Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Cross-eyed Mary

While the classic song found on the epic 1971 Jethro Tull Aqualung album is more about a wayward schoolgirl than an actual cross-eyed girl, it can evoke an image of someone or something not seeing straight. Like inflation.

So What’s Up With Inflation?

It may seem cross-eyed.

Casual mention of the word “inflation” can elicit many different responses. For example, what goes through your mind when you see a story on the low rate of inflation in the U.S.? Any way you slice it, it can probably be agreed upon that the official measures point to inflation that’s running below 2% per year.

Oh yeah, I know you… if you are a guy, you are probably eyeing that smoking hot deal on a 60-inch LED TV just in time for Rivalry Saturday in College Football. These days that thing is probably gonna run you a lot less than you’d spend on a new set of bed linen from Pottery Barn.

But on the other hand you may be saying, yeah but what about the rising food costs, higher health insurance premiums, the cost of an airline ticket or the most recent hike in your cable bill. Really, I’m 12-18 months away from a day where I’m not watching anything that is not streaming off the internet… but that’s another thought for another day.

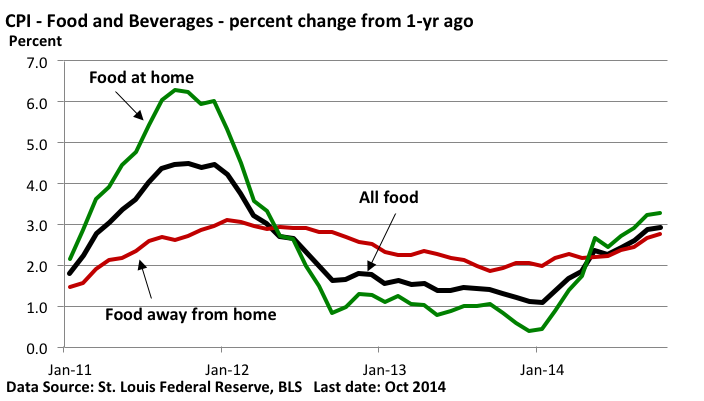

Without a doubt, it’s easy to point to anecdotal examples of outsized price increases. In the case of food, rising prices have outstripped the broader measures like the Consumer Price Index (CPI).

While food costs as measured by the CPI rose just 0.1% in October (BLS), price hikes at your local restaurant and in the grocery aisle have accelerated this year. See the chart below.

Since the start of the year, the rate of increase in all food (it’s the black line) has nearly tripled. Also, shelter costs (not in the chart but make up nearly one-third of the CPI), have been increasing at roughly 3% per year.

So yes, modest inflation is being reflected in parts of the economy.

But, the broader measure of inflation remains benign. For example, last month, the CPI (generally referred to as Headline CPI by smarty pants finance peeps) was unchanged as energy fell 1.9% including a 3.0% decline in gasoline prices. (You’ve been to the gas station lately, right?) If you strip out oil and food (known as Core CPI), inflation rose 0.2%.

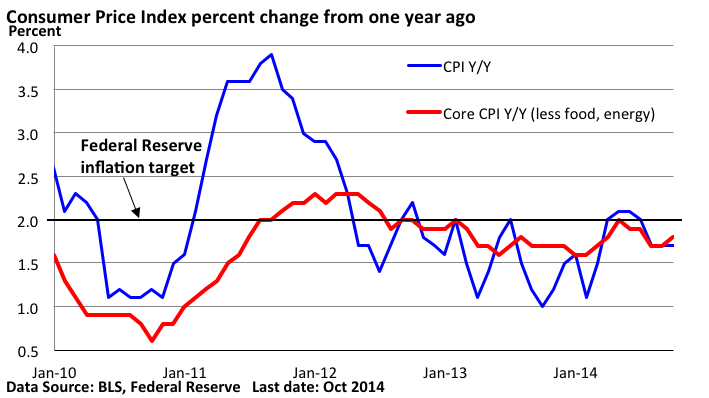

That leaves the year-over-year Headline CPI up 1.7% and the Core CPI up 1.8%. Historically, that’s pretty mild. Kicker – it’s also BELOW the 2.0% target established by the Federal Reserve. Check out this sweet chart.

Check out the part of the chart starting with January, 2013. For the most part, Core CPI (blue line) has held within a narrow range. AND, based on what’s happening to wholesale prices (measured by what’s called the Producer Price Index), there is little in the way of inflation building in the pipeline.

Now, given the recent drop in oil and most commodity prices, some inflation watchers are checking to see whether falling input costs will bleed into Core CPI. We’ll see.

Based on the minutes released from the Fed’s late October meeting, most Fed officials believe inflation is “likely to edge lower in the near term, reflecting the decline in oil and other commodity prices and lower import prices.” But they also continue “to expect inflation to move back to the (Fed’s) 2% target over the medium term.”

If the Fed is wrong and the rate of price hikes begins to slip, it may delay an interest rate increase, which most analysts believe will probably occur in middle of next year…IF it happens.

- I capitalized it because it’s a “BIG” if. Did you see what I did there? Creative huh?

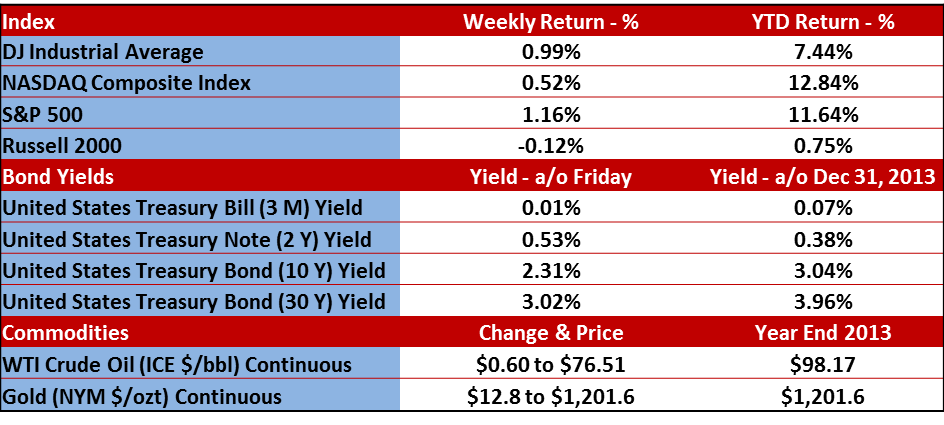

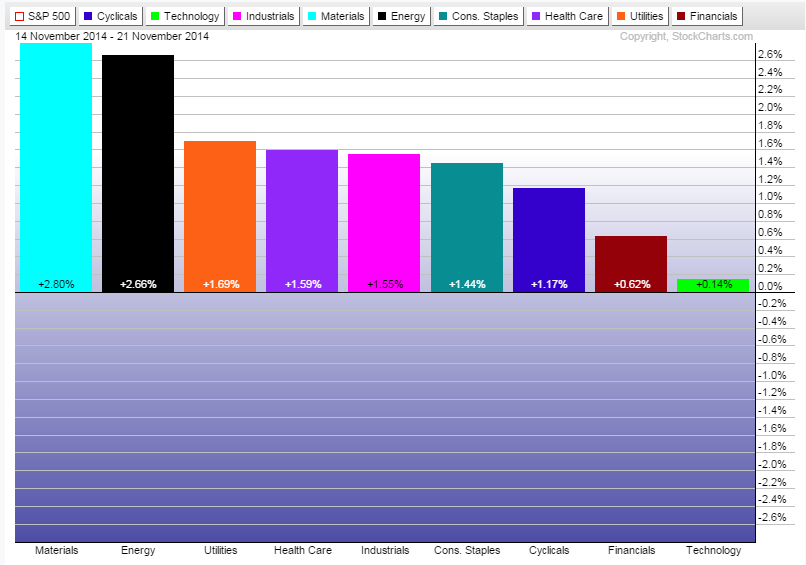

Markets

Here’s how the markets ended up last week.

Earnings

I missed blogging last week when earnings came to a close, so this news is about a week stale. The 3rd quarter finished up relatively strong. Here’s how it wrapped up:

The percentage of companies beating their revenue estimates for the 3Q ended up at 57.2%. This was below the average of 60% that we’ve seen since 2001 and also below the 60.7% that finished up the 2Q of 2014. However, it was above the 56% final reading we saw in the 1Q. Since the revenue readings bottomed out in the 4Q of 2011, quarter-over-quarter readings have ping pong’ed but the trend has been steady UP for revenues.

The percentage of companies beating their earnings estimates finished at 62.1%. This is above the 58.6% final reading from the 2Q of 2014 and well above the 56.7% reading from the 1Q. We were at 66% at one point but once the small-cap stocks started reporting, this came down. But it’s still good.

Thanksgiving

The stock and bond markets will be closed on Thursday and will close early on Friday. We will be open but lightly staffed. Please have a safe and joyous holiday with family and friends!

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.