Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Earnings – You’ll Love this Post

The market highs have been front and center in the news and the President’s twitter feed, with the S&P 500 Index racking up eleven closing records in the month of October. The index has finished higher for eight straight weeks.

That’s pretty impressive.

It was also notable to see the Nasdaq 100 (QQQ) lead the way higher this week versus the S&P 500 and Dow Jones Industrial Average, since it just crossed above the +30% mark on a year-to-date (YTD) basis. The next closest index YTD is the Dow, which is up 21%. The mid-cap and small-cap have been weak (they were losers on the week), which is somewhat of a bummer for the overall health of the rally.

What’s going on?

It’s a combination of factors supporting gains in stocks that remains in place. We’ve seen some decent economic growth here at home combined with an acceleration in growth around the world, which has created a strong lift for corporate profits. If you read this blog with any regularity, you know that I believe corporate profits are a key driver of stocks over the medium and longer-term.

Earnings are important and they are doing well, but let’s not discount a few other things:

- Historically Low Interest Rates – While it creates challenges for those who depend on yields for income, it creates less competition for stocks.

- Tax Reform – At this point, it’s not whether it will be accomplished, but what we will actually get. I’ll let the other sources of news provide all the details on what the House has proposed so not to bore you here. The two important things to know are that “markups” (where the committees debate, amend and essentially rewrite the legislation) are taking place in the House this week. The Senate version will probably be out on Friday, according to Ryan Ellis who held a tax plan overview conference call for the U.S Chamber of Commerce this morning. It is clear that the Republicans want to motivate businesses to spend on plant and equipment by allowing for immediate expensing rather than over the life of the assets. They also want to encourage hiring employees to fill new needed positions. Lowering corporate taxes and reducing regulation are meant to incentivize U.S. and foreign companies to build incremental capacity in the U.S. This reform goes hand-in-hand with Trump’s trade policy, which has already led to many foreign companies announcing new plants in the U.S.

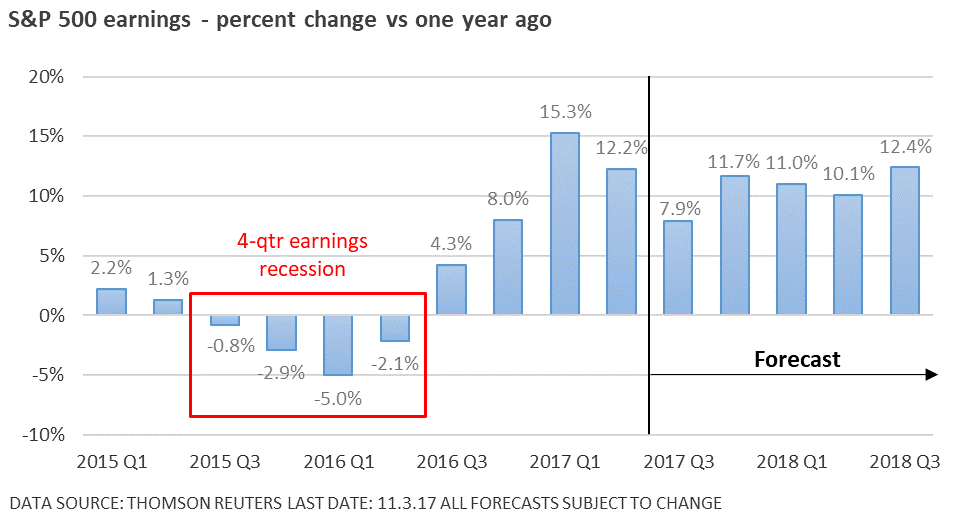

Let’s take a look at earnings growth. There are a lot of different ways to report earnings, but today I’m going to look at data from Thomson Reuters. According to them, 81% of S&P 500 companies having reported quarter three (Q3) results. So far, S&P 500 profits are projected to rise 7.9% (basically calculated by taking those who have reported + forecasts for the remaining 19%).

You can see this in the graph below.

As it stands, earnings appear set to snap a two-quarter streak of double-digit profit growth. However, profits have come in much better than expected. As late as October 23rd, Thomson Reuters had projected a more modest 3.8% rise…. Once again, analysts have done a poor job of estimating the tailwind firms would receive from a sustained, synchronized uptick in the U.S. and global economy.

Looking ahead, earnings growth is expected to return to double digits. However, a note of caution is in order. It’s not easy forecasting earnings more than one quarter out since there are just too many variables that impact the profit equation.

A promising outlook also leaves less room for disappointment – the opposite of “the bar is easy to clear when it’s sitting on the ground”. Still, upbeat forecasts are a sign of confidence in the U.S. and global economy, and we’re seeing that reflected in the latest string of new highs.

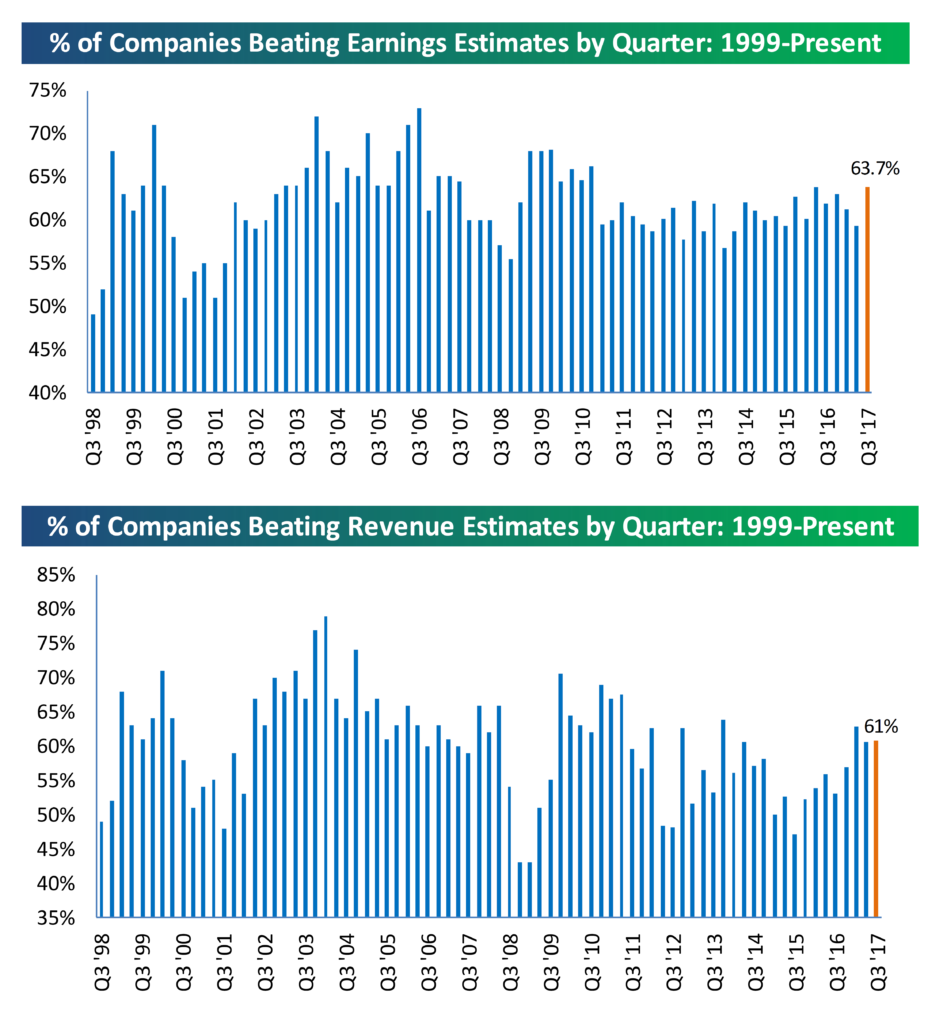

Here’s what should be familiar charts for anyone who regularly reads this blog during earnings season (Bespoke):

The percent of companies beating earnings is impressive at 63.7% if it can stay there. The percent of companies beating revenue estimates is in line with where it was last quarter, which is okay, but if you look back over the quarters to Q3 2015, it’s a nice upward slope.

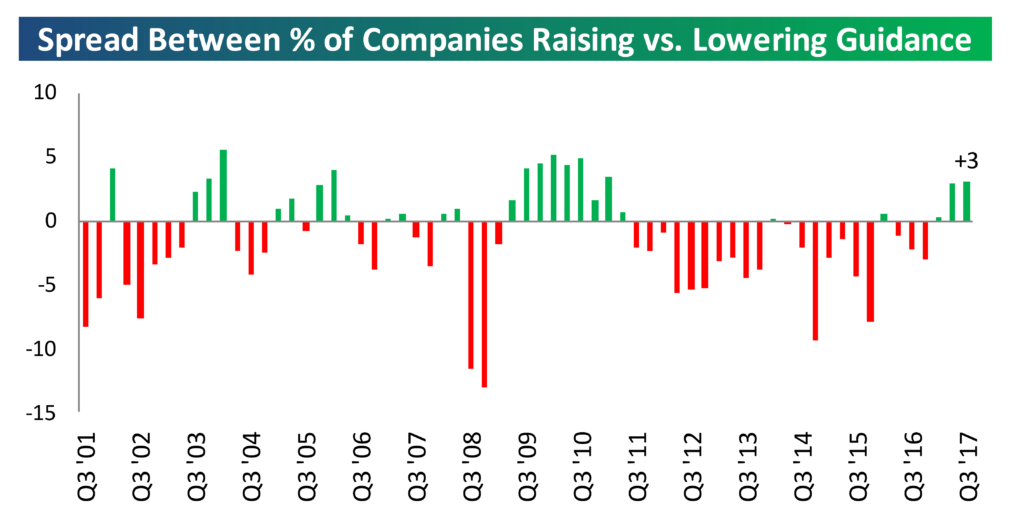

Also of note is the spread between companies raising guidance and lowering guidance. Not only is it at a positive three (more companies are raising guidance than lowering), but it is currently reading three straight quarters with a positive spread. Look back over time and you will see that hasn’t happened since the early part of this bull market…like the 2010/2011 time frame. In fact…it’s been a long string of red.

There is really no doubt about it – economic growth, corporate profit growth, tax reform and low interest rates, coupled with tapered near-term global anxieties, have been a powerful tailwind for the major indexes.

The bottom line is that the trajectory of stocks remains up as the global economy accelerates without any real inflation, low interest rates and earnings improvement…and there is the tax bill as a cherry on top.

Please call with questions.

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.