Dumb Money Ain’t So Dumb

I don’t normally write blogs about articles that other folks write, but in this case I must.

In Wednesday’s edition of The Wall Street Journal, the venerable Jason Zweig published an article called, “Why Charities Do Good—but Not Well—With Your Money.”

I’m a WSJ subscriber so I don’t know if this is behind a paywall, but I’ll highlight some of the article.

It starts with two NYU Professors, Sandeep Dahiya and David Yermack, reviewing some endowment returns. Assume they are smart – I’m reasonably smart, they teach at NYU and my NYU MBA application got rejected.

The typical small endowment, with assets between $1 million and $10 million, earned an average of 4.4% annually from 2009 through 2016. The median large endowment earned 6.1%—a little better, but not much.

Worse, 70% of the large funds failed to outperform the U.S. stock market, adjusted for basic risk factors; 59% of the small endowments fell behind on the same measure.

“You could have done better just by investing in Treasurys,” Prof. Yermack said in an interview, “and that’s pretty sorry.”

Then they go on to apply some analysis.

For the smallest nonprofits, according to the new study, returns improve with proximity to the financial centers of Boston, Chicago, New York and San Francisco, presumably because some advice from nearby professionals is better than none at all.

So, it looks like getting advice was helpful. But then there is this…

For the biggest endowments, however, “investment performance deteriorates if the fund is located closer to Wall Street or to another major financial center,” the researchers write. The closer the smart money is to the heart of the financial industry, the more susceptible it may be to “professional money managers’ sales pitches that lead to over-investment in exotic products with high fee structures,” they add.

It concludes with:

Even with those limitations, the study is a reminder of just how rare the smart money is.

In the words of Peter Lynch, former manager of the Fidelity Magellan Fund: “The smart money isn’t so smart, and the dumb money isn’t really as dumb as it thinks. Dumb money is only dumb when it listens to the smart money.”

But really, here’s my favorite part, just for emphasis…

…the more susceptible it may be to “professional money managers” sales pitches that lead to over-investment in exotic products with high fee structures…

That’s the best. I mean…THE BEST.

I see and hear about stupid investment ideas all the time. The fact of the matter is that there are people in my industry who get paid to sell products. That’s why there are quotations around “professional money managers” above. They are dirty. The fees are disgusting and since they have no advisory responsibilities, they give zero F’s about the illiquidity, fee drag, performance or the client who buys their shit.

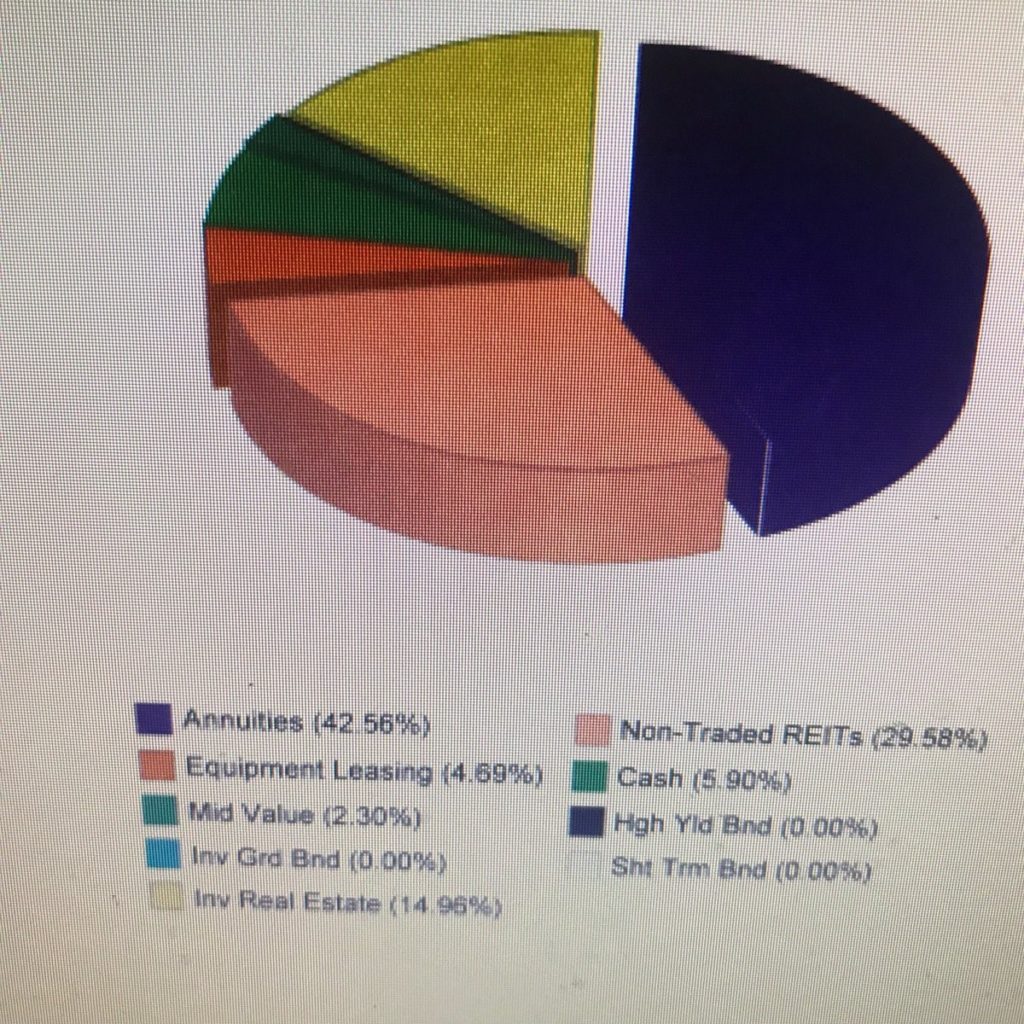

To punctuate my last paragraph, I’ll leave you with this picture from the Twitter account of Anthony Isola (@ATeachMoment) which shows this and a tweet that reads:

This just in! Portfolio of Champions 42% Annuities, 29% Non-Traded Reits and a separate managed account charging 2% which holds a 20% position in a Business Development Co.

Want to hear about a better way to manage money than using a bunch of shit? Email me, I’d love to tell you about how Monument is leveraging new technology to offer a simple, rules-based, globally-diversified, fee-effective and tax-efficient portfolio that is shit free. Figuratively…but literally too.

Because maybe dumb money ain’t so dumb after all.

Keep looking forward,

Dave

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.