Our “Off The Wall” Blog

is now Monument #Unfiltered

Subscribe below to receive our unique, straight-forward, unfiltered wealth advice delivered straight to your inbox.

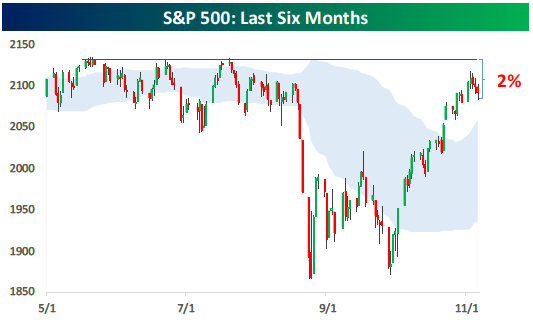

Ahh, 2% Away From an All-Time High?

First and foremost, Happy 240th Birthday to the United States Marine Corps. As I come up on my 26th annual lap in the Corps (I’m still in the reserves until spring of 2017), I’ve got to say that when our birthday rolls around, I’m a little nostalgic. I love all the emails that go around and the old pictures from field operations that get posted on Facebook. Happy Birthday Marines – we have the best uniforms and the best birthday celebrations. Raise one or ten tonight… I can assure you I will. If you know a Marine, be sure to tell them Happy Birthday. They will love that you know about today and how special it is to us.

First and foremost, Happy 240th Birthday to the United States Marine Corps. As I come up on my 26th annual lap in the Corps (I’m still in the reserves until spring of 2017), I’ve got to say that when our birthday rolls around, I’m a little nostalgic. I love all the emails that go around and the old pictures from field operations that get posted on Facebook. Happy Birthday Marines – we have the best uniforms and the best birthday celebrations. Raise one or ten tonight… I can assure you I will. If you know a Marine, be sure to tell them Happy Birthday. They will love that you know about today and how special it is to us.

That’s me enjoying some fine Tennessee moonshine at the Birthday Ball in Chattanooga, TN a few years back as the Commanding Officer of Battery M, 3/14. It was such good moonshine that…well…never mind.

The S&P 500 index posted its sixth straight week of gains last Friday. Not bad for a market that had everyone screaming bloody murder in August. Below is a Bespoke chart highlighting the last six months.

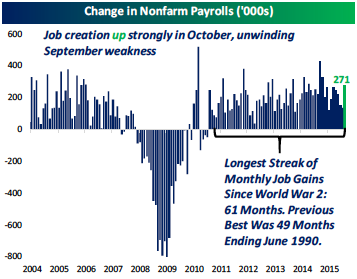

Last week, the U.S. Bureau of Labor Statistics reported nonfarm payrolls. It turns out they grew by 271,000 in October. That was WAY above the consensus forecast of 190,000. August and September reported 153,000 and 137,000 respectively, so October kind of smoked those too.

We love the revival in job growth and it confirms our assertion that the economy is expanding at a modest pace, despite all of the troubles we’re witnessing (ahem, getting beaten over the head by CNBC) in the global economy. However, remember that U.S. exports account for just 13% of total U.S. economic output, so even though China has a high global economic profile, U.S. exports to China account for less than 1% of U.S. output. We have written about this before. Go read it again and tell all your friends about it too.

So What’s the Point?

Well the point is that to us here in the U.S., it’s really insignificant and addresses why China’s troubles aren’t washing up anywhere else on our shores than the set of CNBC.

Manufacturing jobs are also worth taking a look at. Now I’ll warn you, if you or a loved one is in a manufacturing job, this will not be good news. However, from an economic perspective, it’s important to consider what is going on.

For starters, the number of manufacturing jobs created fell from 215,000 in 2014 to just 16,000 in the first ten months of October. However, manufacturing is no longer a substantial component to the overall U.S. GDP. Manufacturing jobs now only account for 9% of total U.S. employment.

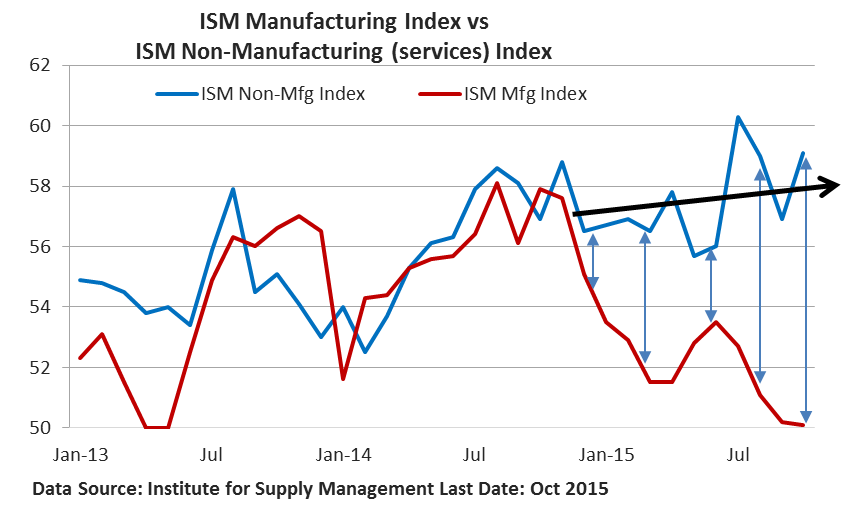

This is highlighted in the comparison between the ISM Manufacturing and ISM Services Index seen in the chart below (curtesy of Charles Sherry). These indices use “50” as the separating point between expansion and contraction. Look at the separation between the blue (services) and the red (manufacturing) lines.

While manufacturing is suffering (blame oil, gas and mining along with reduced exports/strong U.S dollar), it has not yet impacted the service sector. Well at least not according the ISM’s Non-Manufacturing (services) Index. On that note, did you know that three of the last four readings for the service sector have been the strongest of the economic expansion?

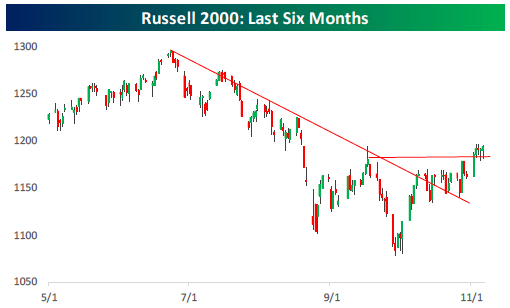

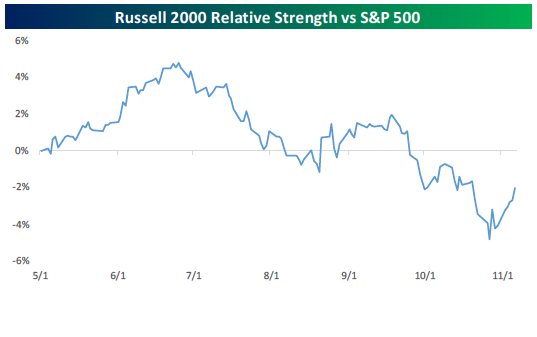

What the Hell is Going on with Small Caps!?!

We like Small Caps and still do. True, our ETF portfolio has been impacted over the past several months by this overweight, but we have not given up on them and we believe that we will end up being rewarded by our patience. Just this last week the Russell 2000 (a Small Cap benchmark index) was up almost 3% versus the S&P 500 which was up less than 1%. These two Bespoke charts show us that things are improving in the Small Cap space.

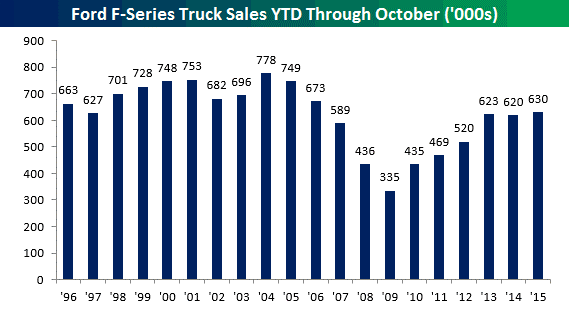

Vehicle Sales – Specifically Ford F150 Pickup Trucks

We have written in the past about Ford F150 sales. The theory is that most people who buy F150s buy them for business utility, BUT, they are a popular consumer vehicle too. So when sales are going up, it is a good economic sign. Sales of F150s are at a nine-year high (meaning 2006 was the last time sales were above this level). See below thanks to, who else, Bespoke. It compares year-over-year through October.

Finally – Thanks for All the Nice Emails on the Victory Lap

I was warmed by all the emails from everyone on the final portion of last week’s blog. It can be found here. I was also reminded of this gem by someone who has always remembered my older missives. Thanks, L.R. I appreciate it.

Important Disclosure Information for “Ahh, 2% Away From an All-Time High?”

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.