Explore Our

“Off The Wall” Blog

Read our Private Wealth Advisory team’s unique thoughts on the markets and investing.

Market Value and Intrinsic Value – Know the Difference

I realize that the idea of sitting down and devouring a good book is usually on everyone’s to-do list. However, when they imagine doing that, I bet it’s rarely with a book about finance … but I have a good one for you. It’s one you can just pick up, open to any page and read for a few minutes. It’s called “The Devil’s Financial Dictionary,” by Jason Zweig from the Wall Street Journal. You can find it on Amazon.

I flipped through it and was laughing within seconds – sarcastic humor based in truth is right up my alley. It really captures a great deal of my global view and fuels my dream of creating a YouTube show modeled as a mashup of the Jon Stewart Show and the old SNL “Really” skits done by Amy Poehler and Seth Meyers. The show would conceptually make fun of, you guessed it, the finance industry. See my favorite SNL “Really” skit here.

Anyway, back to Zweig’s book. It’s a collection of words and definitions, but in order to be funny he takes a great deal of artistic license in modifying the definitions…because let’s face it, if he didn’t it would just be a dictionary and who buys those anymore? Here are two of my favorites from my quick flip through:

- Long-Term: On Wall Street, a phrase used to describe a period that begins approximately thirty seconds from now and ends, at most, a few weeks from now.

- Patience: A quality apparent among such lower life forms as snails and tortoises but rarely among humans who invest in financial assets.

If that made you chuckle, go buy the book…since my YouTube show is not a 2016 project unless my West Coast Creative Partner Rob Bartenstein, @rbartensIII gets motivated. #letsgetitdone

Not For Sale

I spend most weekends down in Southern Maryland and drive by this car every weekend. I always chuckle when I see it. Today I stopped and snapped a picture. It’s hard to see but there are Ace Hardware type stickers that spell out “Not for Sale”.

It leads me into a quick overview on pricing. See, there are always two prices for every asset – the market value, which is what people are willing to pay you for something, and then the intrinsic value, which is what the asset is really worth. In the world of investing, intrinsic value can be thought of as the actual value of an asset.

As an investor, it’s important to remember that these two prices are separate and distinct. Selling because the intrinsic value has changed is a different decision than selling because the market price has changed. If your reason for owning an investment has not changed and the intrinsic value has not changed, it’s best to ignore the market price.

In the case of this car owner, he clearly feels the intrinsic value is so high that he’s not willing to entertain the market prices people are offering because the reason he bought and continues to own it has not changed. (P.S. The picture is more ironic than instructive, but it’s a good lead in.)

If you own assets in your portfolio that have seen their market prices decline but both the reasons you own them and the intrinsic values have not changed, you should mark them “Not for Sale.”

Bull Markets, Bear Markets and Recessions

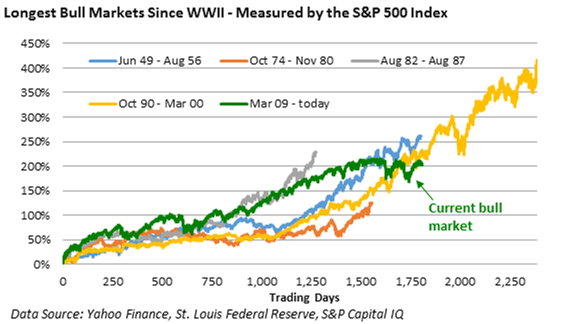

Since around the conclusion of World War II, the S&P 500 Index has participated in eleven bull markets, including the current one. Let’s take a quick peek back.

The shortest bull market lasted 26 months, which was from 1966 through 1968. I was born in 1967 so as luck would have it, I’ve lived through the shortest bull market. Call it bragging rights.

The longest bull market was 115 months, running from 1990 – 2000. As luck would have it, this bull market prompted me to change from being a full-time officer in the Marine Corps watching things blow up around me into a career in finance. After finishing my MBA in 1999 and going to work at the old Donaldson Lufkin and Jenrette, I was still watching things blow up around me…this time, though, it was tech stocks.

That brings us to today. The current bull market is 87 months old, but is still more than two years away from topping the 1990 – 2000 bull market. As of this month, the current bull cycle surpassed the June 1949 – August 1956 bull market, and is now officially the second longest since the end of World War II (Hat tip to Burt White and the seemingly tireless LPL Research team).

Here’s a chart from Charles Sherry that shows the lengths of some of the longest bull markets.

Of course, this assumes the S&P 500 Index can exceed its earlier high set on May 21, 2015 of 2,130.82. Last Friday we saw the S&P 500 close at 2,046.61. If the market goes down from here and closes 20% down from that May, 2015 high, then that would be the official end date of the current bull market.

The natural next question is when will the current bull market end? Bull markets generally don’t die of old age, they have historically been killed off by recessions. See this video we posted the beginning of this year, there is a great section on recessions.

As I’ve written about many times before, while tepid corporate and economic growth have been the norm and we may see more volatility in stocks, most indicators are not suggesting a recession is imminent.

Be sure to see our next video coming out sometime next week where I review these indicators and their current levels. (Preview: they are showing an even smaller chance of recession than at the beginning of the year.)

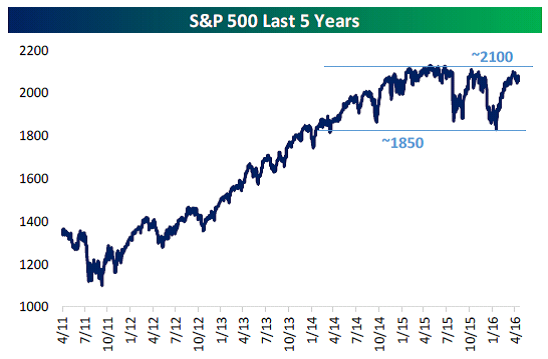

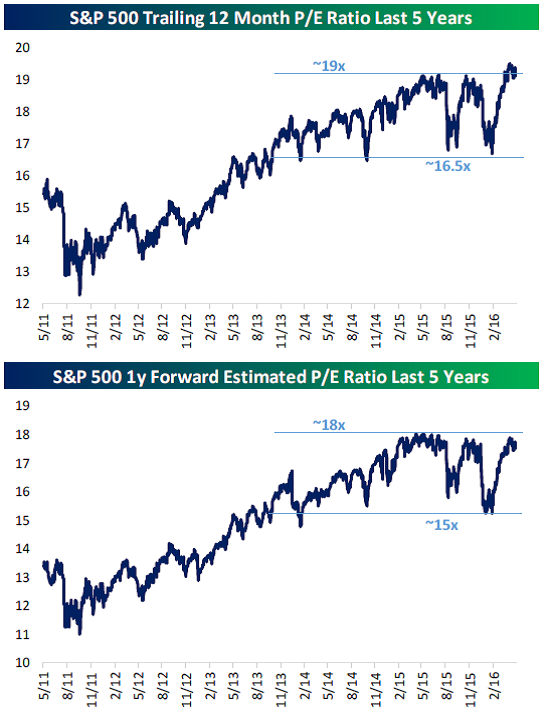

The Market and Portfolio Returns

As I wrote about in my last blog, the S&P 500 has been very range-bound for the past 18 months. Here’s another chart from Bespoke showing the range-bound nature of the S&P 500.

Bespoke goes on to highlight that while the markets have been range-bound, they have not been the subject of runaway valuations.

Please call or email with questions.

Important Disclosure Information for “Market Value and Intrinsic Value – Know the Difference”

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. All indexes referenced are unmanaged and cannot be invested into directly. The economic forecasts set forth may not develop as predicted. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA®

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.