Explore Our

“Off The Wall” Blog

Read our Private Wealth Advisory team’s unique thoughts on the markets and investing.

2022 Outlooks

If you have known me for any time, you know that I generally eschew the annual forecasting published by all the major firms and their strategists.

Why?

My opinion is that it’s nothing more than guessing. But that doesn’t mean it’s not fun to review or think about, so I’ll go over some of the predictions and compare them to the previous year’s forecasts (to the extent I can go dig them up – but I’m saving them all this year to use next year).

But before I jump in, did you see that we have a newly launched podcast? With a bunch of episodes now live, be sure to check out the one where Jessica Gibbs and I host fellow Monument Teammates Erin Hay and Rohit Punyani in a discussion that delves into our Monument Flexible Asset Allocation portfolio strategy. It’s a great listen for anyone who likes a discussion on the nuts and bolts of portfolio management.

Let me just get this out of the way…it’s kind of unfair of me to pick on these forecasts, and here’s why.

The publishing analysts and their whole team are intelligent, professional, well-educated, credentialed, and impressive. I hold them ALL in the highest regard. Forecasting is what they do, and all of their research reports are grounded in rigorous research and analysis.

I hold all of these folks in the highest regard. I read what they write, and I deeply appreciate their reasoning for these annual forecasts.

But…I don’t believe it should be used as “actionable advice” in and of itself.

But let’s review them because, well, it’s fun and educational.

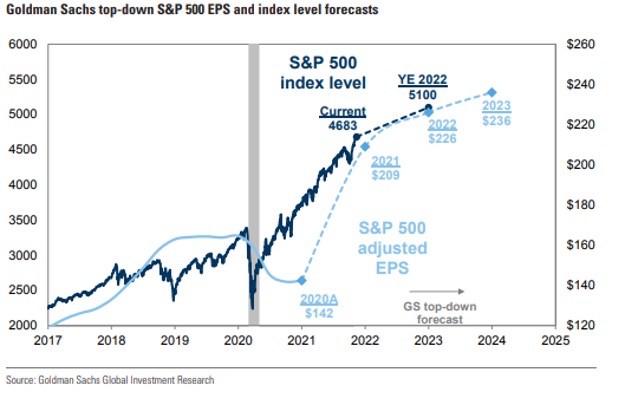

Goldman Sachs

Goldman publishes from two different groups: their Investment Services Group (ISG) and Global Investment Research (GIR).

David Kostin writes the annual outlooks for GIR, and he and his team have forecasted the S&P 500 index will climb by 9% to 5100 at 2022 year-end …so that’s a prospective TOTAL RETURN of 10% when you include dividends.

They predict that S&P 500 earnings per share (EPS) will grow by 8% to $226 in 2022 and 4% to $236 in 2023. Not bad. (See below for the chart from the report.)

JP Morgan

Marko Kolanovic published the JP Morgan (JPM) Global Markets Outlook in early December and has the S&P 500 finishing up 2022 at 5050 and EPS coming in at $240. So their index level forecast is close to Goldman’s, but they are forecasting a much higher EPS. Their estimate for the 2021 S&P 500 index level was the highest on the street at 4700.

So as JPM looks ahead, they see moderate market upside on better than expected earnings growth.

LPL Financial

I love LPL research…it’s elegant in its simplicity, and their analysis is easy to read and relatively jargon-free. But don’t make the mistake of thinking that it’s not the output of serious analysis.

They just have their own style…just like we do, and I like it.

They publish their stuff to the public, which I think is cool. You can follow it all on Twitter: @LPLResearch, Ryan Detrick @RyanDetrick, and the very sadly retiring Burt White @_BurtWhite.

LPL is forecasting the S&P 500 to end 2022 between 5000 and 5100…so in line with JPM and Goldman. Their EPS forecast is coming in a little lower than the others at $220.

SO WHAT?

Again, I love the forecast reports that come out at the end of the year, and it’s all based on good solid, intelligent thinking. Said differently, none of it is grounded in stupidity.

But…

It’s still all guessing. Educated guessing, and fun to read, but guessing nonetheless.

And that’s a problem for anyone who uses forecasts as an investment decision-making tool to adjust portfolios.

Ok, by now, you get it…you know we eschew the actual forecasting. But if you KNOW us, you also know THIS about us – we provide unfiltered opinions and straightforward advice.

SO, here it is.

Our philosophy is centered on determining where the greatest odds are in your favor. That’s it…much like a casino can’t control the short-term volatility of gamblers’ hot streaks at the craps table, the casino knows that the odds of positive returns are in their favor over time, and they stick to those odds.

So are the odds suitable for investors? We think yes.

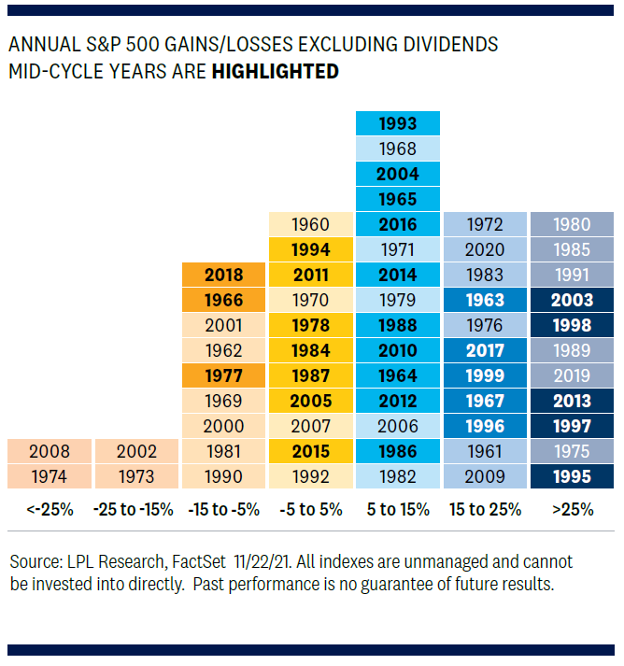

It’s our opinion that we are in the middle stage of an economic cycle. The Fed usually starts raising rates towards the end of the economic cycle, so because they are not yet raising rates, it stands to reason we are not in the late stage of the economic cycle.

In looking at the past 60 years, the S&P 500 Index was up an average of 11.5% during the 30 mid-cycle years identified, and 80% of those 30 years had positive returns. (See chart below – the highlighted years are considered mid-cycle years.) 1966 and 1977 were the only two years with double-digit losses (2018 was a loss but not double digits).

It’s widely believed that the Fed will not start to raise interest rates until 2023, so we are confident in our opinion that we are mid-cycle.

BOTTOM LINE

Take a look at the skew of returns below – it’s showing that the odds are in favor of investors being in the equity markets.

Don’t mess around guessing next year…be in the market because we believe the odds are in your favor.

Of course, there is the chance that odds go against you, BUT that’s where a solid plan comes into play. A good plan should account for those times that the odds go against you. That means a reliable cash flow plan and resources to fund your cash needs in times when things don’t go as planned.

Get help creating a plan! (Pro tip – an asset allocation and portfolio is NOT A PLAN.)

KEYS TO REMEMBER FOR 2022 (AND ALWAYS):

- Don’t risk what you have and need for what you don’t have and don’t need – a good plan helps with this.

- Be financially unbreakable – have the resources available to fund your cash needs during market downturns, so you don’t have to sell investments when they are down.

- The market has had a great run. LOOK AT YOUR CASH NEEDS AND RAISE THEM NOW. Nothing will make you happier than seeing your cash needs sitting nicely in your account when the market goes down. Bonus – if you don’t need that cash when the market sells off, you can buy the dip.

As for Monument’s strategies, we continue to follow our rules-based models that guide us by facts rather than emotions and speculation.

If you are a current client reading this and have questions as we head into the new year or if you need to plus up your cash, please let us know. Just know we have the portfolio management covered and are positioned to take advantage of the odds that 2022 will be a good equity market year

If you are not a client and want to know more about how we create Private Wealth Designs, please reach out – we are not selling timeshares, so don’t be scared we will crush you with some sales machine. We are normal people, just like you. Our value proposition is that we are smart practitioners, and our unfiltered opinions and straightforward advice are what sets us apart from the rest of the industry.

Our culture, philosophy, and causal attitudes are not for everyone, and that’s okay. We take what we do very seriously…We just don’t take ourselves too seriously. We aren’t trying to resonate with everyone. We know that our value proposition resonates with the people who want to remove a source of anxiety from their life through good advice from smart, normal, likable people who bring dogs to work…because we can.

Have a great holiday season, and as always…

Keep looking forward,

David B. Armstrong, CFA®

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.