Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

Confirmation Bias Everywhere…Am I Right or What?

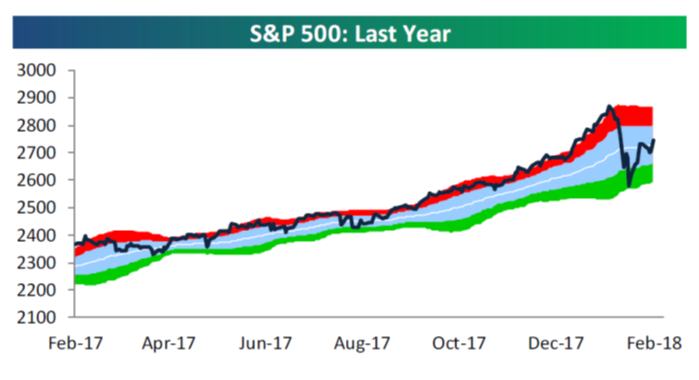

The S&P 500 is back to being nearly flat for the year. It feels worse than that, but it’s where we are. The S&P 500 rose to a record high of 2,873 on January 26th, which was a +7.5% gain for the calendar year. That makes the S&P 500 flat with about December 22nd…which was right when the Tax Cut and Jobs Act (TCJA) was passed.

So basically all the gains the TCJA provided for the earnings outlook have been offset by the early February sell-off when investors feared higher wage inflation and the possibility that the Fed would raise interest rates more aggressively.

Now, it’s fears of protectionism.

According to this weekend’s research report from Bespoke, “since 1/26 when the S&P 500 last closed at an all-time high, there have been 16 days out of 25 where the index saw a daily move of more than 1%. That’s twice as many 1% moves as we saw in all of 2017! Similarly, the S&P 500’s average daily move since the high on 1/26 has been +/-1.2%. In 2017, the S&P 500’s average daily move was a quarter of that just +/-0.3%.”

I think last week was another emotional sell-off. These occur because traders and short-term investors agonize that some new event is going to cause a recession. This sends prices down even though earnings remain solid.

Then once those traders and short-term investors realize that the event will not cause a recession, a rally ensues.

One day there will be a valid event that will correctly anticipate a recession and a bear market, but that will more than likely come as earnings are dropping.

But for now – earnings are GREAT. Earnings season wrapped up about a week ago with Wal-Mart’s report. Remember, companies are reporting earnings all the time, so in order to have a start and finish to compare quarters, Alcoa earnings report start the quarterly season and Wal-Mart ends it.

As you can see below, the beat rates for both earnings (the “bottom line”) and revenues (the “top-line”) were very strong. According to Bespoke, “the percentage of companies that beat EPS estimates came in at 69%, which was the highest reading since Q3 2006 and the sixth highest reading over the last 20 years. The percentage of companies that beat revenue estimates came in at 73.2%, which was the highest reading since Q4 2004 and the fourth highest over the last 20 years.”

Don’t poo-poo this – it’s a big deal because one thing that makes this season’s high beat rates even more impressive is the fact that analysts were hiking their estimates coming into the season at their fastest pace in more than ten years.

On top of earnings, let’s also consider all the good news about the US economy:

- The labor market is tight.

- Consumer confidence is optimistic. See Bespoke’s chart below.

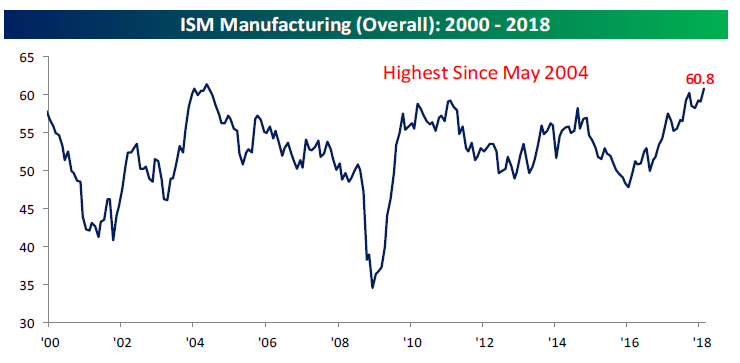

- Manufacturing is booming. On March 1st, February’s Manufacturing PMI was reported showing a gain to 60.8, the best reading since May of 2004. More from Bespoke, below.

- GDP growth is solid. On March 1st, the Atlanta Fed’s model estimate for real GDP growth for the first quarter of 2018 was increased to 3.5%, up from 2.6% on February 27th.

- Global trade is roaring. President Trump will most likely face powerful forces challenging his recent protectionist thrusts.

Be careful of one thing right now as it relates to politics…it’s called confirmation bias. It’s the tendency to say, “I told you so, Trump is nuts and since I’m right about that, I’m right that the world is coming to an end and another 2008 is right around the corner.”

It’s dangerous for your portfolio. I know March 9th, 2009 seems like yesterday to many, but the bull market turns nine years old on March 9th, 2018. Wow…This is now the second largest and second longest bull market since World War II with only the 1990’s bull market holding first place.

That seems to scare a lot of people, especially now with the recent talk of tariffs, higher interest rates, rising wages and increasing inflation. But remember the saying, “Bull markets don’t die of old age, they die of excesses.”

I don’t currently see the kinds of excesses I’ve seen in the past two recessions.

It’s been a while since I’ve written about the things we watch for that signal excess, but they are overspending, overborrowing, and overconfidence…and I don’t see signs of any of these things right now.

Everyone’s worst nightmare is another 2008. I get that. But that can’t keep long-term investors out of the market right now because the odds of a 2008 are low. It’s like saying you don’t want to fly because you are scared of being in a plane crash, but you are willing to drive to work 75 MPH next to other people texting, driving every day feeling immortal.

The real risk to your portfolio is inflation – that’s why you need to be invested. Being invested with a long-term plan and an asset allocation that retains enough cash to weather a storm is the best way to ensure your portfolio is not eroded by inflation.

If you are an investor who feels like the recent downturn has you questioning your willingness to take risk or stay invested, let us know. We have fun online risk tests that we’re happy to send you as a first step. You can email our Team at info@monumentwm.com and we’ll set one up for you.

Keep looking forward – Dave

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.