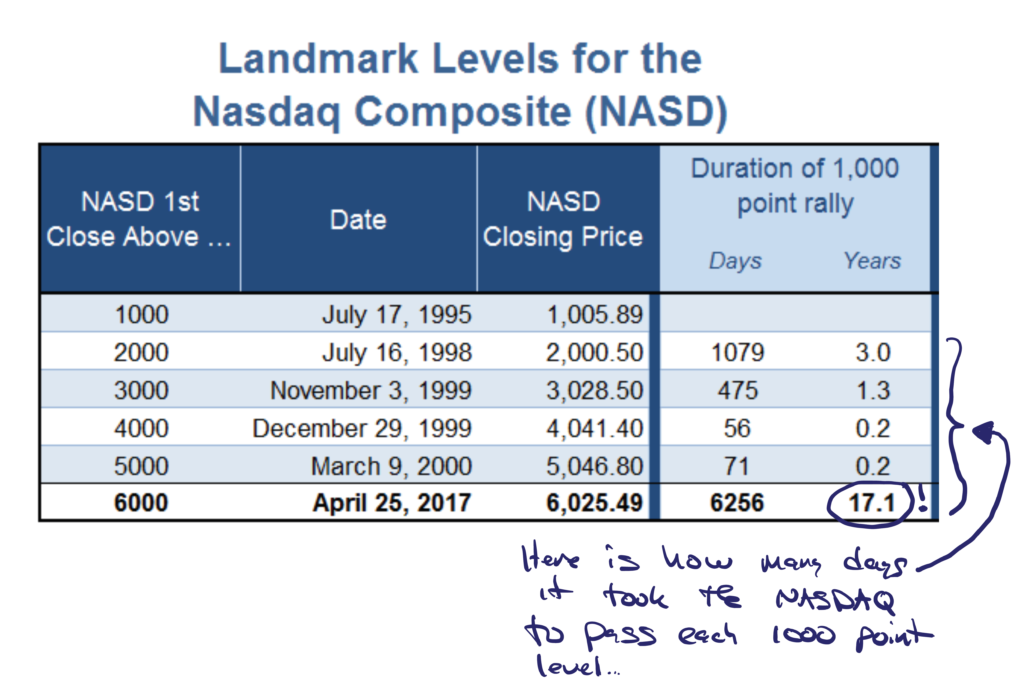

From the Department of Indexing, I captured this gem, below. It took the NASDAQ 6,256 days to print a 20% return. Yet I remember getting started in the business and people saying “I can beat most managers by just buying the QQQs!” (Mom – that’s the ETF that tracks the NASDAQ.) Man, who DIDN’T love 1999. Maybe the shorts…anyway, this chart is from Bespoke (they have some great charts, I can’t help myself).

From the Department of Indexing, I captured this gem, below. It took the NASDAQ 6,256 days to print a 20% return. Yet I remember getting started in the business and people saying “I can beat most managers by just buying the QQQs!” (Mom – that’s the ETF that tracks the NASDAQ.) Man, who DIDN’T love 1999. Maybe the shorts…anyway, this chart is from Bespoke (they have some great charts, I can’t help myself).

This chart below is from Dorsey Wright. (Sorry for the chicken scratch typo… I circled the years but look to the left for the days, specifically the 6,256 days.)

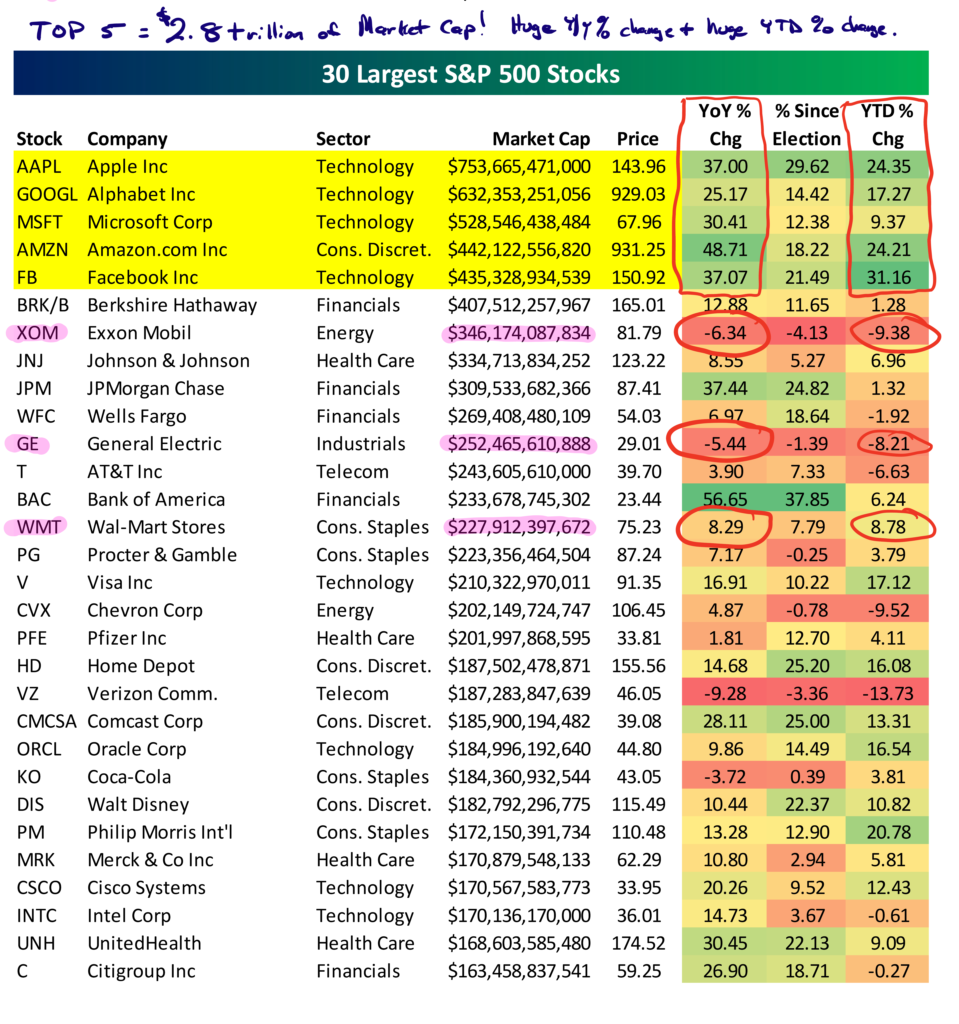

Speaking of the good old days…anyone remember when Exxon, GE and Walmart were the big market cap names in the S&P 500? Yeah…They aren’t anymore. Another one from Bespoke below.

Final Thought

I’m constantly hearing reasons why the bull market’s end is near…I can remember them all the way back to 2012. But the amazing thing is that this market has been able to shrug it all off for years.

Looking back, the biggest event during the first quarter was Trump taking over as President. Investors were hopeful that tax reform might be on the way and there was also hope that the repeal and replace of Obamacare would be a huge plus for U.S. stocks.

I can feel this raising the hackles of some readers – I get it. BUT, that’s what the market rally points to…there is a lot of hope.

However, then there was the failure to do anything meaningful with healthcare.

This is a very stark reminder that politicians love to say things and then get nothing done.

It is what it is and I don’t see any change on the horizon on that issue.

Here’s what I do know…it is very dangerous to mix your political views with your investment strategy. I remember many clients and friends convinced the world was going to stop spinning on its own axis because of one of Obama’s policies or another.

Eight years later, I’m hearing the same thing about Trump now…just from a different set of people.

The bottom line is that the market did extremely well under Obama and his policies. GDP and the economy…ehhh not so much, but you look at the score board and no one can argue that the market did well for the eight years under Obama.

I’m just sayin’.

Time will tell whether or not it will for Trump.

The point I want to make is that keeping your politics out of investing will help you see things much more objectively. Politics is a blood sport in this country which makes me very sad inside, but what makes me very happy is that I know of a lot of people that saw past politics and for the past eight years did well with their financial planning and their investment discipline and strategy.

Don’t turn investing into a blood sport.

Please call with questions.

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.