Explore Our

“Off The Wall” Blog

Read our Private Wealth Advisory team’s unique thoughts on the markets and investing.

Fresh Snow and a Fresh New High

OF COURSE WE ARE OPEN TODAY!

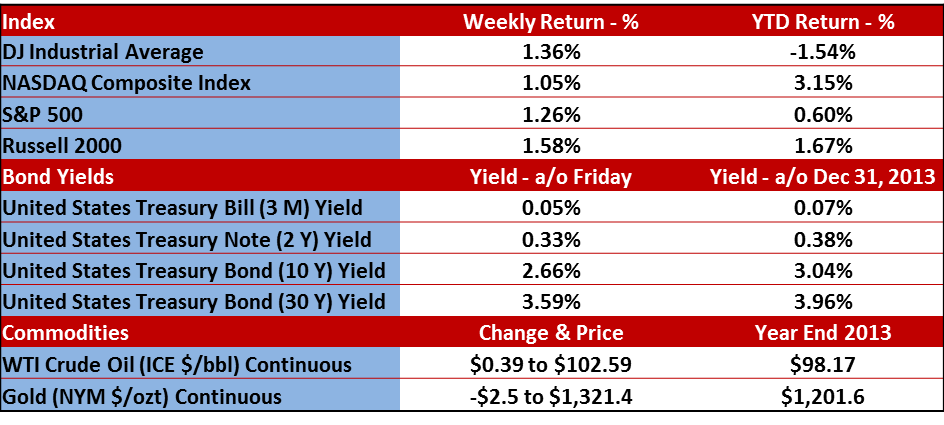

Anyway, it all happened in the blink of an eye… after a 5.8% decline that took the S&P 500 to a low for the year of 1,741.89 on February 3rd, the index rallied to a closing high on February 27th and took the action on through to the final day of last week (and the month) to finish at 1859.*

Much like snow in Washington D.C., the party in the equity markets just does not seem to stop.

Friday marked an all-time high for the S&P 500 and for the month of February we saw a return of about 4.5% bringing it to a positive year-to-date return. The Dow Jones Industrial Average is still about 1.5% away from another all-time high.*

Oh, and a close over 1850 took us above some all-important blah blah blah technical level that some bobble heads on TV were talking about. Just in time to celebrate – wait for it – the five year anniversary of the March 9th 2009 low of about 676 on the S&P 500.

676 to 1859 on the S&P 500… it seems like just yesterday people were LITERALLY calling and saying to me “seriously – this thing could go to zero…” When you factor in dividends, that’s damn near a triple.

Speaking of triples, I’d be remiss if I did not mention the complete SWEEP of Clemson University by my beloved University of South Carolina Gamecocks baseball team this past weekend. Oh the STING of being within ONE PITCH of the winning out in the final game of the series… only to lose by three runs.

We are currently at 1,817 days in this S&P 500 bull market, which is the 7th longest since 1928.

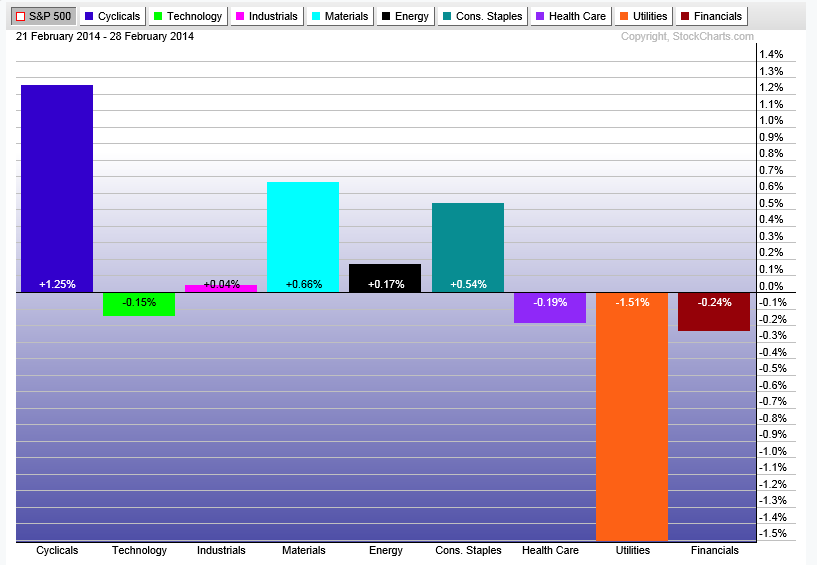

Our favorite sectors for the past five years pretty much remain unchanged. Since the beginning of 2009, we have liked the Tech, Consumer Discretionary (CD) and Industrial sectors, which are reflected in the ETF portfolio we manage. We added Health Care to that list last summer. During the little up and down blip that started around the middle of January through the end of last week, only the Industrial sector had a negative return (around -1.3%) while the Tech was up almost +.90%, CD up +1.1% and Health Care up 4.1%… all rounded of course. Since I’m measuring it as a blip, this basically means the S&P was flat during that time. (My definition of “blip”: the S&P 500 goes down and then comes back to break even at zero. Blip is not a technical term.)

Please call or email with questions.

Interestingly and not well chronicled here, the emerging markets have been making up a lot of lost ground since late January alongside the small-cap indices. We are keeping our eye on them especially since alongside Tech, CD, Industrials and Health Care, we have been big fans of small-cap and mid-cap indices since late 2008.

Ukraine is the last thing I’ll mention before I’m off to prep my shovel, broom and sand/salt mix. It’s a horrible situation from a humanitarian perspective but they simply are not a player in the global economy. There may be some volatility but it will only cause an economic problem if there is an escalation.

Oh, and what’s the broom for you ask? Snow on the car of course… and to celebrate the SWEEP by the Gamecocks! Ok, I’ll stop – no one probably reads this far anyway.

*Data and charts from Yahoo Finance, FactSet and Barron’s.

*Data and charts from Yahoo Finance, FactSet and Barron’s.

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the Monument Wealth Management current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA®

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.