Being Boring

Global markets surged higher this week, boosted by falling (read: diving) interest rates as bad economic data led most pundits to predict multiple Fed cuts this year. Everyone has heard the saying, “Bad news is good news,” but that’s usually not the case if the news is actually really bad.

So is it?

Well, it’s true that the global economy is a little sickly-looking…BUT, if the Fed is going to support growth with lower policy rates absent a really major slowdown (and that’s still an “if” no matter what the probabilities project), doesn’t the recent stronger equity performance make sense?

My answer is yes.

But are we going to have a really major slowdown? That’s the variable, because recent equity performance has been a function of those two things – expectation of the Fed lowering rates AND no major slowdown.

What I wrote in my May 29th blog post remains my current thought:

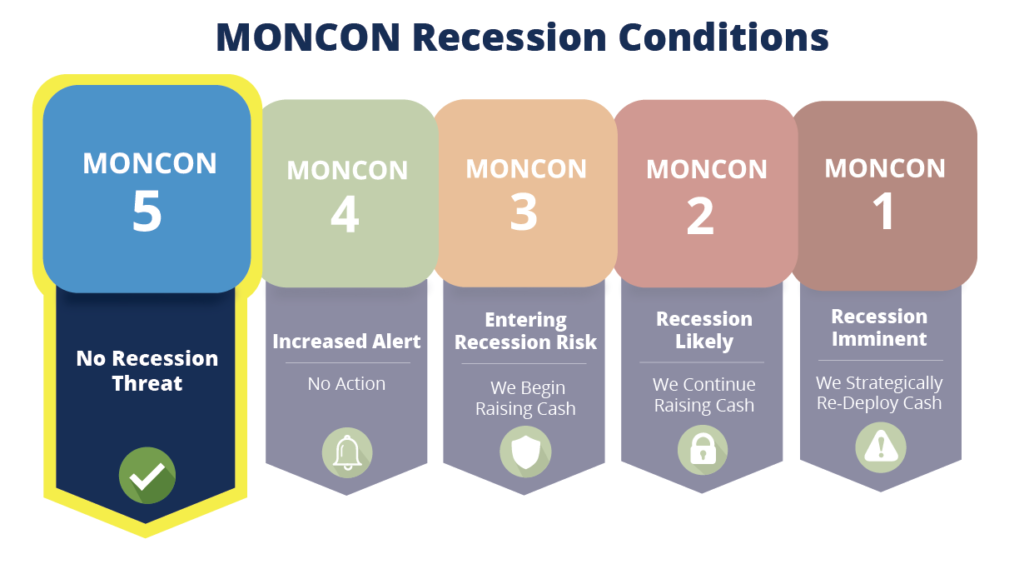

“For now, I still see MONCON 5. I see nothing in the model suggesting that we are in a recession nor do I see data that suggest we are within six months of a recession. It’s true that headwinds have picked up, but a slowing economy is nowhere near the same thing as a negative economy (recession).”

I’m just struggling to find any overwhelming evidence of a recession in the short term, despite the yield curve starting to show some inversions. REMEMBER, lead times to a recession from yield curve inversions are very long and widely dispersed, making them less useful for market timing purposes. This is why we use our MONCON gauge, and as of now, it’s still at MONCON 5.

In fact, as a human, I’m impacted by the daily news cycle highlighting the problems of the day. On the surface, they are all singularly important and meaningful in isolation. The question is whether or not each news item is important or even predictive of what’s to come.

This is why I rely on the MONCON reading.

Things haven’t changed enough to move us to MONCON 4. Sure, some inputs have changed, but nothing enough to move the needle. And even when it does, a move to MONCON 4 is not going to prompt any defensive action in portfolios. That won’t happen until MONCON 3.

MONCON has not changed because it’s not watching TV and it’s not subject to emotions…In fact, it never even budged in the 4th quarter of 2018, as the market tanked around 20%.

Sound boring? Does the lack of action in MONCON get you wondering if it even works? Does my steady drumbeat of the same old advice over and over again cause fatigue?

That’s the thing about boring, it gets really boring after 10 years. Fight the urge to do something just to do something…whether it’s trying to do even BETTER than you have been, increasing your risk just to take action, or taking chips off the table because you come to the conclusion that the market has gone on too long and must be getting ready to crash soon.

Personally, I find it hard to get bored with the below.

Investing is not a contest or a game – your benchmark should be progress toward the success of your plan and reaching your goals.

No one talks about that on TV…you know why?

It’s too boring…

Keep looking forward,

Dave

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.