Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Eject, Eject, Eject?

Last week I wrote a blog titled “What Goes Down Will Come Up – Over Time”. Looks like it was a week too early but you should read it anyway because, well, damn it I took the time to write it so that’s why.

Don’t get all freaked out about last week. I know everyone wants the trees to keep growing to the sky, but pull backs like this happen. They have to.

Last week the Dow Jones Industrial Average (DJIA) fell over 467 points which equates to about 2.75% while the Standard & Poor’s (S&P) 500 fell a little over 53 points which is right about 2.69%. That means the S&P 500 is now about 3.15% off from the high set earlier this year. And when you look into the other sectors of the markets, you can see that everything was down last week and nothing was spared…it was red across the board.

Oh, wait except volatility…which was up. The Chicago Board of Options Exchange Volatility Index jumped over 34% last week according to Dow Jones.

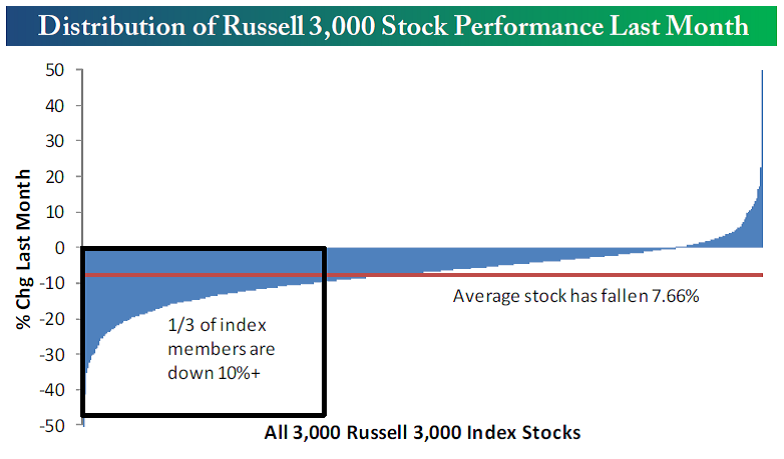

So we are currently looking at the Dow sitting slightly negative for the year, the S&P 500 up around 4% and the Russell 2000 down almost 4%. So 2014 is looking pretty flat right now for investors spread across the three most popular indices. The Russell 3000 index is comprised of 99% of all the stocks in the U.S. The chart below from Bespoke (what would my weekly blog be without a hat tip to them) shows that 33% of all stocks in the Russell 3000 are down 10% or more over the past month.

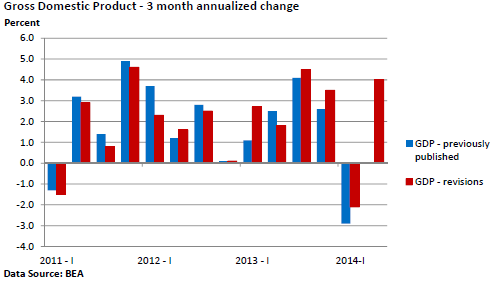

GDP in the second quarter of 2014 expanded at an annualized pace of 4.0% following a -2.1% decline in the first quarter…revised up from -2.9%.

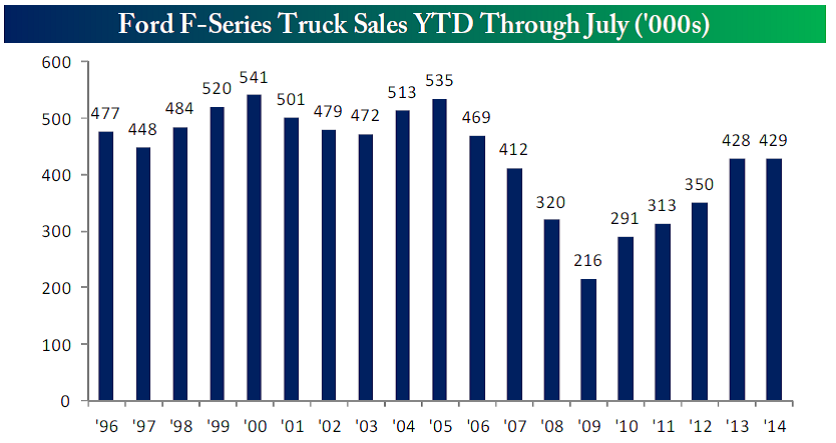

Ford F150 Truck sales are up YTD through July. This is good – only a small percentage of people buy F150’s to just cruise around in for looks and Beast Mode Cowboy antics. The rest use them as actual functioning work vehicles to haul pipes, lumber, tools, compressors, dirt and other building stuff…not golf clubs or Tumi luggage. So it’s a good economic indicator.

(Bespoke)

Employment

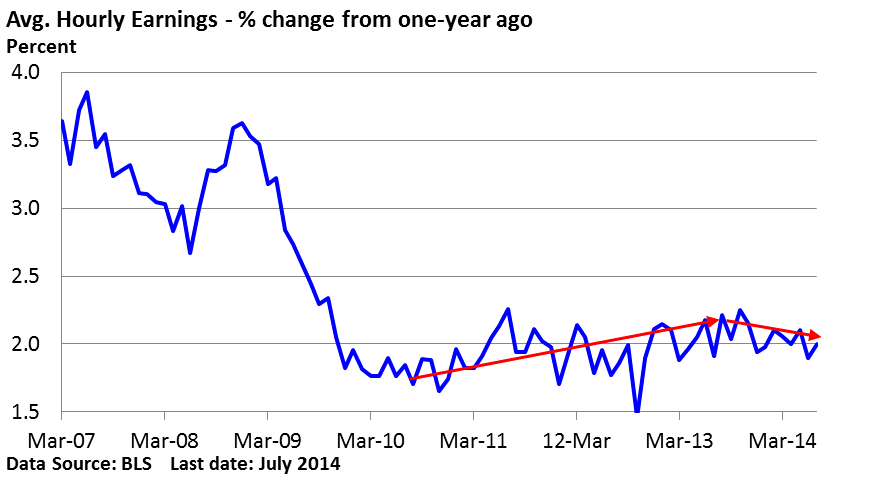

Last Friday, the Bureau of Labor Statistics reported that nonfarm payrolls grew by 209,000 in July, the sixth-consecutive increase north of 200,000. That hasn’t happened since 1997. The report included in the release what is called “average hourly earnings” and it was unchanged in July and is up a poopy 2.0% versus one year ago.

Here’s a chart of the poopy-ness and it indicates wage growth has been weak and the rate is showing no signs of accelerating. If that’s the case, it means that there is still plenty of slack in the labor force, and the Fed can be patient with its low-rate policy.

BUT….

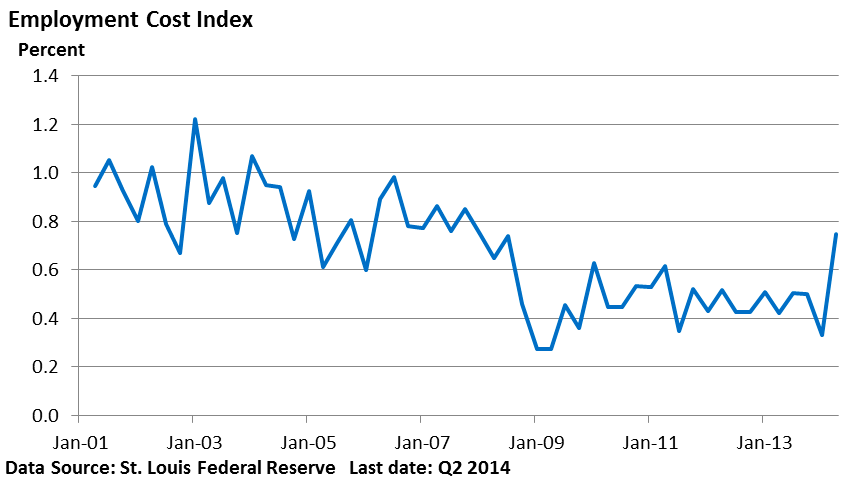

On the other hand, a more comprehensive gauge of labor costs released last Thursday may be suggesting otherwise. The Employment Cost Index, which takes into account benefits, jumped 0.7% in the second quarter, its biggest one-quarter rise since 2008 – see below.

In theory, a large supply of labor would likely give employers leverage over current and potential employees. It’s all about supply and demand – if the supply of labor exceeds demand, then businesses don’t have to offer much in the way of wage concessions. But if the available pool of labor is shrinking, then we should see upward pressure on wages and benefits. This then plays into inflation fears.

Earnings

We follow Bespoke Investment Group for earnings research. So far 1,492 companies have reported their earnings and revenue for the second quarter (2Q) of 2014 with 800 of them reporting just last week.

Here’s where we stand:

- The percentage of companies beating their revenue estimates for the 2Q currently sits at 61.3%. This number is nicely above the average of 60% we’ve seen since 2001 and above the 56.0% that finished up the 1Q of 2014. Of course, the earnings reports are not close to being complete but that sure would be a big move down from the current reading of 62.3% to the 56% final reading we saw in the 1Q.

- The percentage of companies beating their earnings estimates stands at 61.4%, which is well above the 56.7% final reading from the 1Q 2014 quarter.

Important Disclosure Information

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.