Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

The Blood Moon is to Blame for Everything

Everyone seems to want to know why the market is selling off. My casual response to that is usually “because there are more sellers than buyers,” but these days there is so much going on that I thought it would be useful to expand on my usual response with just a little bit more. These are in no particular order of importance or cause…just my thoughts.

Europe

Oh boy…global economic worries have everyone really down right now…ESPECIALLY over Europe. Germany has been posting really sucky data lately. In fact, just last week, German industrial production and exports fell at their fastest rate since January of 2009. One data point does not make a trend but it is data, and people are beginning to worry that Germany is at risk of slipping into a recession. So Europe…yeah. It’s sucking and the European Central Bank seemingly remains behind the curve even with some of its more recent actions.

EBOLA!

Supposedly, it’s not a disease that easily transmits from person to person, especially in a country like the U.S. with generally sanitary public conditions. But somehow a medical worker treating a victim in a Dallas hospital (who you would THINK would has state of the art protective wear) has contracted the disease. So that creates worry… and when the market is selling off this is gonna get thrown into the mix. Now we have Marines setting up field hospitals in affected areas (they do not have state of the art protective gear, I promise) and no travel restrictions. The poor judgment regarding the management of this situation rivals that of a pack of innocent women at a slumber party trying to escape a serial killer in a horror movie.

Geopolitical Issues

Tacking this onto the Ebola thought, when sentiment gets negative, there starts a lot of chatter about Russia, Ukraine, the Middle East and ISIS. So mix that in, too.

Strong Dollar

Most people may think a strong U.S. dollar is good, but it hurts the revenue of other international firms.

Ugh – the freaking SMALL-CAPS

The Russell 2000 (an index used to track small-caps) is in a correction and has experienced the so-called death cross. So the word death is being used in a sentence with Small-Caps. That has people nervous.

Poor Technicals

A lot of people feel like technical analysis is akin to voodoo. I see it differently. It’s really just a great way to visualize the effects of supply and demand in the market. So, the S&P has broken through its 50-day moving average. People who follow technical analysis generally see that as being bad.

The Dreaded Rate Hike

Jeezzz… it’s like seeing the bad guy in a hockey mask with a bloody knife with the hot unsuspecting chick standing right in front of him. EVERYONE SEES IT COMING! But alas, it is still a worry and it’s causing junk bonds to get beaten down like a perp in a Clint Eastwood movie. And problems in junk bond world can easily ooze into stocks.

Oil

Oil is in a free-fall. Good for the consumer. Bad for energy stocks. And they make up a big chunk of the overall market.

Quantitative Easing

News flash. It is coming to an end. And again, like the horror movie bad guy, everyone sees it coming but the end of Fed liquidity is probably causing some volatility.

REALITY

Look, It’s been over three years since we have seen a 10% correction. If you look at current or forward P/E ratios, it seems to me that equities are pretty fairly valued. It’s funny that when P/E’s were in the basement, it was hard to get anyone to listen that they were cheap and to an investor with a long time horizon, they were a screaming buy. Now when they seem fairly valued, everyone seems to think there will be some catastrophic sell-off as if they are just way too expensive and that the steep rise in stocks indices somehow means we should all have a serious anxiety attack.

So those are some thoughts on the current situation. Here’s what I think – my opinions. The U.S. fundamentals are solid and earnings season is upon us. Alcoa started us off last week with a pretty solid crushing of expectations.

And as for the Europe situation, the S&P states that European companies accounted for 9.7% of S&P 500 revenues in 2012 and Goldman Sachs estimates 7% in 2013. So at less than 10%, let’s not get everything all bunched up right this very second.

Also, the U.S. exported $270 billion in goods to Europe last year; but that compares to a $17 trillion U.S. economy. So if the 2012-13 euro-zone recession didn’t cause a slump in the U.S., I say we simmer down on any Europe panic because the U.S. economy is stronger today and it’s not very likely that another euro-zone slump will be the root cause of a U.S. contraction.

Falling oil and commodity prices are a plus for U.S. manufacturers and consumers, and the Fed won’t be raising rates still sometime next year

Finally, I leave you with this. Historically, bull markets end from recessions. I think the odds of a U.S. recession are very low. A 10%+ correction, if it does fully materialize would not be unhealthy for the stock market in the context of our still improving economy.

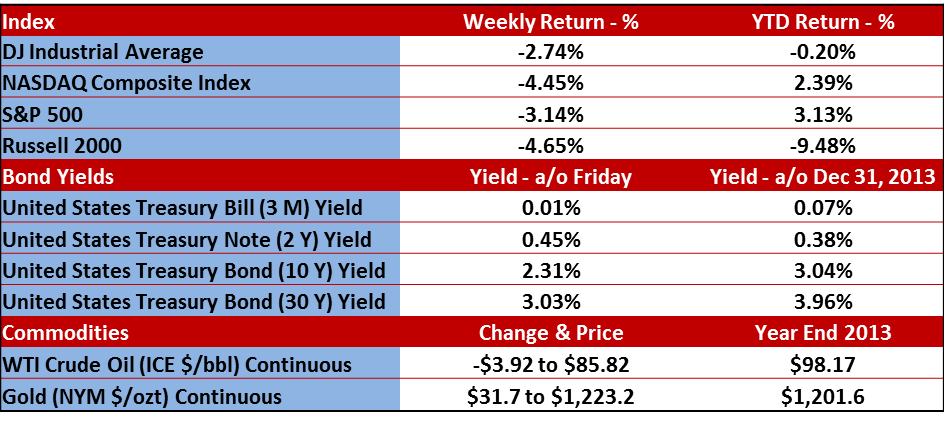

The charts below highlight the market action from last week. Send me any questions. I’m out of town helping a great group of advisors learn from our recent SEC audit experience (don’t worry, we did very well), and I’ll be tying a few things up during the trip that have been lingering on my to-do list but I’ll have plenty of time to respond over the week.

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.